As the entire energy industry transitions across upstream, downstream, and midstream, there is an increasing need for those with industry expertise to take on some of the challenges we collectively face. Industry outsiders often promote technology solutions which look great on paper but fail to recognize some of the unique challenges that only those with relevant experience and expertise can identify. However, by combining new ideas, technology solutions, and the understanding that comes from working in our industry, we have an opportunity to drive the change that will be an inevitable part of the decades to come.

One key part of the energy ecosystem is the trading of these commodities and the freight that transports them. Throughout this process, traders are constantly looking for optionality; choice on when, what, and how much to buy and sell. This optionality allows them to find opportunities and create value for their respective businesses.

When deciding on which price should apply to a specific deal, traders often buy or sell at a premium or a discount to a specific index. Brent crude oil, West Texas Intermediate crude oil and Henry Hub natural gas are some of the most common examples of these indices. Although there is not a “one size fits all” solution for the commodities market, the vast majority of these price indices are defined by price reporting agencies (PRAs) and, more typically, this means just one or two companies. Traders then use these prices as a reference when discussing deals (which can take anything from hours to days to conclude, depending on their structure and complexity), constantly trying to extract value but often without the necessary transparency to make the best decisions. By way of analogy, it would be similar to buying or selling property without a good knowledge of the value of houses in your city and street.

The prices generated by the incumbent PRAs (covering oil, gas, agricultural products, metals, and many other commodities), whose business model typically relies on an army of journalists to gather price and transaction information, impact almost everyone on the planet. These prices are then shared, normally at significant cost, with the trading community often via basic platforms or in PDF format, making it difficult for traders to understand how such prices are derived. Yet despite the enormous impact these prices and organizations have on each and every one of us, very few people can name even one of these PRAs.

At a macro level, the methodologies outlining how these prices are formed are often unclear, hard to understand, and difficult to find. Yet entire trade flows, GDPs—and therefore entire populations—not to mention the costs of everyday items, are all impacted by these price assessments. At a micro level, traders, despite their constant search for optionality, ironically have almost no options or choice in who or what defines the prices, with one index typically dominating an entire market.

Conceptually, this situation just didn’t make sense. So, in early 2019, I left a job I loved (trading LNG cargoes and freight) and started Spark Commodities, based in Singapore and backed by Kpler, the industry leading commodities analytics and data provider, and EEX, a world-renowned global exchange which is part of the Deutsche Boerse Group. The goal was simple enough—to redefine how commodity markets trade. The reality was that we were taking on some of the biggest, most established players in a multibillion dollar part of the energy industry. However, a strong combination of shareholder support and a strong, in-house developer team gave us the foundation to have a chance of making an impact. Importantly, it also allowed us to position ourselves so that we could provide the market with a choice when deciding which index to support on critical commodities.

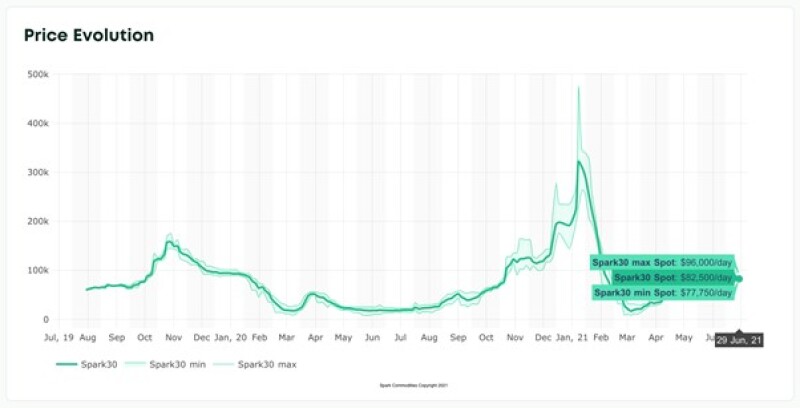

Our initial focus was—and remains—on LNG freight, a critical part of the LNG value chain that historically didn’t have a price index and was (and continues to be) increasingly volatile and difficult to manage. To put that volatility into perspective, in June 2020, the rates were $17,750/day, before peaking at $322,500/day in January 2021. Since then, they have fallen to a low of $16,750/day in March, just 2 months after hitting record highs. As of writing on 29 June 2021, they are currently at $82,500/day. This volatility highlights the need for tools both to understand and risk-manage such price moves.

By removing the journalistic assessment component, and replacing the traditional black box inherent in most PRAs with more transparency, we provide the market with far more insight-driven information, underpinned by a greater volume of data. The more trustworthy prices lead to a higher probability of adoption, trust, and therefore liquidity which, in turn, helps manage risk more effectively. By keeping technology and execution at the heart of what we do, Spark has built an organization that is designed to be responsive and relentlessly opportunistic as the wider industry continues to evolve and adapt to the various challenges in accurately assessing commodity pricing.

Spark now has a set of products, strong market support, and a partnership with one of the largest exchanges in the world, Intercontinental Exchange (ICE). By partnering with ICE, our customers can trade more easily. To draw on the example of the ever-evolving cryptocurrency revolution, the ability to buy and sell Bitcoin and other tokens on exchanges (rather than just bilaterally) has rapidly accelerated their adoption as well as the ability for a wider variety of buyers and sellers to enter the market. For us, albeit on a smaller scale, the same principle applies.

Two years ago, most people said this would be impossible, asking how a startup could compete with some of the biggest, well-funded names in the industry. Two years, 200 organizations on the Spark platform and one listing later, I hope that we have demonstrated the willingness of the industry to embrace change. This is especially true when industry expertise and technology is combined to offer superior value to customers.

While there undoubtedly remains a huge amount to do as the energy transition continues, I hope that the above demonstrates two critical aspects that apply to all parts of the oil and gas industry:

1) Technology will continue to create huge opportunities and, when deployed correctly, can unlock significant value for many market participants.

2) Industry expertise, if combined with the right customer-centric approach, can allow newer ideas to succeed, even if conventional wisdom implies it might be too much of a challenge.