New energy’s time has come. It is less than 4 years since the Paris Agreement set the long-term goal to limit the rise in global temperature to well below 2°C. Back then, the oil and gas industry had zero appetite to invest in decarbonization. Paris lit the fuse. I caught up with Valentina Kretzschmar, research director at Wood Mackenzie, to find out what’s happening.

How serious are oil and gas companies about decarbonization?

It now sits at the very center of the strategic debate. The disruptive threat from zero-carbon technologies like electric vehicles may be some time off—we think peak oil demand isn’t until 2036. Meanwhile, government pressure is ramping up. The UK’s new target for net-zero emissions by 2050 is just the start. More immediate is investor agitation, pressing boards to address carbon emissions and build a sustainable business model. The sector’s share of global stock market indices has halved in a few years. The challenge is to stay relevant and investable.

Who is doing most in the space?

European majors are leading, though strategies vary. Total and Shell have gone further than the rest in increasing exposure to renewables and other clean technologies, but Shell is out on its own in laying out a net-carbon neutral ambition. But more and more international and national oil companies recognize the need to signal clear intentions to shareholders and stakeholders.

What are majors investing in?

They have bought into much of the zero-carbon value chain. Biofuels and carbon capture and storage have been in their portfolios for some time. The focus in the last 4 years has been on renewables (solar photovoltaics, and onshore and offshore wind); battery storage and electric vehicle (EV) charging; and forestry (carbon sinks). There are similarities in scale and complexity between development of the biggest renewables and upstream projects.

How much have they spent?

In time, it is going to be big, but very little has been spent so far—just $6 billion on mergers and acquisitions (M&A) in 4 years, a tiny fraction of investment in the core business. But it is in the formative stages. Right now, it is about positioning, trialing and testing. Companies are trying to assess technologies—and timing—and where they can create value. Both Total and Shell are planning to invest up to $2 billion a year and Total has committed to having 20% of assets in renewables by 2030.

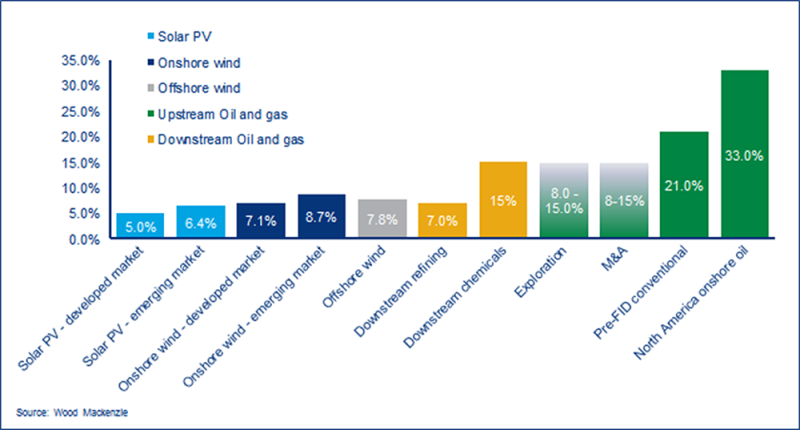

And the returns?

Typically, single digits, say 5% to 9% internal rate of return (IRR), depending on the technology and market among other factors. Returns can be boosted by innovative financing models and taking merchant risk. They don’t stack up well against pre-FID [final investment decision] upstream oil and gas project returns, though there is not a huge difference on full-cycle comparisons. It is also worth bearing in mind that oil and gas returns will shrink as the energy transition gains momentum. That’s what ultimately will drive a ramp-up in exposure to zero-carbon assets.

Can you do new energy without customers?

Yes, though a pure renewable generator has similar advantages and disadvantages to a pure exploration and production player. An integrated business model—generation with customers—has potential for synergies between power and gas, and commodity trading could add significant value. Financing, too, is key in this game; big oil can use its balance sheet to its advantage. There is also scope to leverage customer margins by selling other products and services, including EV charging. Total has dipped its toe in the water by buying Direct Energie (2 million customers) in France, while Shell acquired First Utility (under 1 million) in the UK and is currently bidding for Dutch utility Eneco (0.7 million). We don’t think low-return transmission and distribution assets play any part in big oil’s model.

What takes things to another level?

A big acquisition. The power market is highly fragmented and zero-carbon businesses are typically small or held within a regional or local utility. Big oil with an ambition to be big in new energy will need scale. It may be some years away yet, but transformational M&A will come and accelerate the buildout.

|

|

Simon Flowers is chairman and chief analyst at Wood Mackenzie. He provides thought leadership on the trends and innovations shaping the energy industry. His blogs on energy industry insights can be accessed here.

Valentina Kretzchmar is director of corporate research at Wood Mackenzie. She advises senior managers on strategy, operations, and financial analysis.