The year 2022 marked a decisive turning point for global energy security. When Russia invaded Ukraine, the shockwaves rippled far beyond the battlefield. Suddenly, the vulnerability of relying on imported oil and gas—especially from politically unstable or adversarial nations—was no longer an abstract risk. In Europe, in particular, energy prices skyrocketed, supplies wavered, and governments were forced to confront an uncomfortable truth: their energy systems were more fragile than they had realized.

In this moment of crisis, nuclear power made a surprising return to the spotlight. Countries that had been phasing out their reactors, or had sworn off building new ones, began to reconsider. Lifespans of existing plants were extended, shutdown reactors were restarted, and fresh investments flowed into new-generation nuclear technologies. At the heart of this revival lies uranium—the fuel that powers the vast majority of the world’s reactors.

Demand for uranium has surged, and with it has come renewed scrutiny of its supply chain, production hubs, and geopolitical significance. No longer just a specialist commodity for a niche industry, uranium is becoming a strategic resource in the race toward both energy security and net-zero emissions.

Uranium’s Enduring Appeal

The reason uranium is so valued comes down to its extraordinary energy density and its ability to generate steady, low-carbon electricity. In a world that is rapidly electrifying, whether it’s through electric vehicles, heat pumps, or industrial electrification, reliable, “always-on” power sources are vital. Unlike wind or solar, which are intermittent, nuclear reactors can operate continuously for months or even years without refueling.

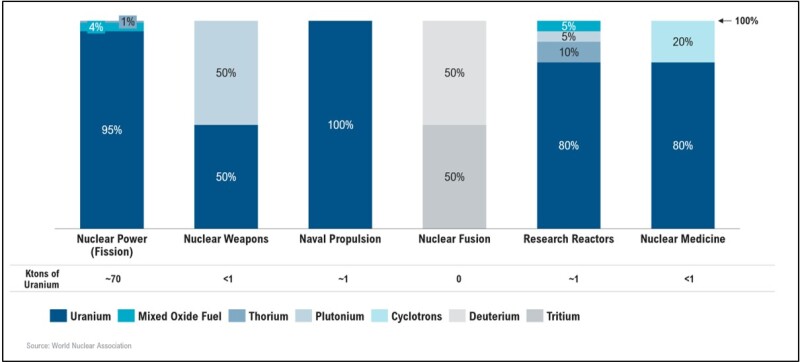

Currently, about 95% of global uranium demand comes from civilian nuclear power plants, which together produce around 10% of the world’s electricity. In some countries, that proportion is much higher: in France, nuclear covers over 70% of electricity needs. The rest of uranium’s uses are more specialized including fuel for naval propulsion in submarines and aircraft carriers, fissile material for nuclear weapons, and certain applications in medicine (Fig. 1).

While alternatives such as plutonium-based MOX fuel or thorium are sometimes used, they remain niche, largely because they require special reactor types or are still experimental. For the foreseeable future, uranium will remain the backbone of the nuclear fuel cycle.

Nuclear and the Energy “Trilemma”

Energy policy is often described as a balance between three goals: security, sustainability, and affordability. Uranium and nuclear energy perform strongly in all three areas.

From a security standpoint, a single uranium fuel load can power a reactor for years, insulating it from sudden price swings or logistical hiccups. Supply chains for uranium are also more geographically diverse than those for some other critical minerals, reducing vulnerability to monopolistic control.

On sustainability, nuclear is one of the lowest-carbon energy sources available. It plays a crucial role in helping countries meet climate goals without sacrificing reliability.

Finally, while nuclear plants are expensive to build, their operating costs are relatively low, and uranium prices have historically been stable. That stability supports predictable electricity costs over the plant’s decades-long life.

Beyond electricity generation, nuclear technology is expanding into new areas such as industrial heat, hydrogen production, desalination, and even space propulsion—each of which could push uranium demand even higher.

A Rising Tide of Demand

The events of 2022 didn’t just give nuclear power a reputational boost; they accelerated concrete investment. Countries have been extending the lives of their reactors, restarting decommissioned ones, and planning fleets of small modular reactors (SMRs)—compact, scalable units that can be built faster and deployed more flexibly than traditional plants.

According to the World Nuclear Association, uranium consumption is projected to grow by more than 30% by 2040, reaching roughly 100,000 tonnes per year. This is being driven not only by established nuclear nations but also by fast-growing markets, particularly China and India.

The Major Consumers

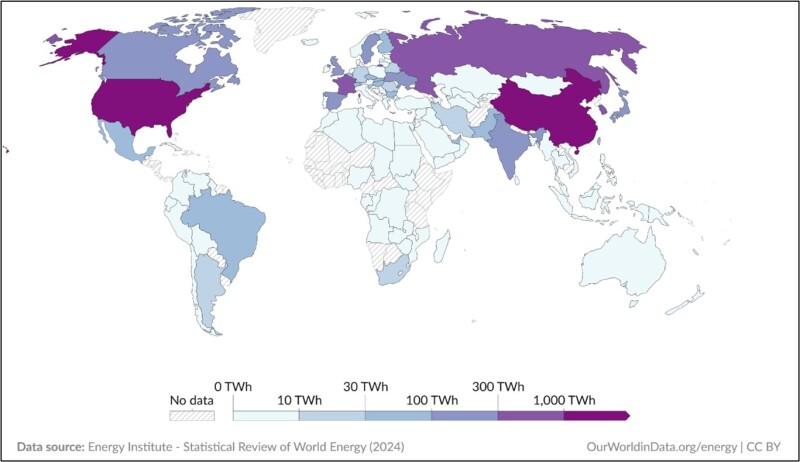

The largest uranium consumers today are a mix of mature and emerging nuclear economies (Fig. 2). The US remains the biggest, thanks to its large reactor fleet, which generates about 20% of the country’s electricity. However, the US produces almost no uranium domestically, relying heavily on imports from countries such as Canada and Kazakhstan.

China is the fastest-growing nuclear market, with dozens of reactors under construction and plans to quadruple capacity by 2050. To fuel this expansion, it has been securing long-term uranium supply deals and investing directly in mines abroad.

France, the most nuclear-dependent major economy, imports uranium from Niger, Kazakhstan, and Canada. It also operates advanced recycling programs, reprocessing spent fuel into MOX to extend its resources.

Russia is both a consumer and a major player in the global nuclear fuel market, supplying enrichment and reactor technology to numerous countries, particularly in Eastern Europe and the Middle East.

India is expanding steadily but faces constraints due to limited domestic uranium. It has long-term ambitions to shift toward thorium, of which it has abundant reserves.

Japan, once a top uranium consumer, saw its demand collapse after Fukushima in 2011 but is now cautiously restarting reactors.

Meanwhile, the Middle East is emerging as a new frontier. The UAE has brought its first reactors online, and Saudi Arabia and Egypt are planning nuclear programs to diversify away from oil and gas.

The Looming Supply Crunch

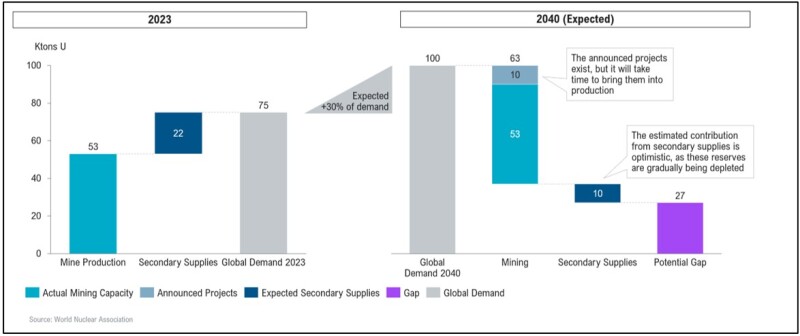

This surge in demand is colliding with a supply picture that is already tight. In 2023, global uranium consumption was over 75,000 tonnes, but mines produced only 53,000 tonnes. The gap was covered by secondary supplies from stockpiles, reprocessed fuel, and other sources—but these reserves are finite and shrinking (Fig. 3).

Adding to the challenge, it can take 7 to 10 years to bring a new uranium mine from discovery to production. This means supply constraints are likely to persist for years, putting upward pressure on prices and prompting utilities to lock in long-term supply contracts.

Where the Uranium Comes From

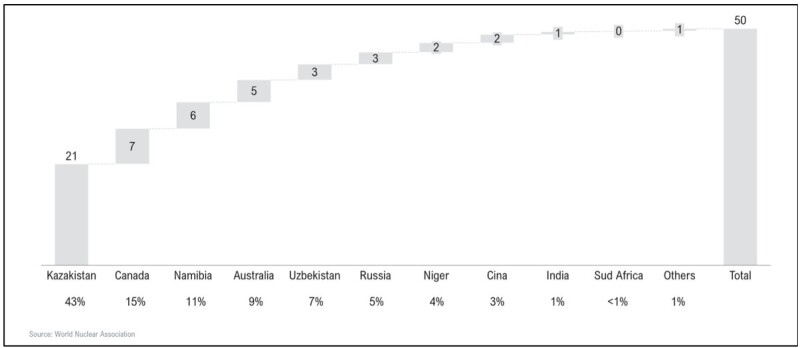

Uranium production is highly concentrated, as seen in Fig. 4. Kazakhstan is by far the leader, providing around 43% of global supply, thanks to low-cost in-situ recovery techniques. Canada is next with about 15%, drawn from some of the richest deposits on Earth in the Athabasca Basin. Namibia follows with about 11%, much of it linked to Chinese investment. Australia holds the world’s largest reserves but produces only around 10%, largely due to environmental regulations and slow permitting.

A handful of other producers—Uzbekistan, Niger, Russia—also contribute, but political instability in some of these countries raises the risk of sudden supply shocks.

Geopolitics and Vulnerability

Recent events have shown just how fragile the uranium supply chain can be. Russia mines only a small fraction of the world’s uranium but dominates the processing side, with nearly a quarter of global conversion capacity and almost half of enrichment capacity.

In Europe, Russia’s role is particularly sensitive due to the continent’s heavy reliance on imported uranium and nuclear services. The EU relies heavily on imported uranium to fuel its nuclear reactors, with virtually no domestic production. Historically, Europe has sourced uranium from a diversified set of countries to mitigate supply risks. Kazakhstan, Niger, and Canada are among the largest suppliers to the EU, collectively covering over 60% of European uranium imports. However, Russia plays a strategic and sensitive role in Europe’s nuclear fuel supply chain, not only as a supplier of natural uranium (accounting for approximately 15–20% of Europe’s uranium imports) but also as a major provider of conversion and enrichment services.

This reliance on Russian nuclear services, particularly for enrichment capabilities, has become a major concern following the geopolitical fallout from the war in Ukraine. While Europe is actively exploring ways to reduce its dependence on Russian nuclear services, the existing infrastructure and contracts — especially in countries with Russian-designed VVER reactors , like Hungary, Slovakia, and the Czech Republic — make this transition particularly complex and politically sensitive. Water-Water Energetic Reactors (VVER), from the Russian Vodo-Vodyanoi Energetichesky Reaktor (Водо-водяной энергетический реактор), are Russian-designed pressurized water reactors (PWR) that use light water as both coolant and moderator, widely deployed across Eastern Europe and exported to countries such as China, Iran, India, and Turkey. As sanctions pressure mounts and utilities seek to diversify supply chains, Russia’s central role poses a major strategic vulnerability for both Europe and global markets, potentially driving long-term shifts in procurement strategies and fuel-cycle investments.

At the same time, the geopolitical fallout from Russia’s invasion of Ukraine has complicated Kazakhstan’s uranium exports to Western markets. Traditionally shipped through the Russian port of St. Petersburg, Kazakh uranium now faces significant logistical challenges, pushing the country to explore alternative export routes (Fig 6).

An alternative corridor through the Caspian Sea and Georgia exists but is significantly more expensive and constrained by serious infrastructure limitations (Fig 7).

More recently, Kazakhstan has revised production targets downward and steered new uranium contracts toward Russia and China, leaving Western buyers uneasy. The increasing alignment with Russia and China reflects a broader trend of "resource nationalism," where governments assert stronger control over natural assets not only to maximize national revenue but also to pursue geopolitical objectives. In the case of Kazakhstan, uranium is increasingly treated not merely as a commercial commodity but as a strategic asset—a tool of foreign policy in a multipolar world.

Niger, a key supplier to France, underwent a military coup in 2023 that disrupted mining operations and led to disputes with French nuclear company Orano. Niger, which is a key uranium supplier to Europe, particularly France, suddenly became a geopolitical flashpoint as the new government suspended military cooperation with Western countries and reviewed foreign mining contracts. France, historically dependent on Nigerien uranium to fuel its extensive nuclear fleet, faced uncertainty over long-term supplies.

These flashpoints underscore how concentrated uranium production leaves the global market exposed to political turbulence.

Rebuilding Control Over the Fuel Cycle

In response, many Western countries are working to secure greater control over the entire nuclear fuel cycle. This means not only mining uranium but also ensuring domestic capacity for conversion and enrichment, stages where Russia currently has significant leverage—especially for high-assay low-enriched uranium (HALEU), essential for advanced reactors.

The US has begun small-scale HALEU production, but volumes are far below future needs. France continues to lead in reprocessing, while countries like Spain are considering lifting mining bans to tap domestic resources. Canada, Australia, and the UK are strengthening multisource procurement strategies to improve resilience.

The goal is clear: build diversified, reliable supply chains that are insulated from geopolitical shocks.

A Market in Motion

After years of low prices following the Fukushima disaster, uranium has staged a strong comeback. Spot prices have more than doubled between 2021 and 2024, driven by reactor restarts, life extensions, newbuilds, and mounting supply concerns. Utilities are increasingly securing long-term contracts to shield themselves from volatility, and the overall market outlook points toward sustained upward price pressure.

Looking Ahead

Nuclear power’s attributes—near-zero emissions, high reliability, and scalability—make it an indispensable part of the low-carbon energy future. But with the uranium market already under strain, its role comes with challenges: a structural supply deficit, geopolitical instability in key producing countries, and the slow pace of developing new mines and processing infrastructure.

As the market becomes more fragmented and politicized, access to uranium will increasingly depend on strategic alliances and national interests. For policymakers and industry leaders, ensuring a stable, sustainable uranium supply is no longer just a technical challenge—it’s a central question of energy security in the decades to come.

For Further Reading

World Nuclear Performance Report, by World Nuclear Association, 2023.

Global Nuclear Energy Consumption in 2024, by Our World in Data, 2025.

World’s Largest Uranium Miner Warns Ukraine War Makes it Harder to Supply West, by H. Dempsey and A. Stognei, Financial Times.