The last century has seen the oil and gas industry transform the world and help lift billions out of poverty by providing cheap and abundant energy to the world. It has paved the way for modern economies to thrive and flourish. The last decade has, however, seen an increased concern about environment and sustainability, both by governments and the populace. Aptly, the oil and gas industry is seen to redefine and adjust course for its business models, investment opportunities, technology, and operations accordingly to positively contribute to the lowering of greenhouse gas (GHG) emissions. The magnitude of diversity, resources, skills, and scalability have always been the key strength of this industry to achieve efficiency and productivity. Increasing global population and expanding global economy is driving the energy demand; the challenge is now for the energy supply to fulfill the needs in an affordable manner while also addressing environmental concerns.

The energy transition performance of the new energy players such as Iberdrola, Enel, and NextEra underscores the impact of capital markets in driving growth and improving the value of their businesses in the green energy market. In a timespan of just 10 years, the combined capitalization of these companies has grown from $110 billion to $350 billion, showing an increase of more than 200%. In contrast, the aggregate capitalization for the mature oil giants—Shell, Chevron, ExxonMobil, and BP—have shrunk by 40%, from $980 billion to $570 billion, over the same period (McKinsey, 2021).

In this two-part series, we intend to present how the traditional oil and gas industry is transforming to meet the current and future challenges in energy security. There is little doubt that the industry is uniquely qualified to address the challenges at scale. Part one of this article series delves into insights about how exploration and production (E&P) companies are shaping themselves for the future energy industry.

E&P Companies

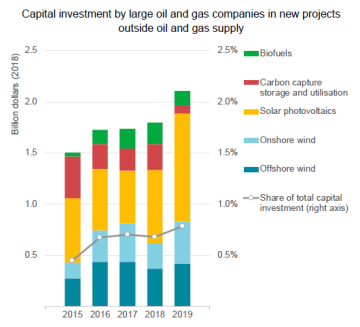

There has been an increasing trend of E&P spending redeployment toward low-carbon businesses outside conventional oil and gas investments, which includes solar photovoltaics, wind, electricity distribution, etc. (Fig. 1).

Fig.1—E&P spending redeployment in new projects outside oil and gas supply, toward low-carbon businesses. Source: IEA World Energy Outlook, Special Report, Jan 2020.

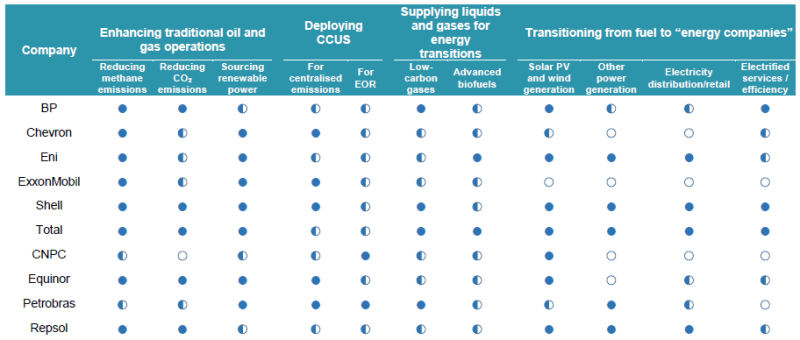

Large “oil and gas” companies are shifting to become “energy” companies. This definitely brings them out of their comfort zone, but also offers a path to handle transition risks. Figure 2 reflects investment and strategic responses to energy transitions by selected companies between 2015 and 2019. Companies not only continue to invest in new technology ventures and innovative partnerships in the strategic sector, but also find ways to make their existing processes leaner, efficient, and more sustainable. Moreover, E&P companies are diversifying their portfolio of projects in selected markets and geographies where existing policies and regulations can make projects attractive. Today, the next-in-energy portfolio for these companies focuses cardinally on reinventing the energy itself, to contribute to the sustainable development of the planet facing the climate challenge, and by probing the broader topics of emissions management, carbon capture, utilization, and Storage (CCUS) opportunities, and new energy investments.

Fig. 2—Activities and engagements of the selected oil and gas operating companies toward the energy transition between 2015 and 2019. Filled circles refer to active participation and spending in commercial projects; half-filled circles indicate minor engagements (i.e., strategy announcements, spending in research, etc.); empty circles denote limited information or lack of it. Source: IEA World Energy Outlook, Special Report, Jan 2020.

Emission Management

The yearning for greater return on investment and opaque risk associated with investment in low-carbon opportunities is increasingly becoming a function of climate resilience. As the transition risks associated with climate change permeate further into the market and shifting energy demands are better understood, oil and gas companies are flagging up to high-grade their portfolio to access the low-carbon market, counting on their incumbent technology, capacity, and pervasive connection. The industry is thus more focused on arresting carbon emissions from its production and transport operations.

European producers have been very aggressive with their targets. Equinor aims to cut emissions from domestic operations by 40% by 2030 with the target of near-zero emission by 2050. BP plans to achieve net zero carbon emission by 2050 and aims to tackle around 415 million tonnes of emissions—55 million tonnes from its operations and 360 million tonnes from the carbon content of its upstream oil and gas production. Likewise, Shell has revised its emission target to be net zero by 2050. TotalEnergies plans 25–40% cut by 2040, whereas Repsol plans to reduce its full emission intensity by 100% by 2050. Eni sets the massive target of 43% reduction in GHG emissions by 2025 (IEA World Energy Outlook, Special Report, 2020).

Besides European producers, various other companies aim to be committed to reduce their emissions. ExxonMobil targets flaring reduction by 25% as an emission reduction strategy. Chevron plans to reduce emission intensity in the order of 2–10% from all their oil and gas production operations between 2016 and 2023. PetroChina’s parent group CNPC targets to cut methane emission intensity by 50% by 2025 (PetroChina, 2020) and has become the first Asian national oil company (NOC) to set that target (Reuters, 2020).

CCUS Opportunities

CCUS opens up a new pipeline juncture for oil and gas companies to channelize existing industry technology to achieve negative emission targets. The industry has an opportunity to extend its core capability, to secure market position in readiness of the opportunities and myriad uses of CO2 emissions. These include as an industrial feedstock in methanol production, to enable absorption of CO2 in cement manufacturing, in the manufacture of hydrogen, or in the production of algae-based biofuels. It is to be noted that CO2 storage for enhanced-oil-recovery (EOR) purposes is more cost-effective than geological storage (IEA World Energy Outlook, Special Report, Jan 2020).

CCUS has become a key priority for the Oil and Gas Climate Institute (OGCI), which has 13 global companies as its members: BP, CNPC, Eni, Equinor, ExxonMobil, Chevron, Occidental, Pemex, Petrobras, Repsol, Saudi Aramco, Shell and TotalEnergies. OGCI is actively working toward developing large-scale commercially viable CCUS opportunities through five global operational hubs in Norway, UK, US, Netherlands, and China. Among the operators, Occidental has been aggressive with CCUS projects and injecting around 950 Bcf CO2 per year for EOR in the Permian assets of West Texas, which also will help to increase their hydrocarbon recovery by 10-25% (Hart Energy, 2020).

Chevron has invested $1 billion for CO2 storage projects in Canada (Quest CCS project in Athabasca oil sands) and Australia (Gorgon gas projects) (Macdonald-Smith, 2020). Equinor, TotalEnergies, and Shell partnered to launch the first-ever cross border, open-source CCS project named Northern Lights aiming to transport, capture, and store nearly 0.8 million metric tons/year CO2 and set to be operational by 2024. It can be scaled up to a total capacity of 5 million tonnes based on market demand (CCUS Around the World, IEA Technology Report, 2021). ExxonMobil has ⅕th of the world’s total CCUS capacity and presently captures 7 million tonnes of carbon per year (LeSage, 2020). Recently ExxonMobil announced a large-scale ambitious CCS project in Texas aiming to capture and store approximately 50 million metric tons/year of CO2 by 2030 from heavy industries around the Houston ship channel (S&P Global Platts, 2021). Repsol also has plans to undertake a CCS project at the Sakakemang natural gas discovery in Indonesia, to capture an estimated 1.6 metric tons of CO2/year. This trend is increasingly being observed for various other big and small E&P players.

New-Energy Investments

In the pursuit of decarbonization, transitioning toward cleaner energy sources, and progressively positioning themselves as becoming “energy companies,” the E&P players have ramped up investments into the renewable energy sector in recent years. As the energy industry evolves, backing next-generation renewable technologies allows firms to remain at the leading edge of the industry, thereby improving their reputation with stakeholders and tailoring opportunities that integrate with the company’s base portfolios. In summary, the investment activities of major oil and gas players in the renewable energy basket can be evidently seen to be spread across the following four key energy segments.

Solar Energy. Clean solar energy is a stable investment that can provide attractive financial returns, and major E&P companies have by now started to believe so, if not all.

France’s major, TotalEnergies, leads the game by already holding a solar portfolio of around 3 GW capacity and making solar a centerpiece of its strategy by furthering investment in a 2.3-GW solar project in India and an 800-MW solar plant project in Al Kharsaah, Qatar. The company is also establishing its presence on the Spanish solar market through two agreements with Powertis and Solarbay Renewable Energy to develop nearly 2 GW of solar projects.

Abiding by its purpose to power progress together with more and cleaner energy solutions, Shell seconds by expanding its solar footprint in locations such as US, where it has acquired 44% stake in one of the largest solar power firm Silicon Ranch (Qadir et al., 2021), and also in Oman and Australia, where it has developed solar farms in 25 MW and 120 MW capacities, respectively.

BP aiming to achieve net zero by 2050, continues its pursuit with a $200-million acquisition of Europe's largest solar developer Lightsource in 2017 (Sheppard and Raval, 2018; NS Energy, 2020) and aiming to deploy 10 GW new solar capacity by 2023. Repsol, another company that champions net zero emissions, acquired a 40% stake in Hecate Energy, currently holding a 40-GW solar portfolio in the US western hemisphere (Repsol, 2021).

Other companies such as Chevron, Equinor, and Eni are penetrating into the solar energy segment together with some of the NOCs. Saudi Aramco has installed 126,695 photovoltaic panels to feed 10.5 MW of solar energy (Saudi Aramco, 2020), thereby sharing the nation's commitment of scaling solar energy capacity to 27.3 GW by 2023. Brazilian Petrobras has also invested in setting up a 1.1-MW solar plant in Açu, Rio Grande do Norte state, to fulfil the energy requirements (Petrobras, 2021).

Wind Energy. Wind energy has gained traction among oil and gas majors dealing with routine price uncertainty and are far more relieved when these costs are diminished with the use of wind energy.

Equinor sets its course to being a sector leader in floating offshore wind with the Hywind Tampen, an 88-MW project to provide electricity for two North Sea offshore field operations. Equinor has four operational offshore wind projects (fixed and floating) of 1134 MW and 13 more at various stages of planning and development which can deliver up to 12 GW.

TotalEnergies is also a pioneer in multiple onshore and offshore wind projects with a capacity of 1600 MW in the UK, 30 MW in France, and around 2000 MW in South Korea.

Shell, already possessing offshore designs in its wind portfolio of 6 GW capacity, is further spreading its wings in the onshore market with its recent investment in four wind farms in the US. It has also partnered with Eneco to develop a 759-MW offshore wind project (Renewables Now, 2021).

Several mid-sized oil and gas companies like Dong (now Orsted), Gazprom, and Neste have chosen more radical transformations. The Indian noc, Oil and Natural Gas Corp. with an existing wind portfolio of 153 MW, is continuing its investment toward 2 GW onshore wind capacity (ONGC, 2021), parallel to its target of doubling hydrocarbon production by 2030. Saudi Aramco has installed the Kingdom's first ever onshore wind turbine at Turaif Bulk plant (Saudi Aramco, 2020). Russia’s Rosneft recently signed a pact with the Danish turbine group Vestas for wind power generation, as the oil company plans to partly power its $100-billion Arctic Vostok oil project by local wind generation (Neftegaz.RU, 2021). China’s CNOOC too is focused on offshore wind development and plans to spend 3–5% of its annual budget in this sector (PetroChina, 2020).

Electric Energy. As part of their diversified business composition, oil companies are betting on electricity to act as the primary means of delivering clean energy to gain potential return of their investments.

TotalEnergies purchased French battery manufacturing company Saft for $1.1 billion in 2016 (Pickl, 2019); recently launched France’s largest battery storage project in Dunkirk, a 61-MW capacity power hub; and also bagged Europe’s largest electric vehicle (EV) charge point contract in the Netherlands.

BP invested $165 million in US firm Free Wire and UK-based Chargemaster, both engaged in EV charging infrastructure. It further invested $20 million in StoreDot, an Israeli company which develops ultrafast charging batteries (NS Energy, 2020) and partnered with Chinese private equity group NIO Capital to invest in advanced mobility technology in China (Ward and Hook, 2018). BP also invested $7 million in a smart EV charging firm which connects EV chargers with the electricity grid using the Internet of Things (IoT), a process known as vehicle-to-grid or bidirectional charging (IOT News, 2021).

Shell announced its target to become the largest electricity company by 2035 (Crooks and Raval, 2020), has acquired UK-based electricity and gas provider First Utility (Qadir et al., 2021), and Europe’s biggest EV charging company NewMotion (NS Energy, 2020).

Geothermal Energy. Considering the intermittency of wind and solar, geothermal provides a critical cleaner energy resource option and is well poised to be an important contributor to the decarbonization portfolio. Last active geothermal participation from oil and gas industry was during 1970s and 1980s when Chevron, Texaco, and Unocal drilled hundreds of geothermal wells around the world but sadly exited due to high exploration cost and poor profit margins in comparison with conventional hydrocarbons. This trend is reversing sooner if not later, as oil companies gain back confidence to tap this niche power source and nurture geothermal resources with its technological advancements and experience in the art of extracting fossil fuels many miles below the surface.

Companies including the venture arms of BP and Chevron invested $40 million in Canadian geothermal company Eavor Technologies, a startup that aims to commercialize their proprietary closed-loop solutions that addresses the bottlenecks of large-scale geothermal adoption (CNBC, 2021; Offshore Technology, 2021). Eavor targets to provide power supply to 10 million homes by 2030.

With maiden and low investments seen from private firms, the NOCs attempt to gain pace. PetroChina, the listed arm of state-owned CNPC started geothermal development in northern China in 2019 and also recently participated in Kenyan geothermal resources development (PetroChina, 2020). A historic agreement for establishing India's first-ever geothermal field development project was signed by ONGC energy center with the Union Territory Administration of Ladakh and the Ladakh Autonomous Hill Development Council, Leh to build a 1-MW power generation capacity pilot.

The Way Ahead

The outlook presented above reflects the measures that many of the E&P companies in the industry are concretely taking to contribute toward a sustainable future while ensuring a secure energy supply for the generations to come. The landscape is changing at a fast pace and there are a lot of new developments that are not mentioned in the article, and/or have happened since the time this article was written. It is encouraging to see that these companies have taken upon themselves an active responsibility to become part of the solution to the environmental concerns.

Nonetheless, the issue is such that it needs combined efforts from a multitude of new and existing players. In order to fulfill the ambitious plans of E&P companies, the services sector has to be the enabler, coming up with new and necessary technologies. In the next part of the article, we will discuss and present how the services sector of the traditionally oil and gas industry is stepping up and playing its part; is it preparing itself for the future needs of the broader energy industry adequately? Stay tuned!