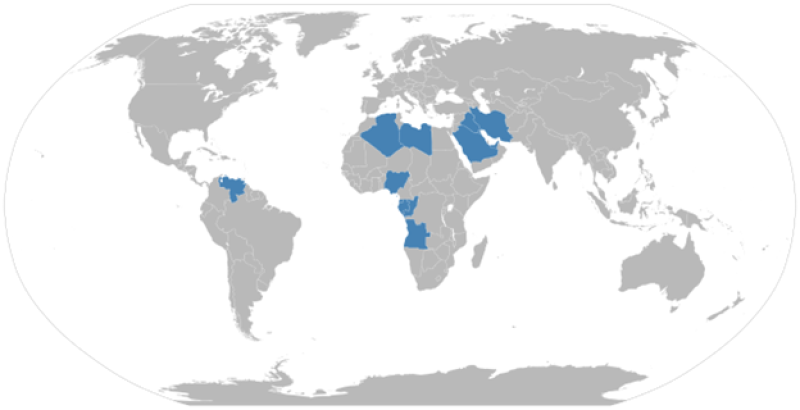

The Organization of Petroleum Exporting Countries (OPEC) arose in response to the role of multinational oil companies as the price makers in the international crude market. In an effort to develop a stronger negotiating position, five countries—Iran, Iraq, Kuwait, Saudi Arabia, and Venezuela—founded OPEC in September 1960, with the mission “to coordinate and unify the petroleum policies of its Member Countries and ensure the stabilization of oil markets in order to secure an efficient, economic, and regular supply of petroleum to consumers, a steady income to producers, and a fair return on capital for those investing in the petroleum industry” (OPEC). Since its inception, the founding members have been joined by a rotating cast of other member countries. Currently, Algeria, Angola, Congo, Equatorial Guinea, Gabon, Libya, Nigeria, and the United Arab Emirates comprise the remaining eight of 13 members (Fig. 1.)

Fig. 1—Current members of OPEC. Source: OPEC

At the time of its inception, OPEC’s five founding members controlled 80% of the world’s crude exports (Yergin 2008). Today, its 13 members control an estimated 40% of global production and 60% of internationally traded crude (Investopedia) as well as 80% of global crude reserves (Fig. 2). Despite controlling such a large portion of the global crude volumes, OPEC’s record of influencing the international crude market has been mixed—coordinated action by members can be difficult with such a multitude of competing political and economic concerns. However, it has had success at a global level. Its successes have also helped create market conditions that would later make it a victim of its own achievement.

Fig. 2—Distribution of OPEC crude reserves. Source: OPEC

1967–The Six-Day War

In its early years, OPEC’s members were subject to, rather than masters of, market forces. Import and production quotas in the US, foreign ownership of concessions, a supply glut compounded by the discovery of new reserves and competing political and economic concerns amongst members made it difficult to corral markets. When the Six-Day War began in June 1967, between Israel and a coalition of Arab countries (Egypt, Syria, and Jordan), Saudi Arabia, Kuwait, Iraq, Libya, and Algeria attempted to throttle Western support for Israel by cutting off oil shipments to the US, the UK, and West Germany (Brookings Institution). However, because the US quota system prevented its domestic producers from maximizing production, producers in the US were able to tap this latent production and reorganize oil shipments to alleviate distressed markets. OPEC members Iran and Venezuela also increased production, negating the impact of export bans from other OPEC members (Yergin). With global crude volumes replenished and embargoing nations losing export revenue, the embargo attempted in 1967 largely failed.

1973 Oil Embargo

The same conditions that prevented the Arab members of OPEC from influencing the market also set the stage for the market to be profoundly influenced by OPEC only 6 years later. Cheap oil resulted in skyrocketing demand and a lack of incentive to explore for additional reserves. Nixon also abolished US oil quotas, adding demand to the international market and allowing domestic producers to run at maximum capacity, thereby eliminating the untapped production utilized in 1967 (US Department of State). Between 1970 and 1973 market prices for crude doubled, and in 1973, Saudi Arabia stepped into the role previously occupied by the US as global swing producer (Yergin). Finally, OPEC members had taken steps to nationalize oil production, giving them far greater control over volumes (Brookings Institution). When the Yom Kippur War began in October 1973, Arab members of OPEC found themselves in a much more influential market position.

Within 2 weeks of the start of the war, Arab oil ministers agreed to an oil embargo targeting the US and other countries supporting Israel (US Department of State). In addition, participants would cut production by 5% a month while maintaining a pre-war supply volume to friendly countries. Lacking the spare capacity of 1967, and with domestic consumption alone up 33% (US Energy Information Administration), market prices responded. The price of a barrel rose from $2.90 to $11.65 by January 1974 (Federal Reserve History) . The embargo would last until March 1974 (far outliving the 3-week war), after which point it was discontinued, despite a lack of consensus amongst participants (Federal Reserve History).

The 1973 oil embargo can be considered a qualified success. It did not achieve its political aims, but it affirmed OPEC’s hegemony over oil markets. It also highlighted a global dependence on abundant oil and spurred a search for new energy sources, new oil sources, and improved energy efficiency (US Department of State).

1979 Oil Crisis and the 1986 Market Crash

Efforts to find new reserves were further galvanized in 1979–1980 when the Iranian Revolution and Iran-Iraq war reduced global oil production by approximately 4.8 million B/D, or 7% of global production (Brookings Institution). Initially, Saudi Arabia and other OPEC members stepped in to fill some of this shortfall (Time Magazine). However, non-OPEC producers also brought on an additional 5.6 million B/D between 1979 and 1985. The surge in supply dropped prices, and Saudi Arabia attempted to moderate production in its role as global swing producer (Brookings Institution). However, other OPEC producers did not adhere to their production quotas and continued to oversaturate the market. By 1985, Saudi Arabia vacated its position as swing producer in a bid to recapture its market share, which had declined by as much as 80%, and push out high-cost producers. Flooding the market with oil precipitated the crash of 1986, which eventually brought noncompliant OPEC members back to the negotiating table. What followed was an agreement on quotas and pricing that eventually helped reestablish market stability (OPEC). While an agreement was finally reached, OPEC failed in its stated mission to stabilize markets in a timely manner due to the competing economic interest of its members.

The Surplus Years

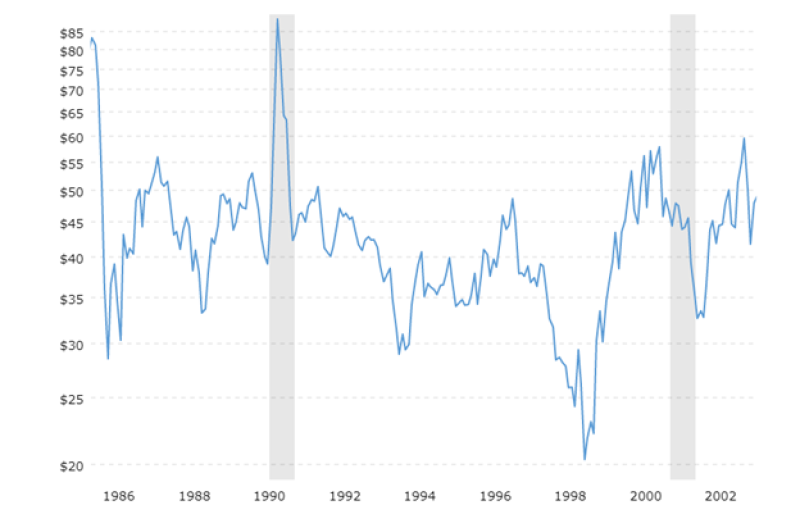

Leading into the 1990s, it could be argued that sustained low crude prices contributed to Iraq’s invasion of Kuwait in an attempt to reduce Kuwaiti oil output. However, the supply disruption from the First Gulf War was short lived. This exception aside, in the 15 years following the crash in 1986, prices remained relatively stable and subdued, especially during the years of the Asian Financial Crisis (Fig. 3). Attempts to regulate members’ production compelled some members who felt restricted by quotas to leave the organization in pursuit of economic goals (The New York Times). Despite quotas, prices remained subdued.

Fig. 3—Oil prices between 1986 and 2002. Source: Macrotrends

The Rise of Fracturing

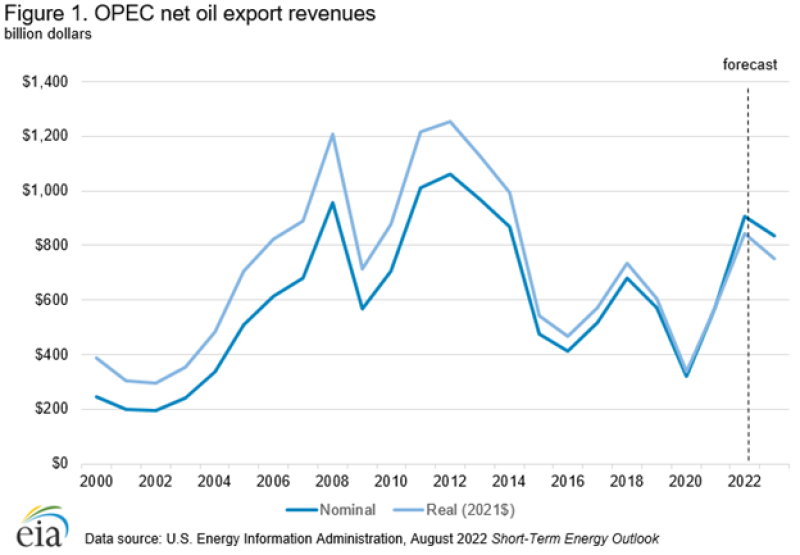

Between 2003 and 2014, crude prices experienced volatility, but were generally high, peaking at $147.30/bbl in the summer of 2005 and providing OPEC with some of its highest-ever export revenues (Fig. 4). This period of sustained high crude pricing was due to factors impacting both supply and demand. On the supply side, instability in Iraq, Nigeria, and Libya impacted production or the perceived reliability of production. On the demand side, increasing industrialization, development, and personal wealth, especially in developing countries with large populations such as China and India, helped push up global demand (The New York Times). Personal transportation in the US also increased consumption notably.

The one exception to high prices in this period was the onset of the 2008 Financial Crisis, which saw oil prices fall significantly. During this time, cracks again appeared in OPEC’s unified front. Although the organization announced it had voted to reduce production (The New York Times) to shore up prices, Saudi Arabia unilaterally committed to supplying oil to all customers in an effort to drive prices below $100/bbl and moderate the size of the impending recession.

Sustained high prices also created an environment that gave rise to a new competition for OPEC—the American shale producers. Known shale reservoirs that were previously left undeveloped due to the economics of drilling and completing them were suddenly technically and economically viable with the combination of horizontal drilling, hydraulic fracturing, and sustained high prices.

Fig. 4—OPEC revenues in the early 2000s were some of its highest ever. Source: US Energy Information Administration

2014—The Crash

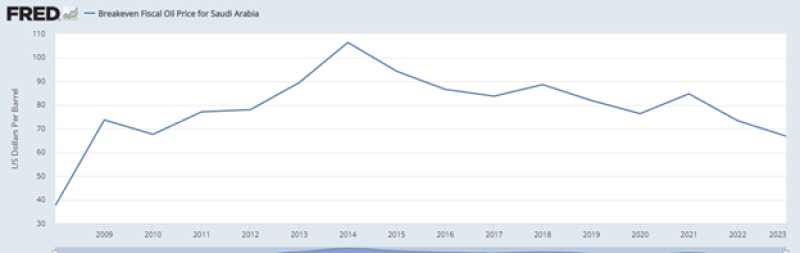

With a new major source of production, the crude market soon entered a state of oversupply. To fulfill its self-appointed role as market stabilizer, OPEC needed to cut production. Many OPEC members, concerned about the impact of lower oil prices on their finances and economies, favored making cuts (The Iran Project 2014) to buoy oil prices. However, as the new production was outside OPEC’s control, Saudi Arabia committed to protecting its market share rather than the market price and refused to consider production cuts and in some instances OPEC members actually increased production (The New York Times). With OPEC’s breakeven production cost (National Bureau of Economic Research) significantly lower than that of its American shale rivals (Insider), there was ample room to try and push shale producers out of the market and prices plummeted, bottoming at $27/bbl in early 2016. While shale producers did indeed feel the pinch, the pain was not unilateral. OPEC members finances were based on a price per barrel significantly higher than $27. Saudi Arabia’s, for example, has been well above $60 for the last decade (Fig. 5).

Fig. 5—Saudi Arabia’s fiscal breakeven price. Source

2017—OPEC+

With widespread economic pain and US shale producers tenaciously holding on by driving down completions costs, in 2017 OPEC (including Saudi Arabia) agreed to its first production cuts (Bloomberg) since the financial crises of 2008 (the ones Saudi Arabia declined to observe). This agreement was unique in that it also included other oil-producing countries that were not members of OPEC, most notably Russia. This grouping, known as OPEC+, has been worked, over the past 5+ years, to manage production within the group in order to balance the global market, predominately through distributed production cuts. These efforts, possibly incentivized by domestic financial strain, have helped stabilize the oil market since their introduction. While events such as the COVID-19 pandemic and Western sanctions on Russia as a result of the war in Ukraine have served as unprecedented market disruptors, the impact on price has been surprisingly transient.

Given how recent this last period is, a final retrospective assessment is still some years out. However, in the 60-year history of OPEC, it’s track record as a market stabilizer is mixed. When it wasn’t flexing its production share in the pursuit of political goals, internal disagreement often scuttled attempts at market making. It took the rise of an external threat and challenger in the form of American shale producers, contribution from non-OPEC producers, and a prioritization of economics over politics to form and maintain a unified, effective front and truly act in a capacity as market stabilizer.