Asia is the largest and the most populous continent in the world covering an area of 44,579,000 sq. km, about 30% of Earth's total land area, and 8.7% of the Earth's total surface area. Its 4.5 billion people form roughly 60% of the world's population. To understand the intricacies of this vast and diverse continent, it is a common practice to categorize the constituting countries as per the subject—economic development—under discussion.

One such categorization is “Tiger Economies.” It is the nickname given to the economies of Southeast Asia. The tigers are South Korea, Taiwan, Hong Kong, and Singapore. With the injection of large amounts of foreign investment capital and huge push from government and corporate sector, these economies grew substantially between the late 1980s and early-to-mid-1990s.

In this YPGT article, we discuss “Tiger Cub” economies and their oil and gas potential.

The term Tiger Cub Economies refers to the economies of five recently industrialized countries in the Southeast Asia: Indonesia, Malaysia, the Philippines, Thailand, and Vietnam. These countries try to follow the same economic path as the four Asian Tigers. Walking on the same growth and maturation path, the goal for these countries is to eventually evolve into a Tiger Economy.

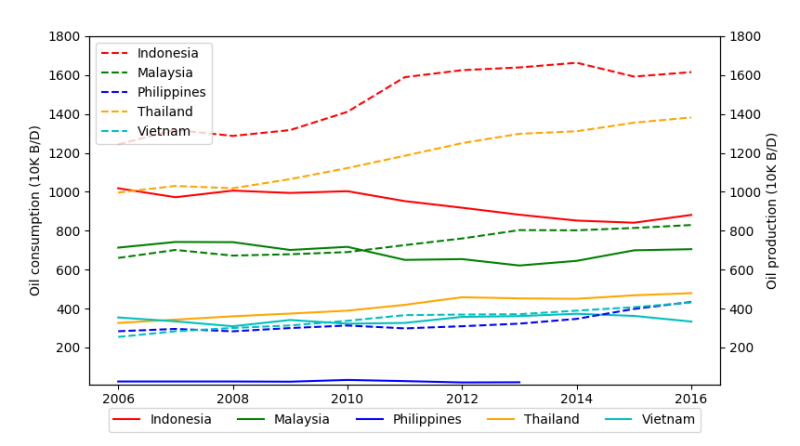

Although the Tiger Cubs have a rich base of mineral resources, many of the individual countries have increased their energy import dependency and have the same trend—increasing consumption and declining oil production.

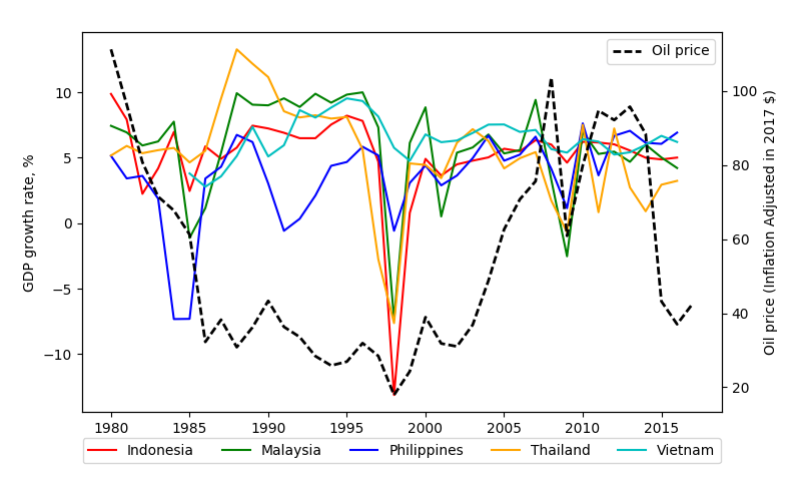

Figure 2 shows comparison between oil production and consumption for the Tiger Cub countries during 2006–2016. Figure 3 shows the Gross Domestic Product (GDP) growth rate of these economies from 1980 to 2016. The dependence of these economies on the oil and gas sector is evident. The GDP of these countries dropped every time the oil and gas sector faced a downturn characterized by a significant drop in oil prices.

To acquaint our readers with the unique Asian culture and spirit, let’s travel to each of the Tiger Cub countries.

VIETNAM

The Socialist Republic of Vietnam is the world’s 14th most populous country and the ninth most populous Asian country. Its capital city has been Hanoi since the reunification of North and South Vietnam in 1976, with Ho Chi Minh City the most populous.

According to the BP Statistical Review of World Energy 2017, Vietnam ranked 28th among 52 countries that have oil and gas potential in the world. By the end of 2015, the proven crude oil reserves of Vietnam were approximately 4.4 billion bbl and ranked first in Southeast Asia, while the proven gas reserves were about 0.6 trillion cubic meters (Tcm) and ranked third in the Southeast Asia (after Indonesia and Malaysia).

Since the first oil at Bach Ho field in 1986, the Vietnam National Oil and Gas Group (Petrovietnam) has made significant progress and strived to be the backbone of the national economy. It has built an integrated oil and gas value chain, including exploration and production, processing, and oil and gas services (Trung, et al., n.d.).

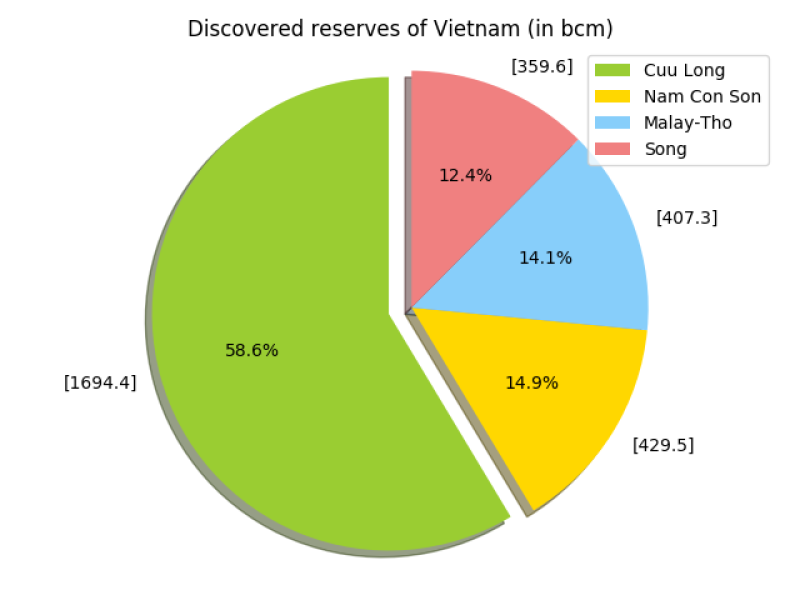

The four major basins of Vietnam are Cuu Long, Nam Con Son, Malay-Tho Chu, ad Song Hong. Figure 4 shows their respective contribution to the total discovered reserves of the country. Bach Ho (White Tiger), Rang Down (Dawn), Dai Hung (Big Bear) and Su Tu Den (Ruby) are some of the largest oil fields located offshore in the Cuu Long and Nam Con Son basins (Trung, et al., n.d.).

In the past few years, Vietnam has made efforts to speed up exploration and field development projects. From 2011 to 2015, 36 new fields and structures were put into operation.

Overall Energy Outlook: According to the Business-as-usual (BaU) scenario, by 2035 the total final energy demand will be nearly 2.5 times higher than in 2015. To meet this demand, the import share of total primary energy supply is due to increase to 58.5%, which is a risk for the country’s energy security (Danish Energy Agency, 2017).

Did you know? Among the recently discovered oil fields in Vietnam, the largest is Su Tu Den with about 100 million tons of oil in place. However, this is only one-third of the first field discovered in 1986—Bach Ho. |

|---|

MALAYSIA

Malaysia is a federal constitutional monarchy in Southeast Asia. It consists of thirteen states and three federal territories, separated by the South China Sea into two similarly sized regions, Peninsular Malaysia and Malaysian Borneo.

With a population of over 30 million, Malaysia is the world's 44th most populous country. Since the 15th century, Malaysia is one of the countries that control the Strait of Malacca and hence it became the most important port in the Malay Archipelago. Until now, international trade plays a key role in Malaysia’s economy.

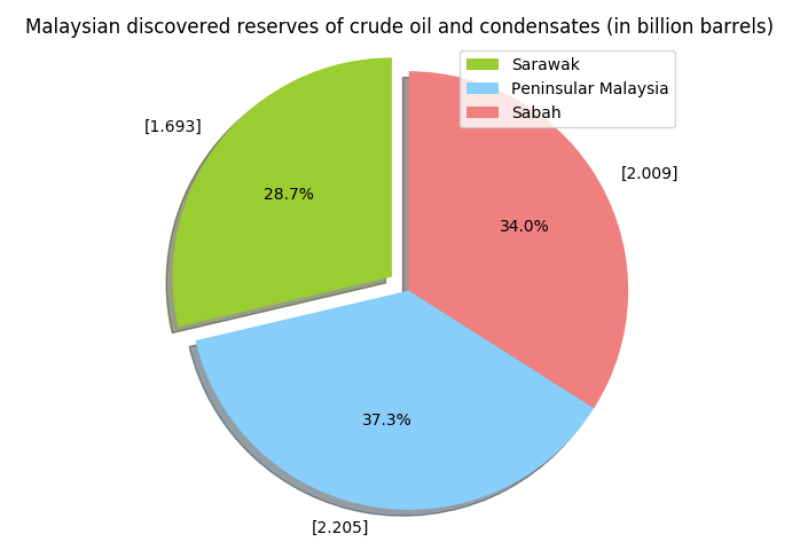

Malaysia has two distinct parts: Peninsular Malaysia in the western part and the states of Sabah and Sarawak in the eastern part. Thus, the producing basin is divided into three: the Malay basin in peninsular Malaysia, Sarawak basin, and Sabah basin (EIA, 2017).

Figure 5 displays the contribution of each basin to the country’s total discovered oil reserves. According to Energy Commission of Malaysia, in 2015, peninsular Malaysia recorded the highest value of 2.2 billion bbl or 37.3% of total reserves, while Sarawak had the highest natural gas reserves with 52.9 Tcf in the same year.

There are more than 160 oil fields in Malaysia, however, a significant part of Malaysian oil production comes from Tapis oil field in the offshore Malay basin. The oil from Tapis field has become the crude oil pricing benchmark, owing to its light weight (43–45o API gravity) and sweetness (0.03% sulfur content) (Jaipuriyar and Yip, 2013).

According to EIA, Malaysia is the second largest producer of oil and natural gas in Southeast Asia. The oil and gas industry has provided around 30% of the country’s revenue through its national oil company called Petronas, which leads all oil and gas activities in Malaysia since 1974 both in upstream and downstream sectors.

The recent fall in oil prices has put the Malaysian revenue at risk with oil-related revenue contribution down to 14.6% in 2017 (41% in 2009). The government decided to diversify its revenue by introducing a government service tax and reducing the dependency on oil-related revenue (Bloomberg, 2017).

Overall Energy Outlook: Malaysia has been very successful in developing its upstream gas sector. Around 17 Tcf of gas has been discovered between 2012 and 2016 in offshore Sarawak. The new discoveries provide fresh gas feedstock to sustain East Malaysia's LNG exports undertaking and new projects.

While Malaysia is expected to continue exporting its surplus gas, its reliance on oil imports is on the rise. Malaysia turned into a net oil importer in 2013 as its demand for oil products surpassed its domestic oil production. The reliance on oil imports is expected to grow (Wood Mackenzie, 2017).

INDONESIA

The world’s largest archipelago, Indonesia, comprises 17,508 islands. It is the fourth most populous country in the world, with 250 million diverse inhabitants.

Indonesia’s economy, the largest in Southeast Asia, was formerly strengthened by oil export during the 1970s to 1980s (Asian Development Bank, 2016), but gradually over time, it transitioned to a net oil importer (Statistics Indonesia, 2016). Indonesia joined the Organization of the Petroleum Exporting Countries in 1962, but had to suspend its membership in January 2009 due to the continuous decline in its domestic oil production.

According to Indonesia’s Ministry of Energy and Mineral Resources (MEMR), Indonesia contains 3.69 billion bbl of proven oil resources, and 101.54 Tcf of proven natural gas reserves. These make Indonesia the 10th largest natural gas exporting country and the 4th largest LNG exporter (MEMR, 2014).

Two of the most recognized oil and gas achievements are East Natuna natural gas discovery, which is the largest discovery in Southeast Asia in the last two decades, and Duri steamflood enhanced oil recovery, which is the biggest steamflood operation project in the world.

Indonesia is recognized as the first country to introduce the production sharing contract model (Putrohari et al., 2007). Currently, Indonesia has started implementing the new Gross Production Split contract system to attract more investors. Earlier this year, Indonesia’s state-owned company Pertamina took over Indonesia’s largest gas block Mahakam.

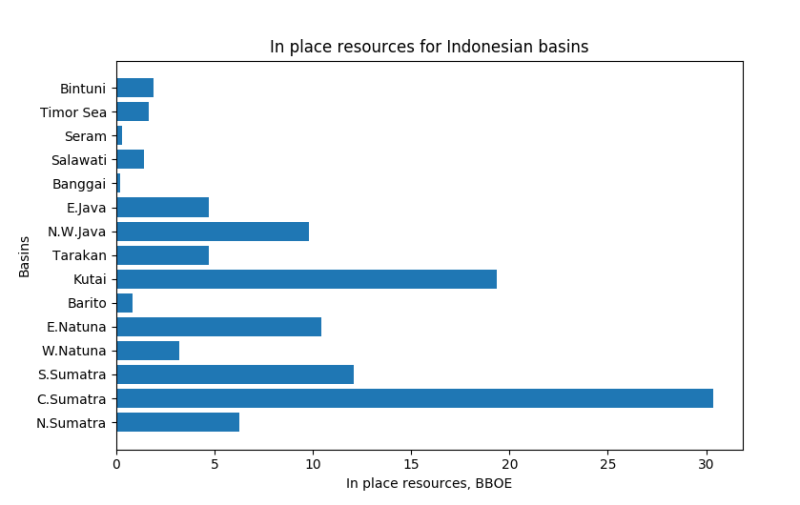

There are 15 petroleum basins in Indonesia. Figure 6 indicates the distribution of in-place resources among them.

Overall Energy Outlook: Oil is the major contributor to the energy demand of Indonesia. Based on moderate GDP growth assumption of 5.6% per year during 2015-2050 and average population growth of 0.8% per year, the national final energy demand will reach 238.8 MTOE in 2025 for BaU scenario.

The demand in 2025 shows 1.8 times increase with the annual growth of 6.4% compared to the final energy consumption in 2015 of 128.8 MTOE. The final energy demand will be increasing up to 682.3 MTOE in 2050. The average energy demand growth during 2015–2050 is around 4.9% per year (Secretariate General of National Energy Council, 2016).

Did you know? Indonesia and Malaysia are two of the 17 “megadiverse” countries, according to Conservation International. Megadiverse countries possess a vast number of species–many found nowhere else. |

|---|

PHILIPPINES

The Republic of Philippines consists of about 7,641 islands that are categorized broadly under three main geographical divisions from north to south: Luzon, Visayas, and Mindanao. The capital city of the Philippines is Manila and the most populous city is Quezon City, both part of Metro Manila. It has been a Spanish colony for more than three centuries and is named after a 16th century Spanish King – King Philip II of Spain.

The Philippines is a net energy importer in spite of low consumption levels compared to its neighbors. The country produces small volumes of oil, natural gas, and coal. In 2011, total primary energy consumption in the Philippines was roughly 1.3 quadrillion British thermal units (Btu). Oil constituted roughly 41% of total consumption, while natural gas and various renewable sources contributed 18% (EIA).

Even though the first well, Toledo-1, was drilled in 1896 in the Cebu Island, the first major oil discovery was in 1989—the Camago-Malampaya trend by Occidental Petroleum in Palawan.

Apart from Malampaya, other smaller oil fields have been found offshore along northwest Palawan in the vicinity of Malampaya, commencing with the first important oil discovery at Nido in 1976. A handful of smaller fields were likewise found on this stretch of coast in subsequent years. However, in total the subject fields have only aggregated about 50 million bbl of production since 1979 (Oil and Gas Journal).

Recently, the Department of Energy and China International Mining Petroleum Company have jointly declared an oil field in Alegria town of Southern Cebu to be commercially viable, with reserves of oil and natural gas that could last until 2037. Alegria was found to have an estimated 27.93 million barrels of oil (MMBO), with a possible production recovery of 3.35 MMBO, or 12% of total oil in place. Alegria also has natural gas reserves of about 9.42 Bcf, with the recoverable resource estimated at 6.6 Bcf, or about 70% of total natural gas in place. Though not as big as Malampaya, which had about 2.7 Tcf of natural gas, Alegria's gas will help boost supply in one of Asia's fastest-growing economies where energy demand is expected to triple by 2040 (SunStar Philippines).

Overall Energy Outlook: The latest Philippines Oil & Gas Report from BMI forecasts that the country will account for 1.26% of Asia Pacific regional oil demand by 2015, while providing 0.55% of supply. The Philippines is now at sixth place in BMI’s composite Business Environment league table. The country ranks sixth, just ahead of Pakistan, in BMI’s updated upstream Business Environment ratings, reflecting a reasonable resource position and a better-than-average output growth outlook (Philippines Oil and Gas Conference).

Did you know? More than 7,000 islands make up the Philippines, but the bulk of its fast-growing population lives on just 11 of them. |

|---|

THAILAND

Thailand, officially the Kingdom of Thailand, is a country in Southeast Asia with coasts on the Andaman Sea and the Gulf of Thailand. Thailand is the world's 50th largest country by total area and the 21st most populous country. The capital and largest city is Bangkok. Although nominally a constitutional monarchy and parliamentary democracy, the most recent coup in 2014 established a de facto military dictatorship.

Thailand has been an oil and gas producer for many decades, with falling reserves amid rising domestic petroleum consumption. Proven oil reserves in Thailand is estimated at around 453 million bbl, while proven natural gas reserves stood at about 10.1 Tcf. PTT Exploration and Production (PTTEP), the upstream subsidiary of state-owned PTT Public Company Limited (PTT) and Chevron, is the dominant player in the Thai petroleum industry. Total, Mitsui, and BG Group are other big foreign companies with a presence in Thailand's petroleum sector (Rig Zone, 2018).

Thailand's upstream oil and gas production is predominately sourced from two offshore areas in the Gulf of Thailand: The Pattani Basin and the Malay Basin. The fractured nature of the offshore geology means no one field or area dominates reserves or output; instead the majority of production is provided by thousands of separate (but relatively homogenous) reservoirs spread across the two basins (Mackinzie, 2018).

In 2011, Thailand produced an estimated 393,000 B/D of total oil liquids, of which 140,000 B/D was crude oil, 84,000 B/D was lease condensate, 154,000 B/D was natural gas liquids, and the remainder was refinery gains. Thailand consumed an estimated 1 million B/D of oil in 2011, leaving total net imports of 627,000 B/D, and making the country the second largest net oil importer in Southeast Asia.

Although Thailand has a relatively small total of proved natural gas reserves, it has been able to produce a significant amount of natural gas given its level of reserves. Thailand only had 238.3 Bcm of proved natural gas reserves as of 2014, but it was able to produce 42.1 Bcm of natural gas in 2014. While the country’s natural gas production has been consistently growing over time, domestic production alone is not able to satisfy the demand. Therefore, Thailand has historically been an importer of natural gas (World Energy Council, 2018).

Overall Energy Outlook: The Thailand Ministry of Energy launched a set of five energy policies, namely Thailand Integrated Energy Blueprint (TIEB), in the year-end of 2015 addressing the changing and challenging contexts that Thailand will encounter in the future while keeping the balance between financial cost and benefit and the potential environmental impacts. According to TIEB Energy Outlook, crude oil and natural gas will still be the main sources of Thailand’s primary demand in 2050. Crude oil demand is expected to increase at 1.8% per year and natural gas would grow at 1.18% per year (Traivivatana, Wangjiraniran, Junlakarn, et al. 2017).

Did you know? Thailand is the only Southeast Asian country never to have been colonized by a European power. |

|---|

CONCLUSION

Although Tiger Cub economies try to follow the same economic scenario as the four Asian Tigers, they are characterized by more heterogeneity in their energy patterns. They are going to become increasingly reliant on energy imports due to tremendous population growth and rapid industrialization.

The future of petroleum industry in the region is not straightforward. Even though many oil fields have already matured (Bach Ho in Vietnam, all Indonesian and vast majority of Malaysian fields), the Tiger Cubs can try to shrink the gap between oil consumption and production by investing in exploration in promising deepwater areas in Thailand and Vietnam. To prevent the oil output decline, Malaysia is already applying various EOR techniques on its brown fields (OGF, 2015). Similarly, Indonesia is trying to increase oil production from its big Kaji Semoga onshore field by applying a novel pillar fracturing technology (JPT, 2018).

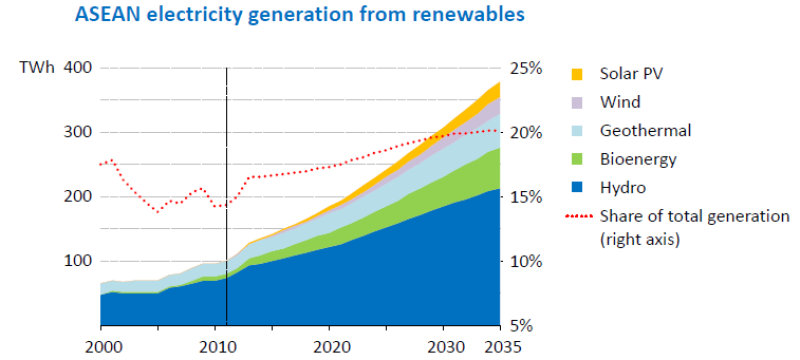

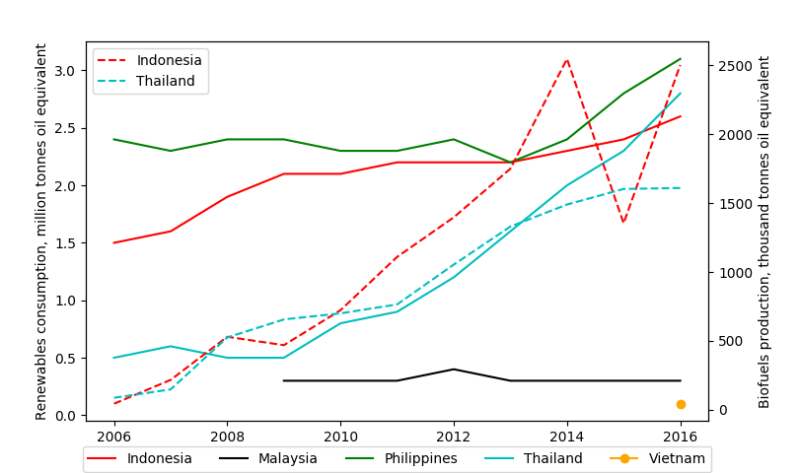

To meet the growing demand, Tiger Cub countries need to diversify their energy portfolio through renewable energy sources. Figure 7 indicates current and forecasted electricity generation levels in ASEAN from renewables, while Fig. 8 shows renewable energy consumption and biofuels production in each of the Tiger Cubs.

Situated near the Asia Pacific “Ring of Fire,” many countries have great geothermal potential. For instance, the Philippines and Indonesia are already the world’s second and third largest producers of geothermal energy for power generation. Indonesia can still grow its geothermal energy output: The country has the largest estimated geothermal energy reserves in the world, approximately 27 GW, or 40% of the global total. Indonesia’s government, through MEMR, is also targeting to increase the share of new renewable energy, including development of coal bed methane, to account for as much as 23% of the total national energy mix by 2025 (MEMR, 2014).

To overcome their energy challenges, all Tiger Cub economies should increase cooperation, both intraregionally through ASEAN, and internationally. Developing policies to improve energy efficiency, diversify energy sources, and attract more investments will allow Tiger Cub economies to enhance energy security, affordability, and sustainability in the long term.

Country | National Oil Company | SPE Sections | Important Industry Events | Must-See Local Attractions |

|---|---|---|---|---|

Vietnam | Petrovietnam | Vietnam Section located in Ho Chi Minh City, Vietnam | Halong Bay (UNESCO World Heritage) | |

Malaysia | Petronas | Sarawak, Terengganu, Kuala Lumpur, and Sabah

| Offshore Technology Conference Asia; SPE Asia Pacific Digital Week Symposium |

|

Indonesia | Pertamina | Sumatra, Balikpapan and Java | Oil and Gas Indonesia (OGI); and SPE/IATMI Asia Pacific Oil & Gas Conference and Exhibition (not annually in Indonesia)

|

|

Philippines | Philippine National Oil Company (PNOC)

| Philippines Section located in Manila, Philippines | Puerto Princesa Subterranean River National Park | |

Thailand | PTT Exploration and Production Company Limited (PTTEP)

| Thailand section located in Bangkok, Thailand

| IADC/SPE Asia Pacific Drilling Technology Conference and Exhibition (Rotates between Singapore and Thailand)

|

|

References

Government of Indonesia, Ministry of Energy and Mineral Resources (MEMR), 2014. Handbook of energy and economic statistics of Indonesia, Jakarta.

Putrohari, R. D., Kasyanto, A., H., S. & A., R. I. M., 2007. PSC term and condition and its implementation in South East Asia region. Proceedings. Indonesian Petroleum Association, Thirty-First Annual Convention and Exhibition, May.

Statistics Indonesia (BPS), 2016. Press release: Economic growth of Indonesia fourth quarter 2015. Jakarta.

Secretariate General of National Energy Council. Indonesia Energy Outlook 2016.

Trung, L. V., Quoc Viet, T. & Chat, P. V., n.d. An Overview of Vietnams Oil and Gas Industry. Petroleum Economics and Management, pp. 64-71.

Traivavatana, S., Wangjiraniran, W., Junlakarn, S. et.al. 2017. Thailand Energy Outlook for the Thailand Integrated Energy Blueprint (TIEB). Energy Procedia. 138 (399-404).

|

|

|

|

|

| Zafar | Mandzhieva | Lakhanpal | Mamat | Baskoro |

Anindito Satrio Baskoro is a geologist-basin modeler at Geochemistry and Petroleum System Group – Exploration Division of Research and Development Center for Oil and Gas Technology “Lemigas” Indonesia. He holds an MSc from the Norwegian University of Science and Technology in petroleum geosciences with a specialization in petroleum geology, and a bachelor’s degree in geological engineering from Bandung Institute of Technology, Indonesia. He will be joining Chevron Basin Modeling Center of Research Excellence at Texas A&M University, US, as a PhD student of Geology.

Nur Suriani Mamat is a tutor of petroleum engineering at the Universiti Teknologi Malaysia. Currently, she is doing her PhD, which is funded by Government of Malaysia, in wellbore instability at the Norwegian University of Science and Technology. Her research interests include static testing on drilling mud rheology, dynamic looping in cuttings lifting, constructing knowledge modeling, and deep learning.

Asif Zafar is a strategy consultant at Accenture. Before this, he worked for 5 years at Halliburton designing drill bits for oil and gas companies in South Asia. He holds an MBA from the Indian School of Business and a bachelor’s degree in petroleum engineering from the Indian Institute of Technology (Indian School of Mines).

Radmila Mandzhieva is a content creator with SPE TWA. She graduated from Norwegian University of Science and Technology with a master’s degree in petroleum engineering and holds a bachelor’s degree from Gubkin University in Moscow. Her interests include pore-scale modeling and digital rock analysis, as well as enhanced oil recovery methods and reservoir simulation.

Vikrant Lakhanpal currently works as production engineer at Proline Energy Resources. He also volunteers as assistant director at Well Engineering Research Center for Intelligent Automation at University of Houston. He holds a master’s degree in petroleum engineering from University of Houston and a bachelor’s degree in petroleum engineering from University of Petroleum and Energy Studies, India.