Of the technical challenges that confront operating in harsh environments, those facing deepwater oil and gas developments are unique. Such projects require high capital outlays and decades-long development plans. Investment decisions are made for the long term, and project economics can be very sensitive to reservoir performance and fluctuations in oil and gas prices.The deepwater Gulf of Mexico (GOM) is still an attractive place to invest, despite recent regulatory changes. The region’s geology and well-developed infrastructure are complemented by a stable fiscal regime. A typical discovery makes positive returns in all five GOM play types. Future development of yet-to-be-found resources in the basin could generate as much as USD 25 billion in net present value (NPV).

Continued development of the conventional Pliocene/Miocene, Lower Miocene, and Paleogene plays will drive regional spending in the medium term. In addition to these plays, discoveries in 2008–09 unlocked the Jurassic and subsalt Pliocene/Miocene, which boast good-quality reservoirs in ultradeep water. Each play’s relative advantage in maturity, location, and reservoir quality ensures returns of more than 10% for a typical discovery.

Capital will shift from maturing plays toward those with large remaining resources. Operators are prepared to accept lower returns in order to diversify portfolios or establish a first-mover’s advantage in plays with large upside potential. This upside can be substantial. A 2-percentage-point increase in recovery or a USD-10/bbl increase in oil price adds USD 1 billion of value to a typical Paleogene field.

Recent Discoveries Add Two New Plays to GOM Potential

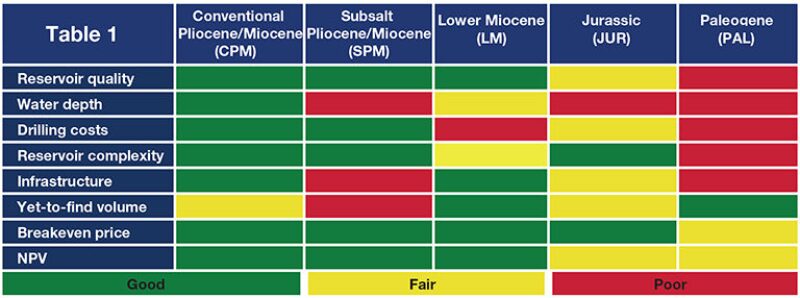

Over time, operators in the deepwater GOM have targeted geologically older plays in even deeper water. Operators initially targeted the shallow conventional Pliocene/Miocene sands before moving into the Lower Miocene. Recent discoveries in the Paleogene, Jurassic, and subsalt Pliocene/Miocene are expected to support long-term regional development. Table 1 presents each play’s relative advantages and disadvantages.

Wood Mackenzie has defined the conventional Pliocene/Miocene play as encompassing Pleistocene, Pliocene, and Upper Middle Miocene targets. The play is mature, but commercial discoveries are still common because of its extensive infrastructure, relatively shallow targets, and short development times.

The Lower Miocene play is the engine of near-term production, with good-quality reservoirs and developed infrastructure. Fields such as BHP’s Shenzi and Chevron’s Tahiti produce at spectacular rates from the play. Existing infrastructure allows smaller finds to be economical as subsea tiebacks. Well costs can be high because these targets are often deep.

The Paleogene, or Lower Tertiary, was first developed in the early 2000s with Shell’s Perdido hub and Petrobras’ Cascade and Chinook fields. Paleogene wells are the most expensive to drill and complete because targets are very deep and the reservoirs are complex. Operators also need high-specification subsea equipment to manage high pressures and temperatures. A high well count is required as reservoir qualities are poor.

Shell’s 2009 Appomattox find unlocked the Jurassic play offshore. Although the play is in the early stages of development, it has a good gas-to-oil ratio and is less remote than the Paleogene. Shell has formed a strategic partnership with Nexen to explore and develop its acreage in the play.

Anadarko’s Lucius and ExxonMobil’s Hadrian were the first finds in the subsalt Pliocene/Miocene play in 2008–09. The play is very attractive because its shallow, good-quality reservoirs can be developed quickly at a relatively low cost. Future volumes are currently not expected to be large because the number of future discoveries is thought to be limited.

Positive Returns Can Be Made in All Plays

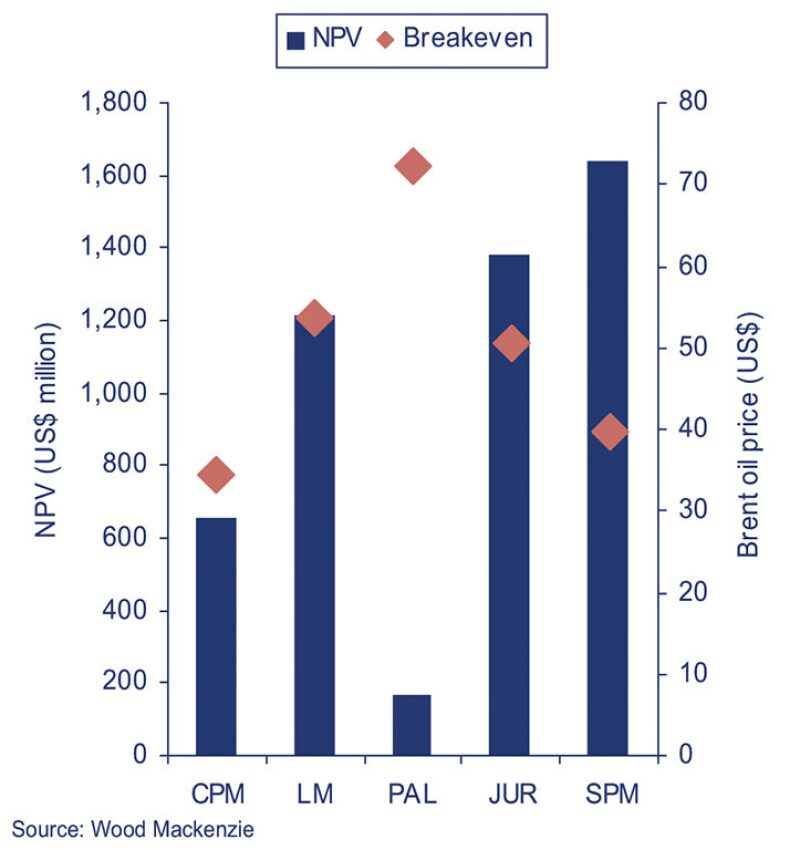

In order to assess play economics, models were created for a typical discovery in each play. Each field is projected to generate a positive NPV. Breakeven oil prices for each play are estimated at under USD 75/bbl, and only the Paleogene is targeted to become subeconomic in a USD-60/bbl low-price environment. The conventional Pliocene/Miocene is projected to still achieve a 10% internal rate of return at an oil price of USD 35/bbl due to inexpensive wells and little capital requirement for subsea development.

The subsalt Pliocene/Miocene discovery is estimated to have the highest NPV because it can be developed with few, low-cost wells with high flow rates. The Paleogene discovery has the lowest NPV because of very high well costs and low estimated ultimate recovery (EUR). In the conventional Pliocene/Miocene and Lower Miocene, the high EUR relative to project costs increases value. The Jurassic discovery is modeled with a relatively low EUR per well. However, the expectation is that drilling and facility costs will be lower than those for the Lower Miocene, resulting in a higher NPV.

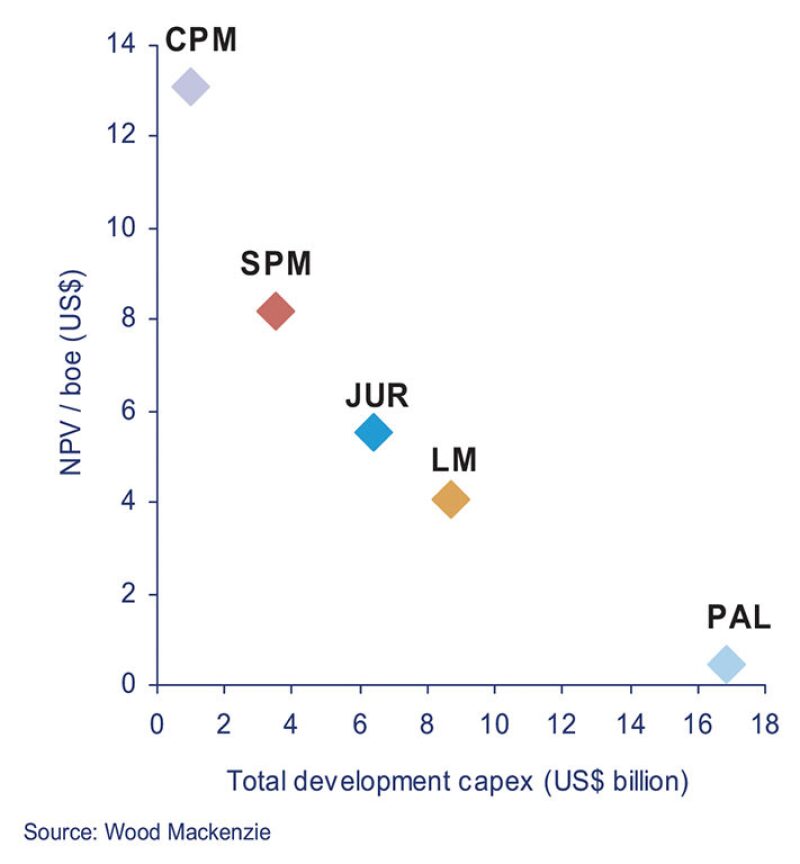

Deepwater operations are very capital intensive and high capital-expenditure (capex)/boe ratios erode value. The Paleogene creates the least value per barrel because its capital requirements are almost double those of the Lower Miocene. As the play develops, cost savings per well are unlikely because the reservoirs are so deep and of such poor quality. The crude is also of low American Petroleum Institute (API) gravity and high sulphur content. Operators are relying on the upside potential of the play to justify the low returns.

The model assumes an 8–10% recovery factor for the Paleogene. It is estimated that an increase of 2 percentage points in the recovery factor or USD 10/bbl in the oil price would add USD 1 billion in NPV. This upside would improve the NPV/boe ratio of the play to levels comparable to the Lower Miocene. It is likely that EURs will improve for all plays as technology advances.

The conventional Pliocene/Miocene and the Lower Miocene have good-quality reservoirs and were expected to attract about USD 9.8 billion in total development capex in 2012, or about 72% of regional spend.

After 2014, operators are expected to invest the most in the Paleogene play. Unlike the Lower Miocene, low-cost subsea tiebacks are currently not possible in the Paleogene, subsalt Pliocene/Miocene, or Jurassic because little existing infrastructure means most projects will require a standalone facility.

Value Is Not the Only Variable

The evolution of the Gulf of Mexico has been a continuous expansion of its exploration and development boundaries. The first operator in a play can cultivate a favorable acreage position, technological expertise, and a strong prospect inventory. Examples of first-movers are Chevron in the Paleogene, Shell in the Jurassic, and Anadarko in the subsalt Pliocene/Miocene. Continued success in the Gulf of Mexico requires forward-looking investment, and operators may need to accept lower returns until the technology can catch up with the resource potential.

Economic Assumptions

The model presented assumed a Brent oil price of USD 110.09/bbl in 2011, USD 102.00/bbl in 2012, USD 99.00/bbl in 2013, and USD 92.00 in 2014. Projected post-2014 prices equate to a Brent long-term assumption of USD 80.00/bbl in real-dollar 2011 terms. Beyond then, West Texas Intermediate (WTI) crude was assumed to trade at a 2.5% discount to Brent. The Henry Hub natural gas price assumptions were USD 5.00/mcf in 2011, USD 5.40/mcf in 2012, USD 5.67/mcf in 2013, and USD 5.69/mcf in 2014. After 2014, prices were inflated at 2.0% per annum in nominal terms.

Each field was assigned a price differential to Brent based on its assumed API gravity. The differentials ranged from a 3.5% discount to a 6% premium to WTI.

All breakeven prices were calculated for a 10% rate of return.

The cash flows were discounted at 10% nominal to January 2012. Each field was assigned an 18.75% royalty rate, with no royalty relief. Each field was assumed to be leased after November 2007, with tax terms dependent on the assumed water depth.

The analysis assumed each field was discovered in 2011, with timing, costs, and resource size dependent on the play.

It was assumed that all wells were drilled with a floating rig.

Lauren Payne joined Wood Mackenzie in 2010 as a research analyst on the deepwater Gulf of Mexico upstream research team. She provides insight on regional trends and develops asset-level production models and commercial valuations. In this role, Payne has focused on evaluating regional regulatory changes and forecasting near-term activity levels. She holds bachelor’s degrees in international business and government from The University of Texas at Austin.

Jackson Sandeen joined Wood Mackenzie’s deepwater Gulf of Mexico team in 2011. He has been following the rig market closely and published an article on market constraints in early 2012. Jackson earned a BA degree in economics and a BS degree in broadcast journalism from Boston University. During 2010, he interned in the global wealth management division of Merrill Lynch’s Boston offices.