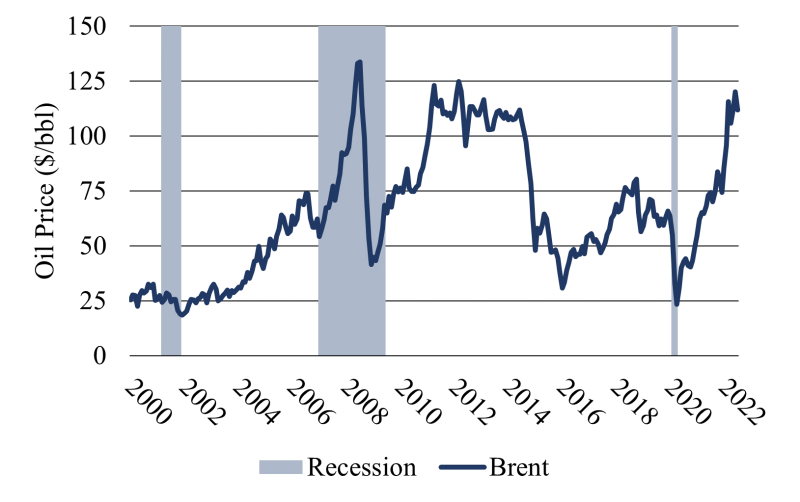

While it may feel like the oil and gas industry has just recovered from the last COVID-induced crash, there are already dark clouds gathering on the horizon. Recent recession worries have weighed on energy prices, with Brent dropping from $128 per barrel in June to $106 in August. While there are several definitions, the US National Bureau of Economic Research defines a recession as when a range of economic indicators such as income, employment, and industrial production decline, portending slower or negative economic growth with subsequent lower demand for many commodities. Oil prices are notoriously volatile because of highly inelastic short-term supply and demand, so it is not surprising that a potential economic downturn would trigger concern in the industry. Over the past three US recessions, Brent oil prices fell by 35%, 70%, and 65% from peak to trough, respectively (Fig. 1).

Oil Prices Can Take Years To Recover Following a Crash

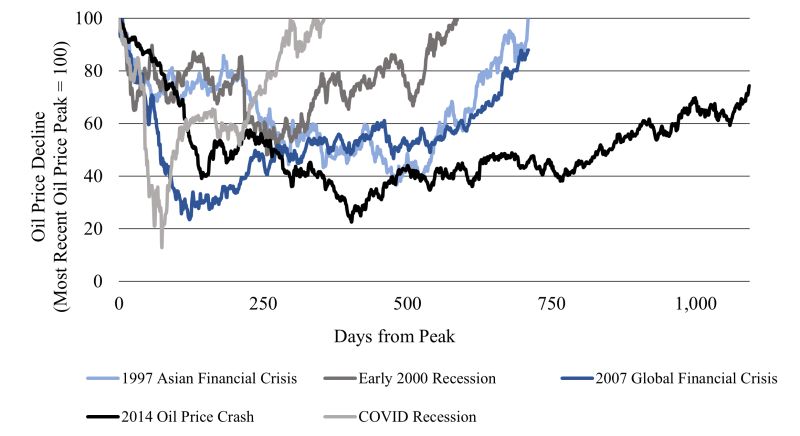

Recessions often impact a wide range of energy-consuming activities. Total vehicle miles traveled has fallen in four of the last seven US recessions. Additionally, both industrial production and power demand have declined in past economic downturns. These show that recessions can have a lasting impact on energy prices (Fig. 2).

Not all oil price crashes are the same; they vary in both severity and duration. For example, the 2014 crash was a clear outlier because it was driven by supply-side, not demand-side factors—prices did not return to the 2014-highs until 2022. Looking at just demand-side downturns, however, there is still a substantial dispersion between the very deep, but rapidly recovering COVID crash seen in 2020–2021 compared to both the 1997 and 2007 downturns that lasted roughly 2 years. The severity and duration of a recession can have a sustained negative impact on commodity prices including oil and gas.

A Recession Is Unlikely in the Near Term, But Uncertainty Remains

While economic growth has slowed, the US does not appear to be on the brink of a recession. Looking globally, depending on the region and the time frame, some financial forecasters project the likelihood of a recession ranging from 25% to 60%—driven by high energy prices, inflation, and rising interest rates. In the case of the US, the world’s largest consumer of oil and gas, the consensus leans toward a recession being unlikely anytime soon. For example, one forecast from Deloitte pegs US recession risk at only 15% in the next couple years.

Another major concern is China. Another large energy consumer, it faces idiosyncratic economic risks stemming from its Zero COVID policy. A downturn in China could not only impact its sizeable domestic oil demand, but also have knock-on effects on other countries. China is the second largest economy globally and the largest trading partner of developed economies like the US. The International Monetary Fund expects Chinese economic growth to slow, but remain positive. However, the country remains a key source of uncertainty for economic growth and energy demand.

Preparing for the Next Oil Price Crash

While predicting future oil prices can seem like a fool’s errand, understanding the likely severity of a potential recession is critical for the industry to prepare for its impact on energy prices. Between 2014 and 2016, US producers drilled 80% less wells, and cut capital spending by a similar amount in 2020. An industry pullback could have significant ramifications for production over the next few years.

Right now oil prices remain elevated, drilling expenditures are restrained, and economic growth is anemic but positive. That could all weigh on oil demand, however, current consumption levels remain robust. Therefore, producers need to focus on sustaining current production while mitigating the impacts from a potential downturn. To do that, they should focus on these two: Managing drilling inventory and cutting costs by streamlining supply chains.

- Drilling Inventory: The supply curve for many oil projects, particularly US shale, is flat. For example, doubling the price of oil increased the amount of economically recoverable oil in the Eagle Ford eight-fold. At higher oil prices, that flatness is a boon, but it poses risks for producers operating acreage that could become uneconomic during a downturn. Producers need to continue focusing on high-grading their acreage portfolio even as current oil prices push them to increase production. In places like the Permian, we have already seen acquisitions focus on quality over quantity with stronger interest in “proven and highly probable production, not necessarily . . . bigger acreage positions,” as Justin Ramirez, senior financial analyst at Mercer Capital puts it. Time will tell if that trend will extend to other basins.

- Supply Chains: Oil and gas supply chains are complex, covering everything from exploration, drilling, and production to transportation, refining, and retail sales. Recent spikes in gasoline prices stemmed from refining bottlenecks and many upstream companies have reported higher operating costs due to supply-chain bottlenecks. We have seen some investments in rigs, pipelines, and refineries, but now would be a good time to double down on reinvesting the industry’s record profits into service providers and energy infrastructure.

Clear Skies for Now

Currently the industry is well positioned with disciplined capital spending, high commodity prices, and even higher profit margins. But high inflation, rising interest rates, and an uncertain economic outlook for many major economies could indicate a looming recession—if not in 2022, potentially in 2023 or 2024. While the current baseline scenario is that projections for sluggish, but positive growth hold true, the oil and gas industry should prepare for a potential recession by controlling the controllables. That means high-grading acreage and streamlining supply chains to boost company performance through both economic highs and lows.