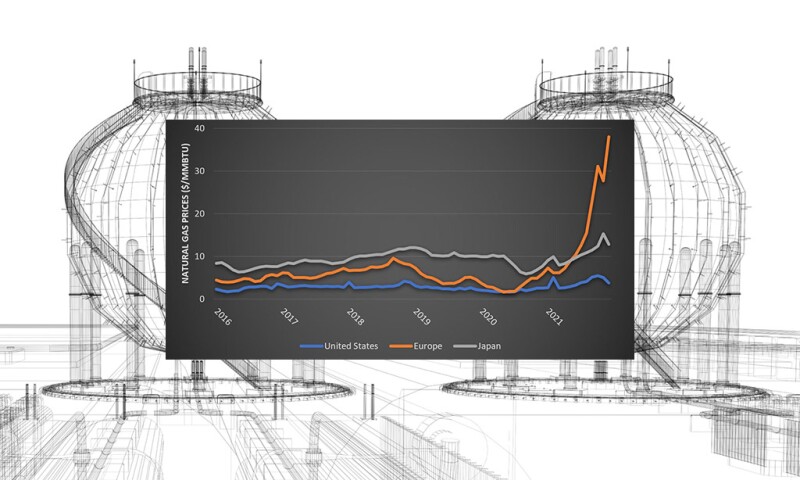

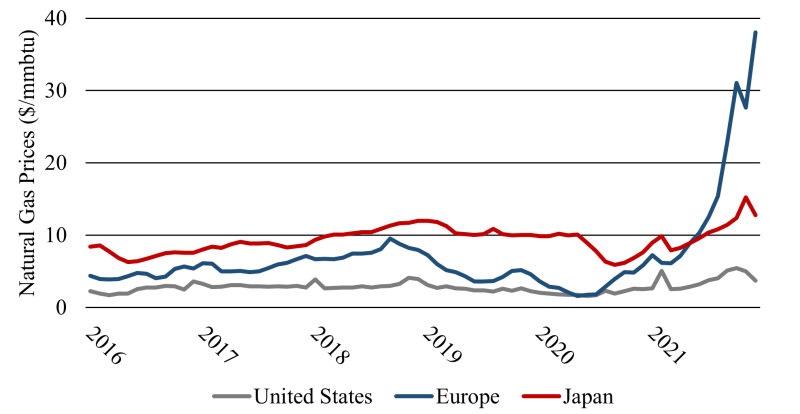

Natural Gas Prices Reached New Highs in 2021

Petroleum engineers often focus on the upstream side of the oil and gas industry. While supply-side factors such as development spend and production levels are important, so too are the demand-side factors driven by midstream and downstream considerations. This is particularly true of natural gas whose fragmented markets and transport barriers cause geographic price dislocations and energy system fragility. Last year saw record price differentials across the three major markets—Asia, Europe, and North America—because of rebounding consumption, low storage inventories, less-than-expected renewable power generation, and tightly constrained liquefied natural gas (LNG) export capacity (Fig. 1). Prices will likely remain stubbornly high in 2022 with both East Asian and Dutch futures trading over $25 per million British thermal units (mmbtu) through the end of the year.

| Note: The Dutch Title Transfer Facility is a proxy for broader European natural gas prices. East Asian futures are often quoted using the Japanese-Korean-Marker or JKM, which includes prices for spot LNG cargoes delivered ex-ship to China, Japan, South Korea, and Taiwan. Spot LNG prices are more volatile and have recently traded at a substantial premium to Japanese contract-based import prices reported by the World Bank and the Japanese Ministry of Economy, Trade, and Industry. |

Natural gas prices will remain elevated until either consumption wanes due to demand destruction and warmer weather, or deliveries increase to strained end-markets. The latter will prove unlikely. Pipeline deliveries to Europe probably will not increase in the near-term. Russian exports in 2020 and 2021 were near 5-year lows despite the fact that Gazprom’s gas production is at a 13-year high. While global LNG exports can mitigate regional price spikes and help Europe reduce its reliance on Russian gas, major exporters like the US have been at or above baseload capacity for most of 2021 (Fig. 2). US liquefaction capacity is expected to grow in 2022, but only by 2.4 billion cubic feet per day (bcfd). That is a drop in the bucket compared to Europe’s 52 bcfd of natural gas consumption.

New Infrastructure Is Needed to Provide Affordable Energy

The world is not running out of gas. At almost 400 bcfd, global production exceeded consumption in 2021 (IEA 2021). The problem is seasonality and geography. Asian and European demand exceed production by 35% and 260%, respectively (ibid.). In Europe, winter natural gas demand is double that of summer, driven mainly by space heating. Both of these challenges can be addressed through infrastructure investment. To reduce price volatility and sustainably and affordably supply natural gas to Europe and Asia as well as smaller producers in regions like Latin America, the industry must invest in increased LNG liquefaction capacity, domestic natural gas storage, and electricity transmission and storage.

1) LNG Liquefaction Capacity

First, LNG liquefaction and export capacity has strained to meet global demand. US LNG plant utilization averaged close to 100% of baseload capacity throughout 2021, with a brief dip in February reflecting Winter Storm Uri’s impact on Texas’ natural gas industry. Similarly, major producing countries like Qatar and Australia’s 2021 LNG exports were near or at record levels. However, those exports have not been enough to ameliorate high natural gas prices in major importing countries.

Increasing LNG liquefaction capacity could meet rising demand, but that takes time. Greenfield LNG project construction could take 4–6 years or more from start to finish even after permitting and financing have been finalized (US Department of Energy 2018). In the short-term, brownfield expansions and debottlenecking could provide incremental supply to blunt the edge of growing demand. LNG liquefaction build-out will likely be necessary but not sufficient to reduce global gas shortages.

2) Domestic Natural Gas Storage

Second, major natural gas importing countries need to invest in underground storage. LNG exports are only profitable if there are sustained price differentials between regions because of liquefaction and shipping costs (Ripple 2016). The rapid growth in LNG exports has not muted volatility as much as expected, with summer prices in the US and Europe converging in 2020. Because LNG exporters want to avoid shut-ins and run their facilities at close to 100%, they will likely be hesitant to build spare capacity.

Countries who bear the risks of undersupply should not rely on others to provide the reliability they need. They need to invest in domestic storage capacity to increase energy system resilience. North America has almost 6,000 billion cubic feet (bcf) of natural gas storage compared to less than 4,000 bcf in Europe and under 800 bcf in Asia Pacific. Moreover, Asia Pacific and Europe are net importers of gas and face price risks from not only seasonal demand but also supply interruptions. That means a cold winter or hurricane in Texas could lead to gas shortages in countries such as China, Japan, or the UK. These countries’ only means to address idiosyncratic market risk is through investing in underground gas storage.

3) Electricity Storage and Transmission

Third, increased reliance on renewable power and low wind speeds has led to electricity shortfalls in some countries. This lower renewable power generation exacerbated energy shortages when gas was diverted to power generation. Moreover, variable renewable generation cannot reliably provide baseload power without demand management and energy storage (Arbogast et al. 2018). Wind and solar generation peak at different times—and often not at the same time that demand peaks. Without expanding electricity storage and transmission, the only alternative to dispatchable fuels such as nuclear or natural gas is massively overbuilding renewable generation capacity (Shaner et al. 2018).

If natural gas importing countries intend to increase renewables penetration while decarbonizing heavy industries, then significant battery and other storage investment will likely be needed to prevent energy shortages (Andrey et al. 2020). That means that large oil and gas companies who intend to transition into large energy companies will need to invest heavily in storage in addition to their electricity generation and trading businesses. That also means that countries who are looking to expand low-carbon energy should support investment in the grid through financial incentives and simplified permitting and regulations for electricity storage as well as expanded cross-border power transmission.

Natural Gas Remains Fundamental to the Energy System

Many countries aspire to reducing consumption of higher-carbon energy in the long term. However, they will likely require fuels such as natural gas to generate heat and power for the foreseeable future. Recent record natural gas prices in Europe and Asia are a reminder how fragile the energy system can be—and how the energy transition might add to, not subtract from, that fragility in the near term. Higher energy prices create substantial societal costs and can contribute to geopolitical instability. The industry needs to continue investing in infrastructure to promote energy security and reduce risk of price shocks by spending on LNG liquefaction, domestic natural gas storage, and electricity storage and transmission. Those investments will not only provide short-term benefits in the form of lower energy prices and price volatility, but also have long-term benefits by enabling countries to reduce carbon emissions and energy system fragility more affordably.

References

Andrey C. et al., 2020. European Commission, Directorate-General for Energy, Study on Energy Storage: Contribution to the Security of the Electricity Supply in Europe.

Arbogast S. et al., March 2018. Kenan Institute, Measuring Renewable Energy as Baseload Power.

International Energy Agency (IEA), 2021. Gas Market Report Q4-2021.

Ripple, R. 2016. IAEE Energy Forum, U.S. Natural Gas (LNG) Exports: Opportunities and Challenges.

Shaner M. et al., February 2018. Energy & Environmental Science, Geophysical Constraints on the Reliability of Solar and Wind Power in the United States.

US Department of Energy and US Energy Association, March 2018. Global LNG Fundamentals.