Coal and hydrocarbons have remained the primary source of energy for a few centuries now. With technological advancements coupled with advanced data analysis and subsurface characterization, both resources have become economic, feasible and reliable sources for energy security worldwide. Naturally, the geographical distribution of coal and hydrocarbons play a critical factor in controlling the energy market. China dominates the coal market by producing approximately 47% of total global output in 2019 (NS Energy). As for hydrocarbons, OPEC holds ~80% petroleum reserves and controls 50% of global oil supply (OPEC).

As we transition to address growing climate concerns, the energy industry is aggressively shifting towards less carbon-intensive energy forms. We see ambitious plans for electric vehicles (EVs), which necessitate secure and affordable supply of EV minerals.

Do we foresee or expect an EV market monopoly like that of OPEC? An EV cartel will have both short- and long-term implications on the pricing, affordability, and consistent supply guarantees. Any geopolitical imbalance or tensions will only worsen the import-export equilibrium and EV supply chain vulnerability. The article presents information for readers to understand where the EV mineral market stands, putting a special focus on the intricacies of lithium, an important mineral for EV batteries.

The EV Market

Electrification of transportation and availability of associated infrastructure has been one of the prime focuses of many of the countries that align their domestic energy policies with the climate goals. In USA, the Biden administration announced electrification of the federal fleet by 2030 together with goals to have EVs comprising 50% of new car sales. The EU aims for 100% vehicle sales to be emission-free by 2035. China’s latest mandate aims to have EVs comprising 40% of total car sales (Atlantic Council). The automobile industry is acting toward the same goal. For example, Audi and General Motor aim to stop selling petrol and diesel cars by 2033 and 2035, respectively (Nature).

The global EV market is projected to reach $567 billion by 2025 growing at compound annual growth rate of 22% (Businesswire). Furthering the ambition of EV adoption will require additional supply of critical minerals as we “shift from a fuel-intensive to a material-intensive energy system.” EV batteries need lithium, nickel, cobalt, manganese, graphite, and iron. Vehicle drive trains need substantial amounts of rare-earth-element (REE)-based permanent magnets to transfer stored battery power into movement. Charging infrastructure will demand massive amounts of copper wiring to offer confidence to customers in their ability to access charging points and travel safely. Without major technological advances, EVs will lead to heightened demand for these strategic minerals. It is possible that access to these components will be used, as oil has been, for energy “statecraft” (New Security Beat). Financial Times also shares the same view: “While it is unlikely to lead to military conflict, the tensions, especially with China, over who will control the resources and technologies that will underpin electric cars will be heightened.”

The EV Minerals

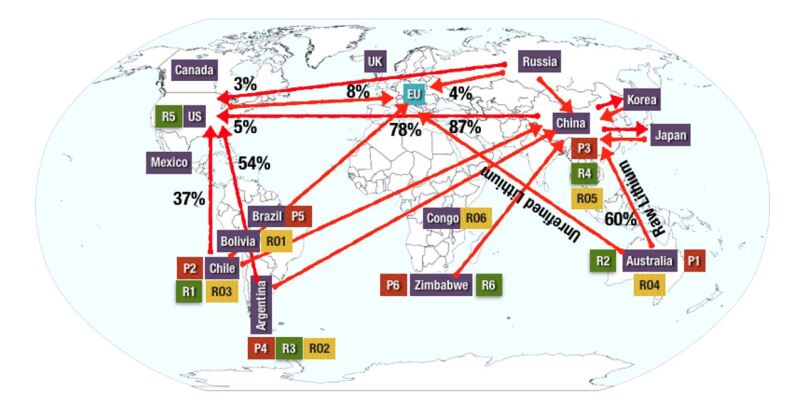

One needs to consider the availability of the necessary minerals to fuel the EV transition. The countries with most of these essential mineral reserves and processing capabilities are the ones that will lead the game and steer the future of EV business in the energy transition. Figure 1 below shows the share of the top three countries in reserves, extraction, and processing of some essential EV minerals in comparison to hydrocarbons.

A clear trend from Fig. 1 can be observed where China is dominating the processing part of the EV mineral chain. China has identified the increasing demand of EV metals and minerals as a geostrategic and geopolitical opportunity. For example, the country controls roughly 60% of REE extraction and 80% of processing and China’s National Development and Reform Commission has identified REE as a strategic resource since 2011 (Scientific American). A taste of the repercussion of such a monopoly was felt when following a territorial dispute over the Senkaku Islands in 2010, China imposed a 40-year REE export ban on Japan which used to be one of the prominent buyers of China’s REE (CNBC).

Similarly, cobalt is on the list of retaliatory tariffs that the US has levied against the Chinese government (Metal Bulletin). Higher tariffs could reroute Chinese cobalt to EU markets leading to the US searching for alternative supply. Newly introduced US legislation promotes the production increase of EV materials and focuses on identifying foreign-sourced critical minerals that could increase US geopolitical vulnerability. Such risks rightly highlight the sensitive geopolitical situation linked to minerals relevant to EVs.

The Lithium Story

Commercial lithium arises from two major sources: underground brine deposits and mineral ore deposits. The extraction process of the former consists of pumping mineral rich brine from high-salinity surfaces in desert, and then evaporating 95% of water using sunlight over a period of months. The lithium is then separated from its residual product through chemical treatment to create a solution called lithium carbonate, which is then processed and used (Bell 2020).

The second method of extraction is rock mining. This technique is characterized by its higher energy demands and additional material required to conduct the processing, even though rocks contain a higher concentration of lithium. The reason this alternative needs more energy is due to a double heating process that the rocks have to undergo. First, they are heated to 2012 F, then crushed and mixed with sulfuric acid, and heated once again. The last steps consist of adding sodium carbonate, heating, and filtering the solution to be left with the end product.

Lithium Value Chain

IEA projects that lithium demand in 2040 will be 42 times higher relative to the 2020 level to achieve battery demands of a sustainable development scenario. Analysis by Benchmark Mineral Intelligence indicates a 26,000-metric ton lithium supply gap in 2021, which they expect to grow to 1.1 million metric ton by 2030.

The most common place where lithium can be found is in natural salt brines, mineral springs such as pegmatites, and igneous rocks. As per US Geological Survey (2021), global lithium resources are estimated to be around 86 million tonnes, and are mainly concentrated in Bolivia, Chile, Argentina, and Australia, in decreasing order.

A country’s lithium resources differ from its reserves. Lithium resources are what lie underground, whereas lithium reserves are deposits that can be exploited. When it comes to reserves, Bolivia doesn’t rank in the world’s top ten countries. Chile ranks the highest, possessing 8.6 million tonnes in reserves, followed by Australia, with 2.8 million tonnes. It is important to note that the lithium reserves found in Bolivia, Chile, and Argentina, requires extraction through brine, whereas all of Australia’s lithium production is from lithium minerals, chiefly spodumene.

While more than half of the world's lithium production comes from Australia, China, by far, is the biggest processor of minerals including lithium, nickel, cobalt, copper and rare earth metals, making it stand as an elephant in the room. China’s continuous investment in the lithium industry in the past decade has also made it surpass the US in lithium production to acquire a place immediately next to Chile. The extracted lithium is mainly shipped to China, where 90–95% of the cathodes and anodes needed for batteries are produced. Zimbabwe, Japan, and South Korea also supply lithium to China, but in extremely low proportions. At present China’s lithium carbonate is mainly exported to South Korea (52%), Japan (30%), and the US (5%), whereas lithium hydroxide is mainly exported to South Korea (59%) and Japan (36%). South Korea accounts for almost half of the world’s total production of rechargeable batteries; while acting as the battery powerhouse, its heavy reliance on imports of raw materials and other rare earth metals from China makes it vulnerable to trade tensions and geopolitical shocks.

Companies and countries can build their EV gigafactories wherever they want, but they can’t change the geology of the Earth’s crust. As per US Geological Survey (2021), the major imports of lithium to the US came from Argentina (54%), Chile (37%), Russia (3%), and China (5%). The US may have many of the minerals at home, but permitting uncertainty, costing finance, and cheap Chinese commodities have marginalized US mining, which resulted in US fulfilling its import dependency of lithium-ion batteries from China (80%), South Korea (9%), and Japan (3%). The EU on the other side stands at the crossroads of dichotomy. The rush for meeting the energy demand can’t square with the desire to be a world leader in climate. The EU is not a lithium producer and meets most of its lithium requirements from Chile (78%), US (8%), and Russia (4%). While there are lithium mines being developed in Europe, the region is not really on the map when it comes to refining lithium, making it dependent on China for the processing.

Currently, Africa only has a small capacity for lithium mineral processing, further refining of lithium chemicals, or manufacturing of battery components. This leads to a scenario where the mineral concentrate is exported (value is added outside of Africa) and products using lithium-ion batteries are then imported back. Many African countries, most notably Zimbabwe, Namibia, Ghana, Democratic Republic of Congo, and Mali, have lithium resources and hence the potential for lithium mines. Nevertheless, there is comparatively less efforts in the valuable stages further along the supply chain and more consideration is due.

The shift towards a cleaner future has a lot riding on a smooth supply chain of minerals and other key components to make the electric vehicles, which are presently dominated mainly by China. The current situation in Ukraine has already shown the impact of hostilities and geopolitics on the flow of fuels and other commodities. Similar risks can be underpinned when it comes to the global EV market, especially lithium.

Risks and Geopolitics

Australia, Chile, and China are the top three countries in lithium extraction. Lithium chemical production is highly concentrated in a small number of regions, and China cements the dominance contributing 60% of global production (over 80% for lithium hydroxide). Lithium prices climbed sharply when China and Argentina teamed up in an partnership, making lithium buyers around the world nervous, as the oligopoly turns even smaller (Oil Price). Fitch Solutions Country Risk & Industry Research states “…the growing rivalry between China and the US (and their allies or areas of influence) pose rising and significant risks to the lithium sector, as it could disrupt demand and trade flows when tensions rise.” In the US, California announced major lithium mining investments in the state’s Imperial Valley to ease the US’ dependence on Chinese-refined lithium but the volume is still insufficient to meet the growing demand (Oil Price).

China’s dominance in the lithium processing business possesses significant geopolitical risk to the EV adoption by the US and its allies. More than 90% of the spodumene produced by Australia is exported to China to be processed into lithium carbonate and lithium hydroxide, which is mostly for use in mainland China (IHS Markit). The remaining processed lithium products are exported to South Korea and Japan. The brine-extracted in Latin American lithium is more expensive. It is to be noted that 43% of Chilean lithium carbonate was imported by China in 2021. The US imports 43% of its lithium carbonate from Chile and the remaining from Argentina and lithium hydroxide from Russia. The Latin American governments are consistently under pressure to pursue state ownership and domestic value addition in the Chile-Bolivia-Argentina lithium business.

Amid all conventional lithium sourcing tensions, a promising news for the oil and gas industry is that Vancouver, Canada-based Standard Lithium is developing a technology capable of extracting up to 90% of lithium from oilfield brines without the need for the evaporation ponds of the conventional evaporative process.

There is growing interest in securing diversified supply options, but surprisingly there’s no overarching international governance framework for critical minerals. To ensure reliable and sustainable mineral supply chains, it is cardinal that countries build international cooperation and improve coordinated policy action.

The Story Forward

Humans have consistently risen to challenges in the past and the expectation is they will again in the case of lithium’s story. Advancement in technology can be a key factor. Waste disposal or recycling needs to be taken into consideration when talking about EV minerals. Unlike hydrocarbons, batteries can be recycled and reused. Battery researchers and manufacturers have traditionally not focused on recycling but rather on improving battery longevity and charging capacity. This is changing gradually and work is done together with battery manufactures and recycling plants to establish and streamline the process from manufacturing to breakdown (BBC).

Just as the world has seen demand and supply volatility in oil and gas in the past decades, one can expect to see such volatility linked to minerals such as lithium as well, making it a vital resource to keep an eye out for in the near future. All indicators reflect a growing demand for lithium to ease the world toward energy transition. Conversely, the supply side, being already tight, gets further complicated with geopolitics playing a crucial role to drive the market.

This is only the story of lithium, but a similar story holds true for other critical minerals like nickel, cobalt, and copper when it comes to understanding the global value chain of EV and shedding light on the true face of energy transition. To say the least, there will be interesting times ahead.