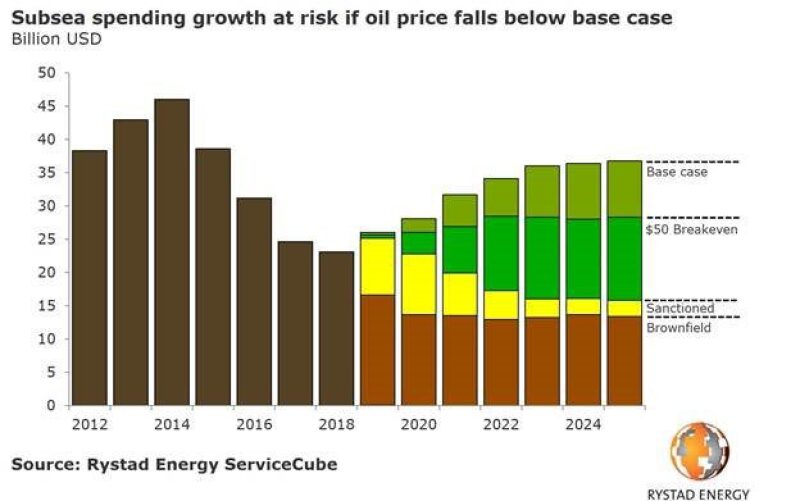

The subsea market in 2019 will experience year-on-year growth for the first time since 2014, but the positive outlook is vulnerable to any significant decline in oil prices over the next few years.

Rystad Energy expects the subsea market to thrive during the coming years, but market growth will be at risk if the oil price falls to $50 per barrel.

An analysis of the outlook for global subsea segments in the coming years forecasts that development this year is essentially locked in with brownfield opportunities and already-sanctioned projects—but the oil price will dictate growth moving forward.

In a $60 to $70 oil environment, the subsea market is poised to grow around 7% annually up to 2025. But a significant portion of this activity is at risk if the price of Brent crude falls to $50 per barrel. We believe prices at that level would still be enough to support 5% annual growth in the subsea market through 2022, but after that the growth rate could fall to zero.

Although we expect the subsea market to have one of the highest growth rates within oilfield services, the segment is also more vulnerable to an oil price drop than the oilfield services market in general. We see significant risks in terms of subsea spending as well as growth.

Segments with especially high exposure to greenfield activity, such as the subsea equipment and SURF (subsea umbilicals, risers, and flowlines) segments, are at risk of having growth slashed by almost 5 percentage points per year. This stands in stark contrast to the oilfield services market as a whole, which exhibits around 3 percentage points growth at risk over the same timeframe.

This trend is echoed when we look at spending at risk from 2019 through 2025 – close to 20% of spending in the subsea equipment and SURF segments is at risk, while around 10% of general oilfield services market spending is at risk should the oil price fall from our base case estimate to $50 per bbl.

Examining the subsea spending risks more closely, we see that Brazil has several projects with breakeven prices around $50 per barrel.

Spending at risk is largely dominated by floater projects globally, but in Norway is manifested in subsea tieback projects. No fewer than 16 projects with subsea expenditure between 2019 and 2025, are at risk on the Norwegian Continental Shelf, 14 of which are subsea tieback projects.

It is worth mentioning that operators have had a remarkable ability to cut costs during downturns, much helped by the oilfield service industry. Should a lower-price environment again become reality, we can be assured that the industry has a proven track record of survival and ingenuity.