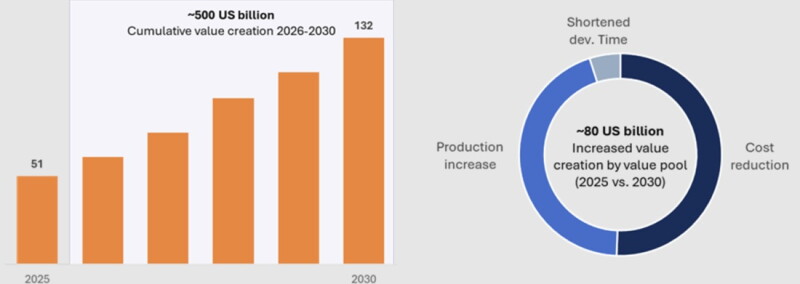

Digitalization and artificial intelligence (AI) could create close to $500 billion in cumulative value for exploration and production (E&P) companies between 2026 and 2030, according to Rystad Energy estimates. This value would be captured through cost reductions from more-efficient operations, production increases from higher uptime and increased recovery, and compressed development timelines (Fig. 1). Rystad said cost reductions and production increases are the largest value pools, contributing roughly equally through 2030. E&P companies currently investing in digital and AI are expected to capture an additional value of $80 billion per year in 2030 compared with 2025.

Rystad said it sees the benefits already emerging, pointing to the Abu Dhabi National Oil Company’s recent report of $500 million in AI-driven value in 2023. The UAE giant has committed $1.5 billion in digital capital expenditure, targeting $1 billion in annual value creation. Norway’s Equinor said it generated around $200 million in AI-related savings between 2021 and 2024, before reporting $130 million in 2025 alone.

The trajectory, however, appears not to be linear. Rystad says digital value creation follows a compounding curve as adoption increases and organizational capabilities mature.

The $500 billion value creation opportunity in upstream oil and gas sits across four main workflow categories, according to Rystad. The first, asset development, and second, operations and maintenance, relate to mostly surface workflows. The third, exploration and reservoir development, and fourth, drilling, wells, and production, represent subsurface-focused workflows. Each appears to be at a different stage of digital maturity, Rystad said.

Historically, operators have deployed a wide range of digital tools into various workflows, especially within exploration and reservoir development. When it comes to newer deployments, operations and maintenance is seeing more rapid adoption, primarily through predictive maintenance and remote operations, Rystad said. Subsurface workflows hold the largest untapped value potential, according to Rystad, especially from getting more volumes out of the ground and reducing drilling costs.

A key structural finding across all four workflow categories is that AI, in general, does not necessarily raise the ceiling for the best operators; it lifts the rest of the industry toward the performance level that the best operator already achieves. In drilling, the dynamic is already visible as leading US shale operators are close to physical drilling limits, where the best wells can still improve, but the biggest effect would come from lifting the average well. Rystad estimates that, for US land, the average improvement potential is close to 10%, while, for more complex deepwater wells, the potential savings can be far greater—more than 50% in more extreme cases, although between 15 and 20% is more representative of the average.

Capturing the value at stake requires investment in digital tools, infrastructure and integration, and E&P companies are estimated to have spent around $25 billion on digital and AI purchases last year. The market for providing these tools and services is expected to grow by more than $10 billion by 2030, surpassing $35 billion in total annual market size, before growing closer to $50 billion by 2035.

The early adopters of these technologies typically have digitalization and AI as an integral part of their strategy. Rystad said that conversations with various industry stakeholders highlight that organizational readiness determines the realistic pace. Traditional cloud migration can take multiple years, while cross-silo collaboration requires cultural shifts that no software can automate. Beyond adopting off-the-shelf solutions, some of these players seek to develop their own solutions in-house to gain a competitive advantage over the rest of the industry.

Rystad said that the central barrier to capturing this value, however, is not technology availability but deployment at scale. Advanced E&P companies, and those with fewer capabilities to start, opt for partnerships with suppliers and technology experts to reduce complexity and simplify integration across equipment, assets, and different parts of their organization, typically through platform solutions. Rystad said it sees traditional oilfield service providers with domain expertise and technology experts such as integrators or hyperscalers as among the more important partners for E&P companies seeking to translate digital investment into operational returns. These projects see the commercial model shift from transactional service delivery toward integrated technology partnerships that can then leverage an ecosystem of players, platforms, and scalable tools.

Rystad said it sees a scenario where AI accelerates value creation further than the base case, where breakthroughs simplify integration and compress adoption timelines industrywide. In this scenario, Rystad said, annual value creation from digital initiatives reaches $150 billion in 2030, with the potential to grow past $300 billion by 2035, compared with the base case of $178 billion in 2035.

Rystad added that the accelerated AI scenario would require additional spending on digital solutions, up to $50 billion annually in 2030 and close to $80 billion by 2035.