Sometimes when the dots are connected, the lines are imaginary.

This may hold true for those trying to draw comparisons between the supergiant Ghawar oilfield in Saudi Arabia with a swath of land in Texas and New Mexico known as the Permian Basin.

“They’re both fruit, but it’s definitely apples and oranges,” said Scott Tinker, the director of the Bureau of Economic Geology at the University of Texas at Austin, who added that trying to size up the two as analogous oil producing systems “is stretching it pretty far.”

But the comparison has become a popular topic this month after Saudi Aramco released a detailed financial prospectus ahead of its first-ever bond auction that revealed some previously non-public production figures.

One of the most cited was that Ghawar’s maximum output is 3.8 million B/D. The number has drawn attention because it is the first official update on the crown jewel’s state of decline in more than a decade when output was pegged at around 5 million B/D.

By the end of last year, the Permian surpassed 3.8 million B/D for the first time. Oil companies there are now just shy of reaching 4.1 million B/D, according to the US Energy Information Agency. All of this has led some to declare that the Permian has overtaken Ghawar as “the world’s top oil producer.”

Earning the number one spot certainly marks a historic milestone for the Permian’s unrivaled comeback story. But seen from the petrotechnical point of view, this is an arbitrary positon.

“For a really good comparison to what the Permian is doing, you need to look at the whole of Saudi Arabia, not just its biggest field,” said Andrew Pepper, the director of a consulting firm called This Is Petroleum Systems and a former vice president of geoscience with Australian producer BHP Billiton.

He pointed out that while some predict Permian production will rise to 6 million B/D in the next few years, “you’re still only half way there” to the 12 million B/D that the entire Saudi oil basin is said to be capable of ramping up to. Current output in Saudi stands at around 10.3 million B/D.

Pepper noted that if the discussion is widened to include the rest of the Middle East’s oil province, which includes Iran, Iraq, and Kuwait, the Texas giant becomes “even less comparable” in terms of production.

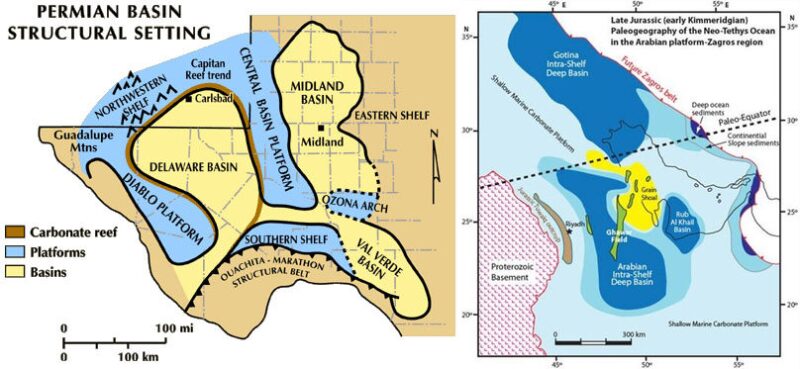

These paleographic maps of the Permian Basin (left) and the Arabian basin, which includes Ghawar (right, in green), reveals the scale of both oil producing regions and their distinctive geologies. As a field, Ghawar is quite simple. As a basin, the Permian is considered complex. Sources: Bureau of Economic Geology at the University of Texas at Austin, AAPG.

A Dream Field

Discovered in 1948, Ghawar has since contributed half of every barrel produced in Saudi. And though they have tried, explorers have never found another field that so precisely hits the trifecta of being onshore (i.e., low development costs), massive in size (174 by 19 mi), and containing such high-porosity reservoir rocks (up to 35%). “It’s a dream,” summed up Pepper.

Decades after the field peaked in 1981 at 5.7 million B/D, these harmonious conditions and its sterling reputation helped some to hold onto the assumption that Ghawar may still be holding steady at around 5 million B/D of crude. Bloomberg News reported that figure has stuck around in part because of a presentation Aramco executives issued 15 years ago in response to concerns over the peak oil debate of the early 2000s.

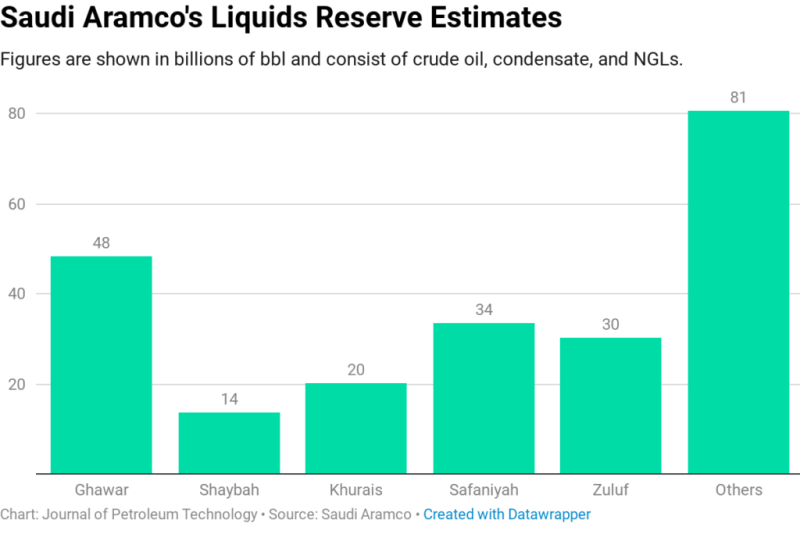

But thanks to the new document, the likes of which has never been released by Aramco before, we know that Ghawar is being asked to do less while its sister fields pick up the slack. Still, the national oil company reports the field has 48 billion bbl in reserves, which at current rates means the pumps should not run dry until some time in the 2050s.

Without considering this kind of historical or technical context, there are concerns that the current production capacity of Ghawar could be overemphasized. Among those who share them is Sami Alnuaim, a 31-year veteran of Aramco where he currently serves as a manager of petroleum engineering application services.

Alnuaim is also the 2019 SPE President, and it was in this capacity that he shared his thoughts on Twitter, writing: “Ghawar is still healthy as it was a decade ago. The lower production is by design to maximize ultimate recovery by increasing sweep efficiency, reducing cost, and minimizing operational carbon intensity. With all respect to all, it takes petroleum engineering knowledge to see this.”

Alnuaim referenced the fact that sections of Ghawar have been undergoing waterflooding for decades. He also quipped that the potential for enhanced oil recovery, or EOR, is so big that Ghawar could be considered “yet to be discovered.”

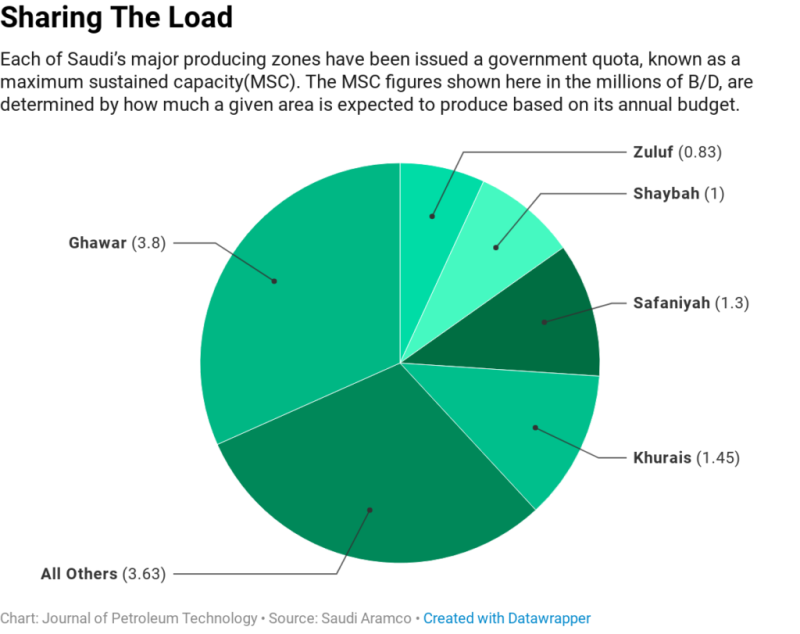

The prospect of improving yield raises an additional nuance that remains unsettled: whether 3.8 million B/D is really the current production of Ghawar, or even its ceiling. The key involves how one interprets what Aramco calls maximum sustained capacity (MSC)—a production target set by the Saudi government.

Ellen Wald, an energy consultant and author of Saudi Inc. which details the financial history of Aramco, said the definition of MSC as presented in the prospectus is “very confusing” as she too issued her reactions on Twitter. “MSC does not imply anything about what a field is producing or could produce at full throttle,” she wrote. “It’s simply a measure of the responsibility to get a total production rate of 12 [million B/D].”

A Rocky Comparison

While much of the focus is on their production figures, it is within the rocks that drawing a likeness between Ghawar and the Permian truly verges on a fool’s errand.

Tinker, who doubles as the state geologist of Texas, recalled visiting Saudi Aramco for a conference in the 1990s where he observed how the carbonate reservoir “behaves and responds” to injections for distances that can span dozens of miles. While acknowledging that the supergiant is composed of subsections, Tinker said such characteristics allow Ghawar to be described as “a unified field.”

By contrast, he said the Permian represents a “a whole basin with multiple source rock horizons in it and multiple conventional reservoirs—and it’s actually two basins separated by a central platform.”

This is a succinct picture of the so-called stacked shale and sandstone formations found within the Midland and Delaware Basins that make up the eastern and western portions of the Permian. The two plays account for the bulk of the region’s tight-oil and gas activity, yet have distinct geologic, tectonic, and production profiles. Also unique are the central basin platform and the shelf areas that make up the outer edges of what we call the Permian.

They all combine to form one of the most complex oil and gas structures in the world—which is one reason it took the technological breakthroughs in horizontal drilling and hydraulic fracturing to be revitalized.

Zooming back to the other end of the spectrum, Ghawar constitutes a single formation (the Arab-D limestone) which is prized for its “giant, simple anticlines” that have been well understood thanks to 3D seismic since the 1970s, said Pepper.

Regardless of which lens is chosen to view the comparison, it only becomes harder to see how the Permian bests Ghawar or Saudi’s combined portfolio on a pound-for-pound basis.

Since it was discovered in 1920, more than 400,000 wells have been drilled across the 86,000 sq mi that make up the Permian. While official numbers are difficult to come by, is not widely held that anywhere close to that number have been drilled across Ghawar’s 3,300 sq mi since the 1940s, let alone the entirety of Saudi’s desert landscape.

A proxy to this argument was highlighted several years ago in an investor report by Schlumberger, which showed that during the shale boom of 2014, US operators drilled more than 35,000 wells to achieve a combined petroleum liquids production of 11.7 million B/D. That same year, Saudi needed to drill a fraction of that—only 399 new wells—to maintain an output of 11.4 million B/D.

Despite advances in well productivity, tight-oil wells come on strong before starting their rapid declines. To offset these deficits, shale producers have found themselves on a drilling treadmill that is raising questions about how much longer the Permian’s production can continue its upward march.

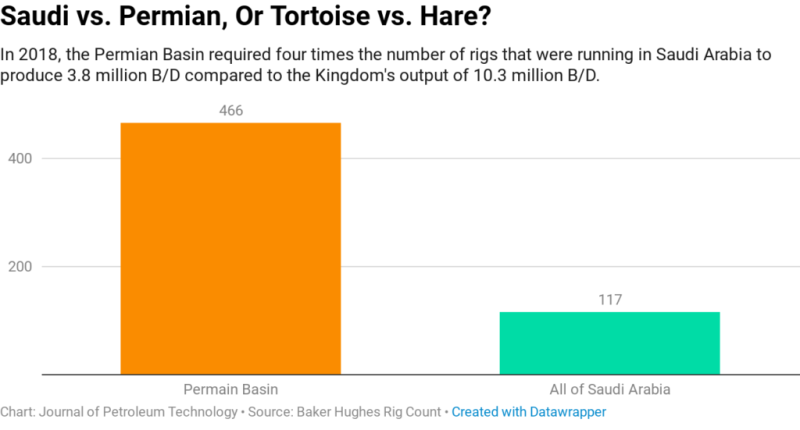

Over the past year, this effect has driven Permian producers to maintain more than 450 active rigs to surpass 4 million B/D, according to the Baker Hughes’ rig count. In the same span, Saudi produced more than 10 million B/D while using no more than 125 active rigs during any period of 2018.