As we approach the end of the year, it strikes me as a good time to take stock of how the oil and gas industry has evolved—and how that evolution will impact young petroleum professionals. While many things have changed over the past 20 years, three trends stand out the most to me. First, the industry has moved from worrying about supply to worrying about demand. Second, investment has pivoted from international and offshore to US onshore. And third, the push for abundant, low-cost energy to power the world has come into conflict with global climate change aspirations. For those who recently joined the oil and gas industry, these three trends will shape their careers, creating both obstacles and opportunities.

From Famine to Feast

Young professionals who like me did not graduate until after 2011 do not recall a period where the supply of oil and gas was in doubt. This has not always been the case, with many oil and gas executives warning of potential long-term hydrocarbon shortfalls and the need to make tough choices to promote industry and the economy in an energy-constrained world (National Petroleum Council 2007). Shale changed that dynamic drastically, with US natural gas production rising in 2007 and oil production in 2011, defying a multi-decadal decline in domestic output (Fig. 1). Today, US production is near all-time highs, and unlike the not-too-distant past, higher prices can readily translate to increased production without significant below-ground risks.

From Offshore to Onshore

While national oil companies (NOCs) represent roughly half of global oil and gas reserves and production, international oil companies (IOCs) such as the majors comprise two-thirds of global investment (International Energy Agency 2021). Historically, international companies’ investment focused on drilling deeper and deeper offshore in mature basins such as the Gulf of Mexico as well as up-and-coming basins like the one off the coast of Guyana and Suriname (Slaughter & Shattuck 2017a, 2017b). Following the 2015 and 2020 oil prices crash, investment declined by roughly 80% and 50%, respectively (Carpenter 2020). Because of onshore oil and gas’ often lower development costs and the rise of US shale, offshore investment fell more rapidly than that of onshore (Ibid.). This trend is not expected to change substantially and offshore spend is projected either to grow only modestly over the next 2 decades or even decline (Fig. 2). That does not mean there will not be continued international and offshore investment and production. But that investment will more likely be led by NOCs, not IOCs because of their access to large-scale, low-cost domestic resources (Alkadiri and Ewers 2020; Krauss 2021).

From Just Ending Energy Poverty to Also Cutting Carbon

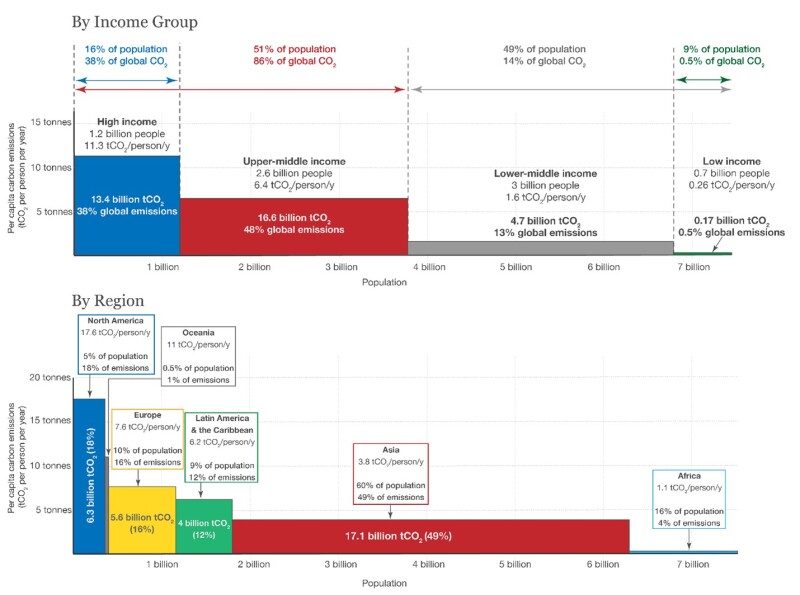

The oil and gas industry has been adept at providing abundant, accessible, and low-cost energy, allowing many to escape energy poverty. Despite the industry’s success, 840 million people still lack access to electricity, including 55% of those in Sub-Saharan Africa (Rockefeller Foundation 2021). At the same time, many countries seek to curb emissions in response to global warming, to be achieved in part by reducing reliance on oil and gas (Sommer 2021). That may not be necessary. Reducing energy poverty and carbon emissions can coincide, but there are inherent tradeoffs between various policy approaches that must be considered (Gordon 2021). The oil and gas industry has a role to play in navigating those tradeoffs by finding lower-carbon means of petroleum production, sequestering carbon through carbon capture, utilization, and storage projects, and providing expertise in oil-and-gas-adjacent industries such as geothermal power production. Ultimately the goal should be to produce more energy at lower carbon intensities and provide a more equitable carbon budget to the developing world (Fig. 3). That would reduce both energy poverty and carbon emissions simultaneously.

There Will Be Substantial Opportunities for Young Professionals

The next 20 years will almost certainly look different from the past 20. First, there appears to be abundant oil and gas resources that are readily accessible to meet growing global demand. While exploration will continue to play an important, albeit potentially smaller role, there will be a substantial need for oil and gas professions to continue drilling, completing, and producing petroleum for the foreseeable future. Second, US shale will play an outsized role in IOCs' energy portfolios but NOCs’ investments in international and offshore basins will provide career growth opportunities for young professionals around the world. Lastly, petroleum engineers will increasingly be looked at to not just develop oil and gas resources, but also sequester carbon, generate geothermal and other alternative sources of power, and find new ways to provide more energy with lower carbon emissions. While this may be a tall order, previous generations have tackled the challenges of their times and this generation will be no different.

References

Raad Alkadiri & Björn Ewers. 2020. Preparing National Oil Companies for a New Energy Landscape, Boston Consulting Group.

Scott Carpenter. 2020. ‘On Pause’ - Offshore Oil Industry Faces Biggest Setback in Years, Forbes.

Meghan Gordon, 2021. Global Leaders Must Weigh Energy Poverty Wile Setting Climate Policies: Barkindo, S&P Global Platts.

International Energy Agency. 2018. Offshore Energy Outlook 2018.

International Energy Agency. 2020. Share of Oil Reserves, Oil Production and Oil Upstream Investment by Company Type, 2018.

Clifford Krauss. 2021. As Western Oil Giants Cut Production, State-Owned Companies Step Up, New York Times.

National Petroleum Council, 2007. Facing the Hard Truths About Energy, pp: 5–11.

Our World in Data. 2021. Emissions by World Region.

Rockefeller Foundation. 2021. Power Equals Opportunity.

Andrew Slaughter and Thomas Shattuck, Seven Decades in the Making, Oilfield Technology, Apr, pp. 10, 12–14.

Andrew Slaughter and Thomas Shattuck, 2017. Hunting Offshore Opportunities, Oilfield Technology, Dec, pp.10, 12–13.

Lauren Sommer, 2021. Here's What World Leaders Agreed to— And What They Didn't— At the UN Climate Summit, National Public Radio.

US Energy Information Administration. 15 Nov, 2021. Drilling Productivity Report.

US Energy Information Administration. 30 Nov, 2021.Crude Oil Production.

US Energy Information Administration. 30 Nov, 2021. Natural Gas Withdrawals and Production.