The 2025 S&P Global Market Intelligence Report presents an analysis of the burgeoning financial risks stemming from physical climate hazards and a lack of corporate preparedness. Against this backdrop, the transition imperative to curb greenhouse gas (GHG) emissions receives far more attention than preparation for the physical impacts of a warming world. The report identifies and quantifies how large the costs due to the climate risks could become and then assesses whether corporate adaptation planning has kept pace with the rise in physical climate risks.

Estimated Financial Costs of Physical Climate Risks

The total cumulative cost of climate hazard exposure for companies in the S&P Global 1200 is projected to reach $25 trillion by 2050, equivalent to 74% of the index companies’ total 2024 revenue and 31% of its aggregate market capitalization. Of this total, $16.5 trillion stems from property damages and excess capital expenditures such as rebuilding, reinforcing, or relocating. Another $4.5 trillion is attributed to foregone revenue from business interruptions like power outages, transport disruptions, and heat-induced productivity losses, while $3.8 trillion relates to elevated operating costs, including cooling, water procurement, and maintenance after extreme weather events.

Primary Climate Hazard Risk Drivers

The primary climate hazard risk drivers identified in the report are extreme heat, water stress, drought, and pluvial flooding, collectively accounting for the bulk of projected climate-related costs. In the 2050s, extreme heat, responsible for 58% of total costs, undermines labor productivity and drives up energy demands for cooling in operations. Water stress, contributing 21%, raises input costs for water-intensive industries and heightens regulatory exposure in regions with tightening water controls. Drought, accounting for 11%, disrupts agricultural and hydroelectric outputs, amplifies wildfire threats, and necessitates costly investments in water-saving technologies. Lastly, pluvial flooding, comprising 4% of costs, results in infrastructure damage from surface runoff, business interruptions, and growing insurance premiums or reduced coverage in flood-prone areas.

Sectoral Distribution of Climate Costs

Utilities bear the highest burden, as extreme heat strains power plants and transmission lines, and water stress undermines hydropower output. Energy firms confront heat‑induced equipment failures, water shortages for enhanced recovery, and flood risks at refineries and terminals, while offshore platforms and coastal facilities must adapt to rising seas and storm surges. Financial institutions face indirect impacts through credit, underwriting, and investment exposures to vulnerable industries. Other sectors like communication, real estate, industrials, and consumer staples also confront significant but varied costs driven by their specific asset footprints and hazard profiles (Fig. 1).

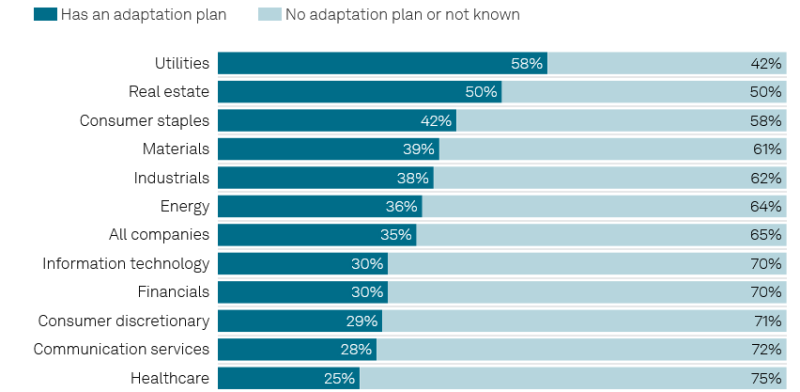

Corporate Adaptation Planning Landscape

S&P Global Corporate Sustainability Assessment (CSA) defines a context-specific adaptation plan as one that identifies climate risks, integrates physical and nonphysical measures, and sets timelines and accountability for implementation of adaptation actions. Only 35%, about one-third, of the 7,934 companies assessed in the 2024 CSA disclosed having such a plan. This low penetration highlights a critical adaptation gap as physical risks intensify.

The report disaggregates adaptation plan adoption by sector (Fig. 2). Sectoral adaptation rates vary widely, reflecting differences in physical exposure and operational priorities. The Utilities sector leads with 58% of companies disclosing climate adaptation plans, driven by the high vulnerability of grid infrastructure and generation assets to storms, extreme heat, and water scarcity. Real estate follows at 50%, where direct property ownership necessitates proactive measures such as flood defenses, cooling system upgrades, and resilient building designs. The lagging sectors include IT, financials, consumer discretionary (29%), communication services (28%), and healthcare (25%), that are increasingly exposed to climate hazards but remain underprepared.

The report paints a clear picture: As climate hazards intensify, the financial stakes for global corporates mount into the tens of trillions of dollars. Yet the pace of adaptation planning remains inadequate. To avert escalating losses and safeguard long-term shareholder value, companies must elevate adaptation alongside decarbonization. This entails robust hazard mapping, board-level oversight, cross-sector collaboration, and alignment with evolving regulatory frameworks. Investors, lenders, and policymakers play critical roles in catalyzing and scaling these efforts through transparency mandates, financial incentives, and standardized risk metrics.