Global demand for natural gas is expected to drive floating liquefied natural gas (FLNG) capacity to 42 mtpa by 2030, before rising to 55 mtpa by 2035. The figures represent a three- and nearly fourfold increase over the 14.1 mtpa of installed FLNG capacity as of 2024, according to a new report from Rystad Energy.

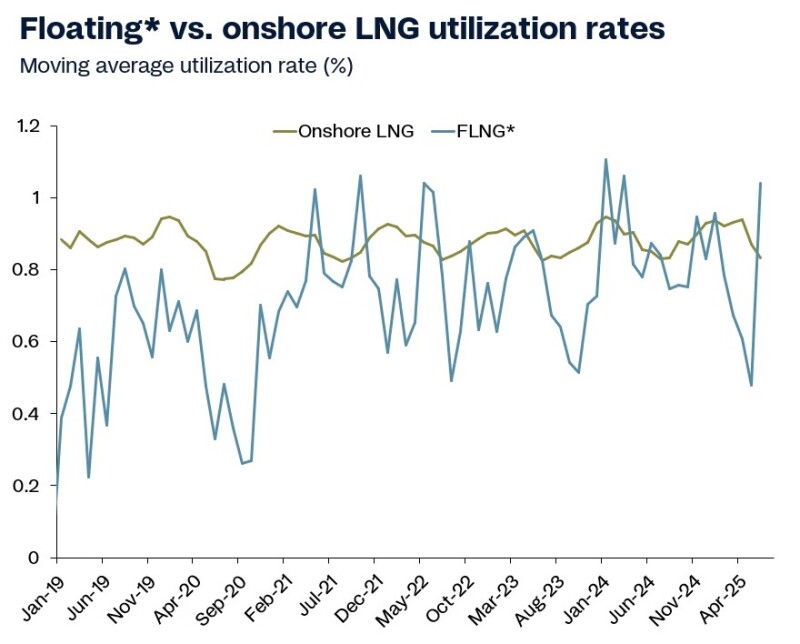

Rystad also found that utilization rates for FLNG facilities built prior to 2024 topped 86% last year and have reached 76% so far this year, which it said are on par with the utilization rates of onshore LNG terminals.

The market research firm said momentum is building for FLNG after the earliest of these megaprojects faced significant technical and operational setbacks. Rystad noted that FLNG is now viewed as a relatively fast and cost-competitive solution for monetizing otherwise stranded gas reserves.

“FLNG has come a long way in less than a decade. The only real roadblocks were early teething issues that come with any new technology, as seen with projects like Shell’s Prelude, which faced cost overruns and unstable output,” Kaushal Ramesh, vice president of gas and LNG research for Rystad, said in a statement.

Commissioned in 2018, the Prelude was celebrated as the largest floating structure ever built. But as the first-of-its-kind FLNG facility, the 488-m-long vessel also experienced several high-profile technical issues and operational errors that led to major supply disruptions.

Rystad noted that Shell paid the price for being a pioneer, calling the Prelude “a negative demonstration of FLNG’s early limitations.” The research firm estimated Prelude’s cost of supply reached $2,114 per metric ton (Mt), though it added that the floating facility, along with the wider FLNG sector, has turned a corner and found ways to lower costs.

From LNG Tanker to FLNG Facility

One way developers are cutting costs is by repurposing older LNG tankers rather than building new floating facilities. The vessels can operate in deepwater or be moored nearshore to process gas from onshore fields. Once production dries up or becomes uneconomic, they can be redeployed or sold.

Rystad said the conversion approach also takes advantage of the vessels’ existing spherical storage tanks, which integrate relatively easily with prefabricated liquefaction modules.

As more LNG carriers near retirement, Rystad said the pool of low-cost candidates for FLNG conversion is expanding. The firm reported earlier this year that a glut of LNG vessels includes more than 80 tankers over 20 years old, many of which could be used for FLNG.

Another advantage of FLNG is shorter delivery times, with projects typically taking around 3 years to reach completion, compared with 4.5 years for similarly sized onshore facilities. Rystad found current FLNG projects that are still under construction are on track for completion in just 2.85 years, helping drive boardroom support for reaching a final investment decision (FID) on future projects.

Rystad pointed to examples of cost efficiency, including Golar LNG’s Greater Tortue Ahmeyim FLNG project offshore Mauritania and Senegal ($640/Mt) and its Cameroon FLNG ($500/Mt), along with Southern Energy’s FLNG MK II offshore Argentina ($630/Mt).

Costs are higher in the US, where proposed FLNG projects are averaging $1,054/Mt which is close to the $1,062/Mt reported at Eni’s Coral South project offshore Mozambique, which began exports in 2022 as Africa’s first FLNG facility. Eni is considering building a second FLNG facility offshore Mozambique and as a cost-saving measure will use the same design as the first if an FID goes ahead as expected later this year.

However, it is difficult to compare costs between projects on a like-for-like basis, Rystad explained, as they depend on whether the facility includes upstream elements or is built solely for gas liquefaction.