The UK Continental Shelf (UKCS) continues to serve as an operating environment where innovation is not optional but fundamental to sustaining production efficiency, maintaining asset integrity, and achieving emissions-reduction targets. Historically, the basin has incubated a range of subsurface, drilling, and facilities technologies that ultimately resulted in the recovery of billions of barrels of oil and gas. That innovation is now being redirected toward net-zero requirements, electrification, and technologies that support carbon storage and low-carbon hydrogen value chains.

As part of its regulatory and stewardship responsibilities, the North Sea Transition Authority (NSTA) compiles operator-level data on technology deployment and near-term development plans. This information, gathered annually through the UKCS Stewardship Survey, provides a basinwide view of uptake, maturity, and technology readiness levels (TRLs).

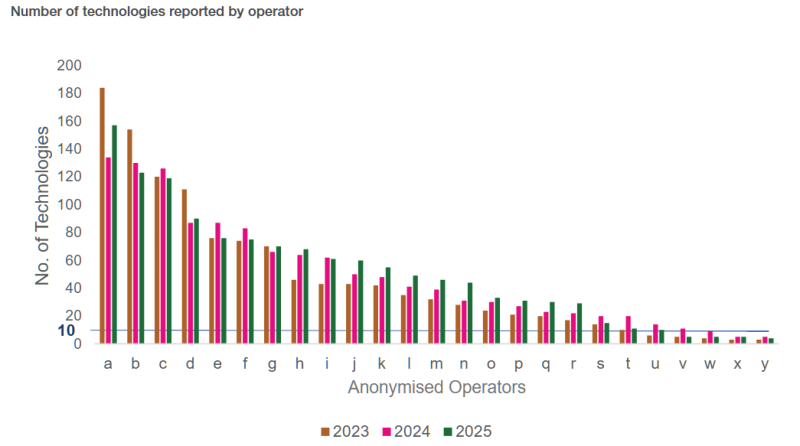

The 2025 data set reflects submissions from 46 operators, with technology inventories and development plans submitted by the end of February 2025.

Among the operators’ reported advances were electro-hydraulic devices which emit precision pulses to remove scale deposits that restrict wellbore flows and innovative bubble-based systems, developed in north-east Scotland, to improve the separation of oil from produced water. Microbial-enhanced recovery has emerged as a powerful tool, with injected microbes breaking up trapped oil droplets within reservoirs. Subsea tieback solutions, supported by remotely operated pumps and gas compression systems, are making a difference in connecting smaller or marginal fields to existing infrastructure. Emerging interventions also include reservoir-cutting lasers, successfully piloted onshore in the Middle East, which create clearer flow paths for hydrocarbons.

Technology Inventory Overview

Operators reported 1,280 distinct technologies, an increase on the previous year’s 1,250. Approximately 50% of these solutions have been field-proven, while 141 entries were newly reported in 2025. Technologies that have already become industry-standard practice, as well as concepts that failed to progress beyond initial screening, were excluded to ensure the analysis concentrates on innovations with demonstrable or emerging impact.

Distribution across life-cycle stages shows a broad spread of activity:

- 40%—New asset development

- 45%— Asset operations and production optimization

- 14%—Decommissioning and well P&A activities

Digitalization and net-zero-aligned solutions now cut across all categories and exhibit the strongest year-on-year growth.

Detailed Technical Highlights

Analysis of the 2025 submissions shows a concentration of innovation in four core domains where technology deployment is directly improving operational efficiency, asset integrity, and emissions performance.

The following subsections outline the technologies referenced by operators, with emphasis on tools and systems that have demonstrated measurable performance in UKCS conditions or are advancing rapidly through field trials. These technologies reflect operators’ prioritization of reduced nonproductive time (NPT) in well construction, improved facility reliability, production optimization, and tangible reductions in Scope 1 emissions across existing assets.

1. Drilling and Well Construction

Operators are deploying a suite of technologies aimed at reducing well-construction NPT, optimizing wellbore placement, and improving safety system reliability.

- Modular and lightweight platform drilling packages to reduce rig-up complexity and improved deck-load management

- Single-lift well-to-well transfer systems to decrease intervention cycle time and personnel exposure

- Logging-while-drilling sonic tools for accurate top-of-cement determination to improve barrier verification and cement integrity assurance

- AI-driven digital well planning integrating offset-well data, dynamic modeling, and probabilistic risk assessment

- Combined wireline tool strings to minimize runs and reduce mechanical wear and rig utilization

- Tubing-retrievable surface-controlled subsurface safety valves to enhance fail-safe well barrier performance and simplifying workovers

2. Facilities Engineering, Inspection, and Automation

Advancements in topsides and subsea facility design are concentrated on reliability, remote operation capability, and reduction of intrusive inspection.

- High-frequency vibration and axial load analytics for early anomaly detection in rotating equipment and critical flowlines

- Extended-reach subsea tieback technologies to enable marginal-field development with lower capex

- Subsea gas compression and multiphase boosting to maintain reservoir drawdown and enhance late-life production

- Nonintrusive inspection using advanced electromagnetic, acoustic, and radiography techniques to reduce vessel shutdowns

- AI-enabled risk-based inspection models which integrate real-time sensor data and historical degradation mechanisms

- Automation and advanced process control systems to stabilize operations and optimize heat, power, and compression loads

3. Well Intervention and Production Optimization

Technologies designed to restore or enhance well deliverability are seeing sustained uptake.

- Wireless downhole surveillance for distributed temperature and pressure sensing without permanent cable installation

- Disposable fiber-line systems for rapid data acquisition and simpler rig-up workflows

- Retrofit downhole safety valves and electrical submersible pumps to extend well life without major recompletion

- Advanced zonal isolation materials and expandable elastomers for remediating complex flow-path geometries

- Real-time slickline and coiled-tubing telemetry systems to improve decision-making during live interventions

- Water-shutoff chemistries to target high-salinity environments and heterogeneous reservoir flow regimes

4. Emissions Reduction and Low-Carbon Operations

Operators continue to prioritize technologies that directly reduce Scope 1 emissions.

- Flare gas recovery units and vapor recovery systems to lower routine and nonroutine flaring

- High-resolution emissions monitoring, including methane-specific sensors, infrared imaging, and flare efficiency-measurement instrumentation

- Platform electrification options, including grid-tie, floating wind integration, and hybrid microgrid architectures

- Hybrid energy systems combining battery energy storage with reduced-load gas turbines

- Emissions monitoring during wellsite activities to extend measurement coverage to drilling and intervention operations

Technology Sourcing and Collaborative Development

Technology sourcing patterns in 2025 indicate a more proactive approach to innovation management across the basin. Sixty-one percent of reported technologies were sourced directly from vendors or OEMs, reflecting a growing reliance on commercially available solutions. Another 22% originated from operator–supplier co-development efforts or participation in joint industry projects. The Net Zero Technology Centre contributed 5% of the technologies through its targeted funding, piloting, and accelerator initiatives. Additionally, 21 operators reported deploying more than 10 distinct technologies, signaling their organizational commitment to structured technology maturation across the TRL framework.

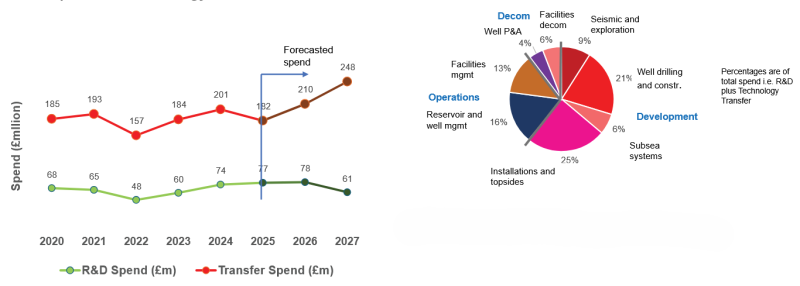

Expenditure Patterns in R&D and Deployment

For 2025, operators forecast £77 million (USD 101 million) in direct technology R&D expenditure—broadly consistent with recent historical spending but lower in real terms compared with pre-2015 levels due to inflation. Key observations include:

- Technology transfer costs, the capital required for deployment, continue to rise as a larger portfolio enters field trial and implementation phases.

- Development-stage activities capture the largest portion of total technology spend (61%), indicating prioritization of near-commercial solutions over early-concept research.

- Spending trends suggest a maturing innovation pipeline in which the focus has shifted from basic research to the deployment of technologies in the field as the main driver of investment.