Hydrogen is the most abundant element in the universe. It is a fuel source so powerful that it took us to the moon. Presently, 73 million mt/year of pure hydrogen is used mostly by the industry during oil-refining (~60%) and synthetic nitrogen fertilizer production (~40%), and a low quantity is used for energy because it is expensive when compared to fossil fuels. However, hydrogen is often viewed as an important energy carrier in a future decarbonized world. The use of hydrogen can be broadly divided into four categories: power-to-power, power-to-gas, power-to-mobility, and power-to-industry.

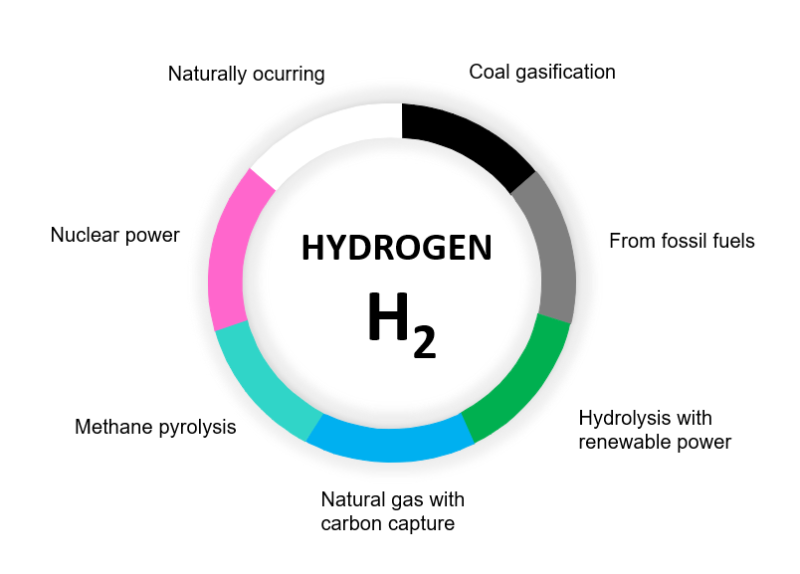

Hydrogen is odorless and invisible to our eyes but is often described through a range of colors. The color codes are based on how the hydrogen is sourced. The article provides an overview of the production, cost, and key players of different colors of hydrogen.

Black / Brown

What: Hydrogen originating in a process of coal gasification is called black (from black coal) or brown (from brown coal) hydrogen. Coal gasification involves conversion of coal from its solid state into gaseous form. The process disintegrates coal into its chemical constituents, which includes methane gas. The coal then reacts with oxygen and steam under high temperature and pressure, which results in the formation of syngas, a blend of hydrogen, carbon dioxide, and carbon monoxide. The syngas then further undergoes hydrolysis to increase the hydrogen yield.

3C + O2 + H2O ⇌ 3 CO + H2

CO + H2O ⇌ CO2 + H2 ∆H −41 kJ/mol [Water-gas shift reaction (exothermic)]

Current Cost: The cost associated with brown hydrogen production is less when compared to hydrogen production from electrolysis and natural gas. The cost of brown hydrogen, which pumps around 830 million tonnes of CO2 annually, currently ranges currently from $1.20 to $2.20/kg, largely depending on the price of coal (IEA).

Players: A pilot project that involves transport of liquid brown hydrogen from Australia to Japan has been commenced by a Japanese-Australian consortium. The Hydrogen Energy Supply Chain pilot project, valued at $388 million (A$500 million) comprises a team of experts from Sumitomo, Iwatani, J-POWER, Marubeni, Kawasaki Heavy Industries, and AGL (Hydrocarbons Technology).

Future: A forecast predicts the valuation of the brown hydrogen market in 2030 to reach $48.9 billion from $30.4 billion in 2020, witnessing a compound annual growth rate of 4.7%. The minimal economic cost linked with coal gasification is boosting the demand for brown hydrogen production (PR Newswire).

Gray

What: Gray hydrogen refers to hydrogen produced from fossil fuels, using the most commonly applied concept of gas reforming. In this process, natural gas and steam at high temperature and pressure are converted to hydrogen and carbon dioxide through a catalytic chemical reaction, which is endothermic and uses steam at 700 °C to 1000 °C. Since a large amount of carbon dioxide is emitted during the production process, it is referred to as “gray," the name giving off a less sustainable impression. In fact, the production of gray hydrogen is responsible for 6% of all natural gas consumption globally (Power Technology).

2CH4 + 2H2O ⇌ 2CO + 3H2 ∆H +206 kJ/mol

CO + H2O ⇌ CO2 + H2 ∆H −41 kJ/mol [Water-gas shift reaction (exothermic)]

Current Cost: A range of technical and economic factors influence the production cost of hydrogen from natural gas, with gas prices and capital expenditures being the two most important ones. Fuel costs account for between 45% and 75% of production costs. Gray hydrogen is presently the cheapest source of producing industrial hydrogen (around $1.00/kg). The process on its own is not environmentally friendly since 9–12 tonnes of CO2 is produced for every tonne of hydrogen (Pillsbury Law).

Players: The first methane steam reforming process was built in the UK during the 1930s by companies like Imperial Chemical Industries, today known as AstraZeneca, and Standard Oil Co., which today comprises ExxonMobil, Chevron, Marathon Petroleum, and BP (Murkin and Brightling 2016), and since then, these have produced gray for multiple purposes. It is not until recently, a consortium of 28 companies including Shell, TotalEnergies, Equinor, and others took the H2Zero pledge at COP26 to replace gray hydrogen with hydrogen processes that release less carbon during its production (Recharge).

Future: The low-carbon transition threatens both gray and brown hydrogen. Carbon capture and storage (CCS) technologies exist to some extent but they are still unrealistic to be applied on a larger scale. However, government and policy makers envisage to swap the use of gray hydrogen with green and clean colors of hydrogen.

Green

What: Green hydrogen is the hydrogen produced without greenhouse gas emissions. It is made through the electrolysis of water using renewable energy sources such as solar or wind power. Electrolysis entails an electrochemical reaction to split water into oxygen and hydrogen, releasing no carbon-dioxide in the process. There are some other specific colors of hydrogen associated with electrolysis using specific renewable energy source, such as yellow hydrogen, which is produced using solar energy (National Grid).

Current cost: Green hydrogen makes a small proportion of the existing hydrogen mix since its production is expensive. In a 2020 study titled Path to Hydrogen Competitiveness, the Hydrogen Council (a global CEO-led initiative of leading companies with the goal of promoting hydrogen to enable the clean energy transition) expressed the current price for green hydrogen to be around $6/kg. This means that currently green hydrogen is more expensive than both gray and blue hydrogen. However, it is identified that $2/kg is the tipping price point for green hydrogen to become an attractive choice for use in multiple sectors. (Pillsbury Law)

Players: Several players have had a history of utilizing electrolyzers to split water into oxygen and hydrogen. While previously a niche, this sector is about to ramp up in an unprecedented manner. The key players to note include Bloom Energy Corp., Plug Power, Next Hydrogen Solutions, Fusion Fuel Green, ITM Power, and NEL, among many others. In addition, green hydrogen has already seen some investments from major oil and gas companies. Shell has plans to increase green hydrogen production capacity at its Rhineland refinery 10-fold by 2030. Moreover, BP has invested $1.9 million to explore the creation of a green hydrogen export facility in Western Australia. (Wall Street Journal)

Future: According to a PWC report, green hydrogen demand will grow at a moderate, steady pace through niche applications until 2030. Beyond 2030, the demand will accelerate and the hydrogen demand by 2050 could vary by 150–500 million tonnes per year, depending on global ambitions and trends, and the development of sector-specific activities.

Blue

What: It is produced mainly from natural gas, using the steam methane reforming or autothermal reforming process that mixes natural gas with very hot steam and catalysts and produces H2 and CO2. This CO2 can be then captured and stored underground by CCUS to make the process carbon-neutral, and the resulting H2 is called blue hydrogen.

Current Cost: This is the most common way to produce hydrogen. As per IEA, the cost of producing hydrogen from fossil fuels in 2019 was capped at $2.6/kg; This is three times lower than the highest prices for hydrogen produced from renewable electricity. The difference is expected to narrow in 2050, but blue hydrogen is still expected to be cheaper. Future costs of blue hydrogen will critically depend on the technology, scale, and proximity to CO₂ storage options, as well as the price of the natural gas feedstock. However, it requires a lot of energy to make blue hydrogen. For every unit of heat in the natural gas at the start of the reforming process, only 70–75% of that potential heat remains in the hydrogen product (Kalamaras and Efstathiou 2013). Also, to achieve a carbon-neutral outcome, the required CCUS adds ~$0.5/kg to the cost of conventional hydrogen processes, resulting in a range of $1.5–$2.5/kg, final price depending on the cost of natural gas input (Nolan et al. 2021).

Players: Among some big projects, industrial gas supplier Air Products released a plan to invest $4.5 billion in blue hydrogen production at Ascension Parish site in Louisiana (AP News).

Future: Considering the energy conversion aspects of the process, a higher volume of methane is required to produce blue hydrogen, which must pass through reformers, pipelines, and other infrastructures. This increases the methane leakage potential, which raises concerns regarding the “cleanliness” of the blue hydrogen fuel. Having said that, when used with CCUS, blue hydrogen produces nearly zero emissions.

Turquoise

What: Turquoise hydrogen production uses a modified pathway when compared with blue hydrogen production. A pyrolyzer splits the natural gas feedstock to produce hydrogen and solid carbon without any need for carbon emission abatement. The turquoise color fits in between the green and the blue colors because even though natural gas is used as the raw material, the low carbon intensity of the process makes it an attractive option.

Current Cost: If the electricity needed to generate heat for the natural gas breakdown comes from renewable sources, the process becomes carbon neutral. If the natural gas comes from biogenic sources, the process can be carbon negative. The aim is to bring the cost of turquoise hydrogen down to the same price as traditionally synthesized (gray) hydrogen today, making it more attractive to buyers.

Players: Mitsubishi Heavy Industries Group has recently invested in Monolith Materials (first US manufacturer of turquoise hydrogen) and has since also backed another startup company, C-Zero, to strengthen its hydrogen-energy value chain strategy. C-Zero is focused primarily on producing hydrogen and sequestering solid carbon. In Nebraska, Monolith Materials already runs a commercial-scale, emissions-free production facility which will produce clean hydrogen alongside around 14,000 metric tons of carbon black per year.

Future: Methane pyrolysis has been around at least since the mid-twentieth century and the technical approaches have evolved from thermal cracking through fluidized bed and thermo catalysts process to more recently using plasma and liquid metal bubble columns. The researchers at Palo Alto Research Center have tracked the industrial efforts to commercialize methane pyrolysis technologies. Most of the technologies in the works have been able to achieve the Technology Readiness Level of 3–4 out of 10 with some exceptions of commercial and pilot plants currently producing hydrogen around the world. Turquoise hydrogen is appealing to many hydrogen proponents because it bridges the gap that exists within the industry for green hydrogen production, especially considering the fact that turquoise hydrogen can tap into the existing hydrocarbon value chains without CO2 emissions in the production process.

Pink

What: Like green hydrogen, it is generated through electrolysis of water but using nuclear energy as a power source. It is also referred to as purple hydrogen or red hydrogen.

Current Cost: According to the US Department of Energy (DOE), the current goal of the hybrid nuclear systems (residual heat and electricity) breathing new life into nuclear-powered hydrogen production is to bring the cost of the clean hydrogen to $1/kg within the next decade. The current cost associated with nuclear hydrogen production ranges from $2 to $6 depending on the production system in place. For example, Japan Atomic Energy Agency successfully demonstrated the feasibility at pilot-plant scale and plans to commercially utilize high-temperature reactors to produce hydrogen at less than $3/kg. (World Nuclear Association)

Players: In October, PNW Hydrogen received $20 million funding from the US DOE to produce pink hydrogen at Palo Verde Nuclear Station in Phoenix, Arizona (US DOE). French electricity company EDF also showed interest in producing pink hydrogen at Sizewell C nuclear facility in the UK. Recently, world’s first pink hydrogen commercial deal has been signed in Sweden between Swedish power corporation, OKG, and London-based industrial gas company, Linde, where pink hydrogen will be produced at the OKG-operated Oskarshamn nuclear power plant (Recharge News).

Future: The very high temperatures from nuclear reactors could be utilized in other types of hydrogen production by producing steam for more efficient electrolysis or fossil gas-based steam methane reforming. However, nuclear processes produce radioactive waste, which requires safe disposal and storage in the long term.

White

What: This type of hydrogen is not created by humans; on the contrary it is found as free gas in the Earth’s oceanic or continental crust, in volcanic gas, in geysers, or in hydrothermal systems. This free hydrogen seems to be present in a wide range of rock formations and geological regions. The origin of natural hydrogen although not fully understood, shows signs of viability for technical hypothesis that include natural radiolysis (dissociation of water by plutonium or uranium), decomposition of organic matter, reaction of water with ultrabasic rocks (serpentinization) or reducing agents in the mantle, and degassing of hydrogen directly from the core of the Earth. (Energy Observer)

Current cost: Although white hydrogen is not a known widespread resource, a few projects are already set up to produce it in commercial quantities. It is the cheapest solution to produce carbon-neutral hydrogen and is competitive with fossil fuels. Hydrogen is continuously generated deep inside the Earth and current estimates of the flux provide 23 million ton of hydrogen per year from all geologic sources combined (Solar Impulse Foundation).

Players: Recently, reservoirs containing significant quantities of hydrogen have been discovered. Natural Hydrogen is expected to start drilling for hydrogen in the US continental shelf. Likewise, some white hydrogen deposits have also been found in places like Mali and Australia, which has led to a competition for drilling and exploitation; firms have applied for or gotten 18 exploration licenses for white hydrogen in South Australia. However, the market is still in its infancy.

Future: White hydrogen is being seen as a promising carbon-free and abundant energy resource that needs minimal infrastructure for its exploitation. It has been difficult to evaluate the resources in the world due to a lack of dedicated research in the field. Nonetheless, its value chain is similar to natural gas production and includes prospecting, selection of sites, drilling, and extraction.

One should expect new color codes to emerge with time. Regardless of the origin of hydrogen, there has been an exponential rise in technological advancement and investment in using hydrogen to achieve the ambitious goals of decarbonizing the worldwide economy.