If natural gas is the new oil, then LNG is the engine driving global mega infrastructure investment and powering growth in upstream exploration and development to ensure sufficient supply for liquefication well into the 2030s and beyond.

Shell’s LNG Outlook 2025 forecasts a 60% rise in demand for LNG by 2040, driven by economic growth across Asia, decarbonization in heavy industry and transport, and rising energy needs driven by artificial intelligence.

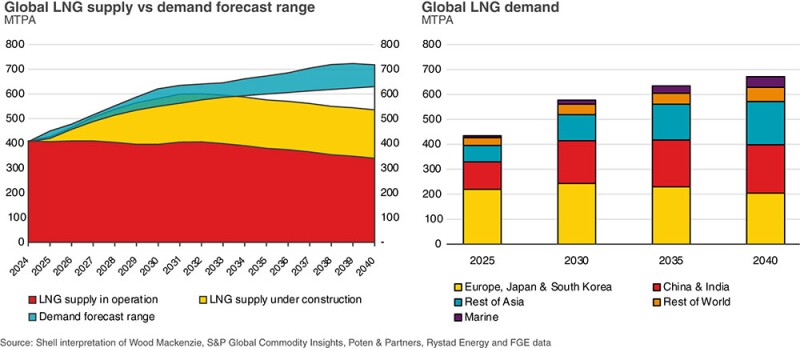

While global demand is set to rise over the next 15 years, new production capacity starts to decline in 2034, setting the stage for a widening gap between supply and demand, according to Shell’s outlook (Fig. 1).

The International Gas Union (IGU) red-flagged a decline in final investment decision (FID) activity in 2024, noting in its 2025 World LNG report that the approximately 15 mtpa of new liquefaction capacity reaching FID last year was the “lowest annual approval volume since 2020 and well below the 58.8 mtpa greenlighted in 2023.”

Whether that’s cause for concern depends on the volume of pre-FID projects in play and the industry’s appetite for investing in a critical mass of those projects. As a new investment cycle begins, the aging project pipeline needs refilling.

North America led the world in pre-FID activity in 2024, with proposals for approximately 648 mtpa in new aspirational liquefaction capacity, mostly in the US. Projects in Canada and Mexico also contributed to the region’s lead.

The North American figure outpaced No. 2 ranked Russia’s 170 mtpa in pre-FIDs by a factor of three, with Africa finishing a close third at 133 mtpa, according to the IGU report.

The Middle East proposed 66.5 mtpa in pre‑FIDs in 2024, closely followed by Asia Pacific at 67.0 mtpa, while the rest of the world contributed 36 mtpa.

US Strives To Maintain Dominance

Since the US lifted its permitting pause in January, it has accounted for nearly 95% of all new LNG capacity sanctioned globally in the first half of 2025, according to the International Energy Agency (IEA) Global LNG Capacity Tracker.

Already-sanctioned projects are expected to bring nearly 295 Bcm/year of new LNG export capacity onstream by 2030, marking the largest wave of capacity additions to date, the IEA noted.

Given that the IEA 2030 estimate for new export capacity excludes pre-FID activity, that wave of LNG development could become a tsunami.