The US continues to boom at record levels. Venezuela is in production freefall. And other members of the Organization of the Petroleum Exporting Countries (OPEC) have agreed to gently open the spigot on spare capacity starting this month.

This is a snapshot of the driving forces behind the world’s crude market. The US Energy Information Administration (EIA) says in its most recent energy outlook that this may all lead to an uptick in prices for the rest of this year before the balance is disrupted and we see them walked down a few dollars per unit in 2019.

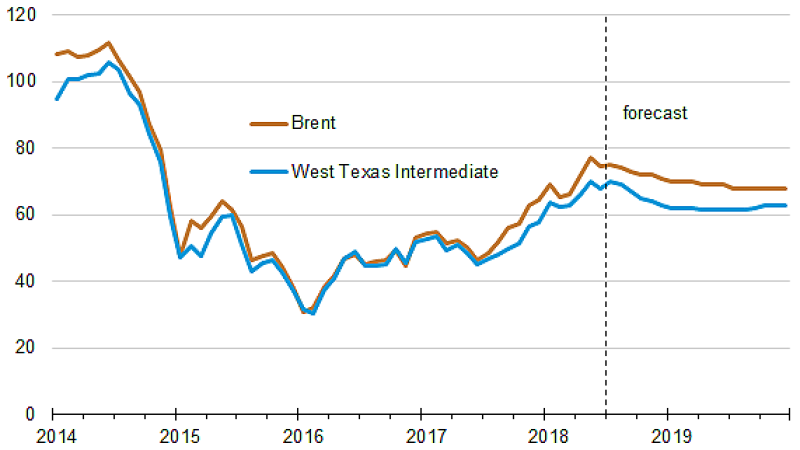

The forecast calls for West Texas Intermediate (WTI) to average at $66 for the remainder of 2018, compared to $73 for Brent crude. In the first half of next year, average WTI prices may then drop to around $62 with Brent hovering closer to $69.

Supply growth into next year is projected to outpace global demand, brining markets once again into a state of relative imbalance.

The estimates are partly backed on global fuel inventories which declined by 500,000 B/D in 2017, went mostly unchanged this year, but are expected to increase by 600,000 B/D in 2019. The bulk of that buildup will come from the US, Brazil, Canada, and Russia, according to projections.

About 2.2 million B/D out of 2.4 million B/D will come from these four non-OPEC nations. “Supply growth of this magnitude would outpace EIA’s forecast for global liquid fuels consumption growth of 1.7 million B/D for 2019,” the report said.

It is also expected that the US will top 10.8 million B/D in average production for this year, which amounts to an increase of 1.4 million B/D over 2017’s figure, and then in 11.8 million B/D may be reached in 2019.

“If realized, the forecast level for both years would surpass the previous US record of 9.6 million B/D set in 1970,” said the EIA. “Crude oil production at these forecast levels would probably make the United States the world’s leading crude oil producer in both years.”

The agency attributes half of the production surge to come from the highly active Permian Basin region in Texas and New Mexico where more rigs are running than in any other spot on the planet. The other half of the forecast is to come from other shale plays including the Bakken and Eagle Ford, along with the US Gulf of Mexico.

OPEC meanwhile is seeing a lower surplus production capacity this year and that might be the most important factor to watch with regard to oil prices. The EIA notes that if additional supply disruptions take place, or production targets are not met, then prices could continue their rise.

The big figure to monitor: 31.9 million B/D a day. That is OPEC’s projected daily production average for all of this year, and it may dip by less than 100,000 bbl next year.

The strength of this EIA prediction rests on the future of Venezuela, which amid an ongoing economic and political crisis has seen its crude production plummet from 2 million B/D this time last year to about 1.4 million B/D today. Together with Iran, which is facing unilateral sanctions from the US that intend to curb its exports, the two OPEC countries may account for a combined 1 million B/D production decline.

However, other OPEC members—Saudi Arabia, Kuwait, United Arab Emirates, and Qatar—will likely make up for these declines after agreeing this summer to begin loosening up the landmark production cuts that have helped stabilize the market over the past 2 years.