As digital innovations such as artificial intelligence, cloud computing, automation, and the Internet of Things (IoT) become more readily usable, energy companies are developing strategies that incorporate these burgeoning systems into their operational infrastructure. Distributed ledger technology—otherwise known as blockchain—may be the backbone of this new infrastructure.

Already well-known in the financial sector, blockchain is a peer-to-peer (P2P) network technology that uses advanced computer science techniques to enable trustworthy interactions between parties, even if those parties do not trust each other. It is a shared electronic ledger in which access can be managed by multiple sources, including anonymous ones. Proponents say blockchain is reliable and likely to change the way in which energy companies perform transactions.

Operators are already working with various blockchain platforms, but the developers of these platforms are still forging a path that they hope will lead to widespread adoption within the industry.

The Mechanics of Blockchain

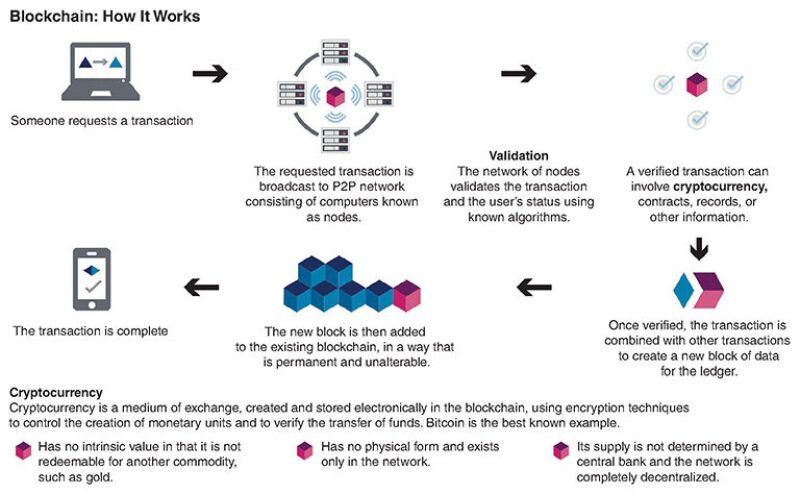

Fig. 1 illustrates the basics of a blockchain platform. An entity requests a transaction, the transaction is broadcast to a P2P network, validated, combined with other transactions to create a block of data within a ledger, and added to a chain of previous transactions in a way that is permanent and unalterable. These transactions can represent anything, from the exchange of numbers of digital assets to the acceptance of a trade of a digital commodity that can be audited by a third party for authenticity without revealing sensitive information. The blockchain ledger can be shared with all members at all times. It is not stored in one place, and there is full transparency—companies can control exactly which information gets shared and with whom.

A blockchain entry can include executable computer code that reflects the terms of the contract, creating a smart contract that automatically validates transactions without the need for human intervention. A smart contract self-executes code that enables straight-through processing and eliminates the need for manual intervention in the execution of a transaction. Smart contracts can mimic regular contracts and execute the contract automatically if the conditions required to consummate the contract are met.

Jerry Bailey, director and president of Petroteq and a former senior executive engineer at Exxon, compared blockchain to traditional means of storing information.

“We all have had big file cabinets, big file rooms all through the years,” Bailey said. “You go into a file room and find dozens of file cabinets. Everybody had a key to the file room but not everybody had a key to each of the file cabinets, depending on what their part in the company was. Blockchain is like this to me. It sets up a system where not only the company, but our vendors, our suppliers, and our buyers can look into the appropriate file cabinet, as it were.”

Writing about blockchain in a report for Deloitte, Mike Prikop and Mark Koeppen looked at four areas where oil and gas operations may be a good fit for blockchain applications.

- Energy transactions. Providing a platform for executing and recording transactions, and for tracking ownership as assets change hands before settlement. With blockchain, transactions can be recorded and settled immediately, with no need for an intermediary and with little or no need for reconciliation since all parties are using the same platform. There is essentially nothing to reconcile because there is only one system and one entry for the transaction, which is shared by all parties.

- Regulatory reporting and compliance. Enabling transparency by allowing regulators to securely access tamper-proof data at the source, while also allowing strict control over which information is available and who is allowed to access it.

- Asset optimization across sectors. Making optimal management decisions amidst interactions with suppliers, vendors, and counterparties that may drive up complexities within a project.

- Global supply network. Creation of a platform that supports the end-to-end process of the exploration, production, refinement, and delivery of hydrocarbons that incorporates every entity in the process, from operators to government inspectors to individual service providers.

Prokop, a managing director at Deloitte Risk and Financial Advisory, said that blockchain’s effect on supply chain management could also apply to the physical transaction life cycle, which he said was similar in many ways to the supply chain.

“You have the dockworkers, the folks who own the tankers and lease them, and then you have two counterparties: one with oil and one without oil who wants to receive it. That entire supply chain, if you will, is able to apply their services and their reporting responsibilities onto a blockchain so that the two counterparties can actually see if the transaction is moving along like it is expected to.”

Blockchain Use Cases

Operators have already begun making use of the technology. BHP Billiton uses blockchain to record movements of wellbore rock and fluid samples, and better secure the real-time data it generates during delivery. Last year BHP began requiring its vendors to use blockchain to collect live data, and it is running its own nodes on the InterPlanetary File System, a peer-to-peer sharing protocol that is commonly used in conjunction with blockchain systems.

Last November, BP, Shell, and Statoil announced the joint development of a blockchain-based digital platform for energy trading. The platform, which is scheduled to be operational by the end of this year, will manage physical energy transactions from trade entry to final settlement. Pending regulatory clearance, it will be open to the entire commodity industry after initial testing by the investor companies. Over time, the companies intend to lead the migration of all forms of energy transaction data to the blockchain.

“The blockchain-enabled energy enterprise can be visualized today,” said BTL Group CEO Dominic McCann. “Imagine gas pipelines, equipped with connected sensors, communicating securely and reliably with one another, autonomously updating volume, temperature, and flow pressure measurements in real time over a platform that does not require costly central IT infrastructure to broker information,” he said.

Since 2015, BTL has been building Interbit, an industry-agnostic blockchain platform soon to be released publicly. Interbit was written in JavaScript and designed off the Redux pattern, which helps manage the data displayed and how responses are made to user actions. It enables the creation of an unlimited number of connected blockchains to improve scalability and protect privacy. BP and Eni tested Interbit over a 12-week period by carrying out trades in European natural gas, and last June the companies agreed to run blockchain trades in parallel with their live trading systems.

Last year, Petroteq announced that it was developing Petrobloq, a blockchain-based oil and gas supply chain management platform, along with First Bitcoin Capital Corp. The platform will be designed to improve efficiencies in facilities management, allowing for continual operations management through the collection of data from a network of IoT-backed sensors.

Petrobloq joined the Enterprise Ethereum Alliance in December, the world’s largest open-source blockchain initiative. The following month, the company announced a deal with Grupo Pelge, Pemex’s international liaison, to represent its interests in Latin America. As part of the deal, Petroteq will register as a service provider through the Pemex management portal run by Achilles Information, a provider of a global network of collaborative industry communities that allows trading partners to share structured, real-time data. Once registered, Petrobloq will provide Pemex and other affiliated companies with a supply chain management system.

Bailey said companies that do not invest in blockchain platforms will not get “left behind” in the event of widespread adoption, but may end up ceding a competitive advantage to competitors targeting similar groups.

“Say you’re a service company trying to get your services out to other oil and gas companies. You may find that the people who are hooked into those companies’ blockchains may be able to get their questions answered or get their bids in quicker. You might find that there will be a period where you could be at a disadvantage to your competitors,”Bailey said.

Barriers to Adoption

One of the consensus opinions in discussing blockchain is that education is one of the biggest hurdles to widespread adoption from energy companies. Bailey said part of his role in building support for Petrobloq is explaining exactly what blockchain is to interested companies.

“We don’t understand. How is this going to help? In the oil and gas business we don’t make changes very easily—if it ain’t broke, don’t fix it. Anything new that comes along takes a lot of education,” Bailey said.

That education extends to the government bodies developing blockchain-based regulatory platforms. Last year, Deloitte partnered with Irish Funds to develop a proof of concept focused on assessing the application of blockchain technology in meeting regulatory reporting requirements within the fund industry. This led to the development of RegChain, a platform that acts as a central repository for the safe storage and review of large volumes of regulatory data.

Although RegChain was developed for finance, Prokop said the work done in this space is applicable to oil and gas because of its adaptable nature.

“This is the great thing about blockchain. It’s compatible across industries for many of these platforms, so work that you’ve done in banking, in pharma, in the automotive industry, can be applied very simply to energy and resources,” he said.

In the US, the Commodity Futures Trading Commission (CFTC) created LabCFTC as a focal point to promote innovation in financial technology and serve as a platform for the commission’s understanding of new technologies. It includes a dedicated point of contact for developers to engage with the CFTC, learn about its regulatory framework, and obtain feedback and information on the implementation of new technology ideas on the market. The commission said this feedback was designed to help developers save time and money at the early stages of development.

Prokop said LabCFTC created an environment where energy companies and those engaged with energy companies can come together and work with the regulator in an off-production environment. Additionally, he said that RegChain’s acceptance in the European Union and in Asia are other positive signs. Koeppen, a principal at Deloitte Consulting, thinks regulators can go even further with their involvement in blockchain.

“I do think the regulators could be even more forward-thinking and develop their own blockchain solutions,” Koeppen said. “We’ve talked about putting land title records on blockchain so that they would be digitized and no longer simply stored in courthouses, needing people to go file through them. The environmental regulators could build out their solutions so that they are actually the ones bringing technology to bear. Why can’t they set the standards for the solutions? That’s where I’d like to see them go.”

While education is an important hurdle for both industry and regulators, Koeppen said another major hurdle is the overall acceptance of the consortium model of doing business. Blockchain has the power to be a transformative technology, but that technology requires a lot of participants to be on board with a way of working that is much different from how they have worked in the past.

“In the past I was responsible for my ledger, my transactions, and I shared with you when you needed to get a service but I still kept my book of record,” Koeppen said. “Well, if we start talking about having a shared book of record that people can see the parts they need to see—even if they can’t make changes they’re not allowed to make—that’s fundamentally changing the entire conversation about the way we do business. If I can prove to you that this service was provided, and the time it was provided basically in real time, and you can see the same thing I see when the work is done, why do I need to invoice you?”

Cryptocurrency Future

Many people think of blockchain as the public transaction ledger for the cryptocurrency bitcoin, the first digital currency to work without a central bank or a single administrator. Bitcoin has fluctuated in value recently after consistent growth in its first 9 years of existence. The value of a bitcoin rose from $800 in January 2017 to $17,900 on 15 December 2017 before experiencing a dramatic drop. It lost one-third its value on 22 December, and over a 16-day period in late January and early February it fell a further 50%. As of 5 April, it was $6,768.

Industry proponents of blockchain in oil and gas have been careful not to emphasize its connection to cryptocurrency—Prokop described it as “more of an infrastructure and a vehicle for the transfer of information rather than something that holds an intrinsic value”—but this does not mean that cryptocurrency has no future in the industry. Koeppen said he has heard discussion of a digital coin based on the value of a barrel of oil, and while he thinks blockchain has potential on its own separate from bitcoin, he said cryptocurrency may have long-term potential with oil and gas.

“It’s certainly something that’s started to gain interest, like, how would we do that?,” Koeppen said. “Bitcoin is enabled for us by blockchain, it’s probably the biggest, well-known usage of blockchain, so it does have value for us.”

Bailey also said that Petroteq had discussions about an oil-backed cryptocurrency. These discussions have been theoretical and are not the primary focus of Petrobloq’s efforts, but he sees a future in cryptocurrency that might evolve out of the industry’s use of blockchain platforms. Given the financial sector’s previous adoption of blockchain, the infrastructure may already be in place.

“It’s so much trouble already to communicate and move money across international boundaries,” Bailey said. “If we end up using something like a Petrocoin, where your asset is really backed by your oil and gas reserves, you can actually tell somebody, hey, I need a ship of oil but I’m not going to transmit a wire check for $10 million. How much Bitcoin is that worth? Much of this stuff was already being done by the financial institutions. Already, if I file for a mortgage, my bank can check all the other banks that they’re wired into, even if they’re not part of the group.”

Venezuela’s efforts to launch the petro cryptocurrency have met a firestorm of controversy. First announced on 3 December, and issued on 20 February, the petro was supposed to make new forms of international financing available to the country and help back up the value of the bolivar. The price of the petro is based on the Venezuelan’s government’s interpretation of oil and mineral prices.

On 7 March, the country’s National Assembly declared the currency unconstitutional debt issuance and that it would not recognize it. Twelve days later, US President Donald Trump signed an executive order prohibiting transactions in Venezuelan-issued cryptocurrency by anyone in the US. In the executive order, Trump called the issuance an attempt to circumvent US sanctions against the country, which prohibit the purchase of newly issued Venezuelan debt.

Security Concerns

Like with any new digital technology, blockchain comes with its share of security risks. Deloitte outlined some of these risks in a report published last year. In the report, authors Prakash Santhana and Abhishek Biswas said that in addition to exposing companies to risks similar to those associated with current business practices, blockchain technologies introduce other nuances.

Santhana and Biswas broadly classified the risks associated with blockchain platforms into three categories: smart contract risks, standard risks, and value transfer risks. Standard risks are comparable to those associated with current business practices such as the integration of legacy infrastructure with the core infrastructure that makes up blockchain technology, or third-party risks from external vendors. Value transferred refers to the assets, identity, or information exchanged between parties in a blockchain.

Blockchain’s consensus mechanism can help avert the threat of email hacking and invoice interception. McCann said that if a compromised invoice arrives and a transaction is initiated, it would be flagged as invalid as soon as it was broadcast to the network. Since the invoice account details would not match those found in the record, consensus could not be reached and the transaction would not be executed.

Additionally, McCann said cybercriminals would not be able to punish companies that suffer a lapse in diligence after entering a transaction. The account discrepancy would be immediately apparent to everyone on the blockchain and an audit would uncover a fraud attempt. On top of that, he said blockchain’s design limits the influence that a hacked device may have on a network, which will be increasingly valuable as vulnerabilities pop up with the increased adoption of connected devices.

“If a device on the network is compromised, the blockchain record will protect historical information from being changed, and the nature of the decentralized consensus mechanism means that the device cannot successfully execute rogue transactions,” he said.

Bailey concurred on the virtues of blockchain platform design: Instead of having a major server with significant amounts of data stored on it, companies in a blockchain system can have their data saved across multiple servers in a limited fashion, so even if a hacker managed to get into a server it would not have the same compromising effect. He said that companies will always carry some security concern, but the risks involved in implementing a blockchain platform are no different from other everyday transactions.

“Now you can do all your banking on your computer. You take those risks. We buy stuff, we put our credit cards on there to buy something online. We’re all depending on trusting the system to develop security aspects that protect what we’re doing. If you don’t believe in that, that’s fine, you can go another way, but I think the good will far outweigh the bad risk,” Bailey said.