Imagine if you could have seen North America’s shale gas phenomenon coming, years ahead of the competition. What would you have done differently?

Some companies might have avoided spending billions of dollars on liquefied natural gas import facilities in the United States. Some might have acquired acreage before hyperinflation escalated land values. Others would have reallocated capital to better position their companies for the onslaught of natural gas and natural gas liquids. If you had seen it coming, would you have anticipated the global competitive advantage of US domestic industries, from manufacturing to fertilizer to plastics to coal, and the resulting changes to international flows?

Hindsight is 20/20, but there were indicators pointing to a shale gas supply shock. What was missing for most executive teams was a systematic approach for identifying plausible scenarios and defining the leading indicators that would allow them to monitor the market’s evolution toward them.

Most energy companies could benefit from this type of approach, especially with the high level of today’s uncertainty. We have developed a series of plausible scenarios based on our analytical models. To build these scenarios, we capture the dynamics of the energy ecosystem along three major vectors: natural gas supply, crude oil supply, and the uptake of renewables (Fig. 1). Within each, we consider experience curves and the relevant efficiency gains to determine supply curves and possible clearing prices. We then use those prices to calculate intrafuel substitution (such as shale gas for coalbed methane gas) and interfuel substitutions (such as natural gas for coal). We also reasoned that regulatory actions and technology breakthroughs could make renewables competitive and lead to substitution away from fossil fuels. Then we looked at the constraints on infrastructure build-out and we balanced supply and demand by industry sector (power generation, transportation, industrial heating and power, and industrial feedstock). This type of scenario building is a forward-looking process that anticipates disruptive change and can help inform executives for better decision making.

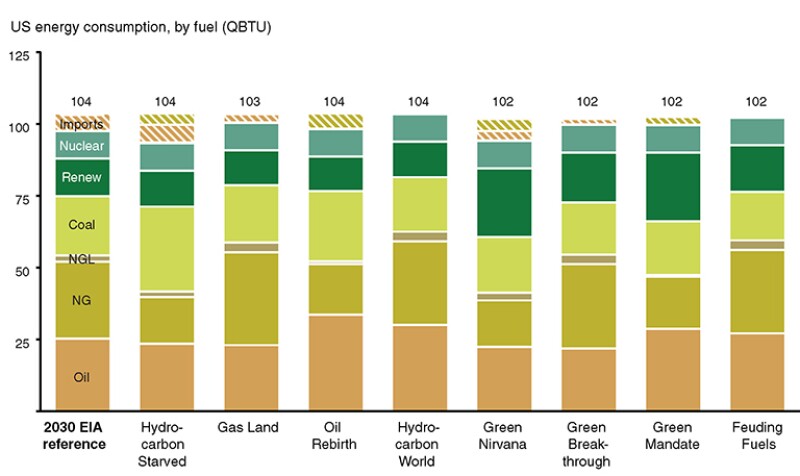

Balancing supply and demand by industry sector (power generation, transportation, industrial heating and power, and industrial feedstock) as the final step reveals material differences in the US energy mix for total consumption (Fig. 2). The models produced some interesting findings:

- High production volumes of shale gas and tight oil could lead to a scenario in which coal and renewables are priced out by cheaper hydrocarbon fuels, and the US stops importing oil and gas from outside North America.

- If renewables continue on their trajectory of cost reduction and experience a breakthrough in storage technology, there may be a shift to a scenario in which a significant percentage of power generation and transportation comes from clean sources.

- If, on the other hand, shale gas and tight oil prove to be less available or harder to extract than anticipated, there could be a coal renaissance and mounting pressure to impose stricter climate legislation in the US.

Despite the material differences, there are some commonalities across scenarios:

- Oil will continue to be the dominant energy source for the US transportation sector through 2030, notwithstanding some very interesting inroads from electricity and natural gas under some scenarios.

- At the other end of the spectrum, the supply mix of industrial feedstock could vary widely depending on interfuel pricing dynamics.

- Coal will continue to be a critical component of the total energy mix, driven by low-cost, coal-fired power generation.

Collectively, these scenarios yield a wide range of production and prices for US oil and gas in 2030:

- Oil production could range between 8 million and 14 million BOPD, with prices between USD 60 and USD 130 per bbl (in 2012 dollars).

- Natural gas production could range from less than 50 Bcf/D to more than 120 Bcf/D (depending on exports), with prices between USD 4 and USD 12 per MMBtu.

- The share of the fuel mix from coal and renewables varies widely, too. Renewables could supply between 10% and 25% of the total energy mix, while coal could supply between 15% and 30% of the mix.

Within these scenarios, there are interesting implications for US energy-intensive industries. For example:

- Natural gas prices in the US could hover near USD 4 for years, creating a strong incentive for many vehicle fleets to switch to natural gas vehicles. As the infrastructure to deliver fuel to natural gas vehicles builds, and as gas producers climb the experience curve, natural gas vehicle ownership is likely to grow.

- Electric vehicles may be cheaper than gasoline cars by 2020.Batteries for electric cars are getting better, solving the problem of limited range. Within 7 years, electric cars may be less expensive to own than gasoline-powered vehicles (assuming today’s oil prices).

- Batteries could unleash solar and wind power—but not yet.There are upper limits on how much of the power mix can come from solar and wind power, because they can generate power only some of the time (in daylight and when the wind blows). Utility-scale storage is the key, but battery technology will need to improve. It will take more than 5 years to develop batteries that can solve this problem at scale.

The global implications are also interesting and wide ranging. In a scenario of abundant tight oil, reduced US imports could push down the global price of oil by returning 5 million to 7 million BOPD to circulation. If, on top of this, Canada, Iraq, and Brazil achieve their aspirational production targets, the global supply could outpace demand by 8 million to 18 million BOPD, an oversupply that could easily trigger a price collapse. It is difficult to estimate the size of a potential price collapse, but previous oversupply situations have cut crude oil prices by 30% to 70%. A price decline of this level would jeopardize the economics of all high-cost sources of crude, including higher-cost sources of tight oil.

The potential for global disruption of natural gas and natural gas liquids (NGL) markets is just as great. Abundant shale gas could displace all other sources of natural gas in the US (aside from associated gas) and leave plenty for export (Fig. 3). These scenarios presume a high level of drilling intensity and infrastructure build-out, but they are plausible—and could have a profound impact on global markets. Specifically, US demand for natural gas could swell to nearly 100 Bcf/D according to our calculations, and total production could still put aside 50 Bcf/D for export.

Each region will find itself at different positions within the scenario cube, depending on how supplies play out. It is also clear that we can describe and track the variables that define the trajectories across the cube. Today, North America has abundant natural gas supply, an emerging supply of tight oil, and growing but still unsubstantial renewables. Western Europe is at a crossroads between the Hydrocarbon Starved and Green Nirvana scenarios: Low supplies of oil and gas are precipitating a coal renaissance, but there is also a strong policy push toward renewables. China is Hydrocarbon Starved and likely to remain so for some time with its growing energy needs—but under a strong policy push to reduce reliance on coal and increase use of natural gas and renewables.

Hundreds of variables help determine the trajectory of any region across the cube, including production and refining issues, regulations, advancements in technology, infrastructure investments, and user economics and preferences. But attempting to consider all of these variables together without a simplifying structure is a complex process that will not necessarily lead executive teams to the right options as quickly as they need them.

Companies can fall into common traps when faced with the kind of uncertainty present in today’s energy industry. Some traps result from being underconfident:

- Treating uncertainty as unknowable

- Focusing only on the things they can control

- Taking a wait-and-see stance

- Doubling down on current advantages

- Failing to take bets on innovation or new ventures

And some traps stem from being overconfident, which is also a common reaction when facing uncertainty:

- Taking bold but unrealistic stances

- Failing to anticipate competition

- Placing big bets that lock in future investment

- Having little or no risk management

- Rigidly adhering to current business models

Strategy in uncertainty requires developing plausible supply and demand scenarios, identifying signposts that determine supply and demand levels as well as prices that drive fuel substitution and import-export markets, and tracking leading indicators to assess the state of these signposts so companies can predict potential disruptions. A major advantage of this approach is that it creates a dynamic strategy. When leadership teams weigh different scenarios rather than betting on one point of view, they are able to see the strategies that will help companies win under different scenarios. This approach also allows teams to develop a strategy with options, such as specific triggers that signal when they need to change direction. Identifying the decisions that teams will need to make in advance of an imminent signpost conditions the organization to become more agile and respond quickly to market realities—a step more effective than taking long periods of time to study the latest disruptive events.

These decisions should align with and inform the organization’s long-term strategic plan and goals. Given how rapidly the situation can change, it is no longer about making one right bet, but about being more accurate more often. The strategy is, increasingly, a dynamic process in which companies continually monitor their options, realign direction, and roll steadily toward their goals. It allows companies to be constantly aware, stay ahead of competitors, and enables them to quickly take advantage of market shifts and opportunities.

Executives in energy and energy-intensive industries are just beginning to come to terms with the likelihood of ongoing supply shocks. Potentially abundant supplies of natural gas, NGLs, and crude oil may continue to outpace the ability of global industry participants to make reasonable bets on future supply levels and pricing. In this world, many assets and projects may require levels of investment that become uneconomic as additional supplies enter the market.

Current estimates do little to reduce the uncertainty surrounding how the energy markets might evolve. Under such uncertainty, it is impossible to predict the future. But companies can build the capabilities to see further into the future by developing scenarios, identifying signposts, and tracking leading indicators. Doing so will help both companies and their investors make sense of the future landscape.

Jorge Leis, SPE, leads Bain & Company’s oil and gas practice in the Americas and is a managing director of the firm’s Houston office. He has more than 20 years of experience advising top business leaders in oilfield services and equipment, exploration and production, refining and marketing, and retail. Before joining Bain, he worked in the chemical processing industry and began his career with Shell Oil. Leis earned a PhD from the Massachusetts Institute of Technology, an MBA from Harvard Business School, and a BS in engineering from Arizona State University.

Mark Gottfredson is a director of Bain & Company’s office in Dallas and a leader in the firm’s performance improvement practice. His experience covers a wide variety of upstream and downstream oil and gas businesses, with specialization in marketing and complexity reduction. He holds an MBA from Harvard Business School, where he was a Baker scholar, and a BA in Japanese from Brigham Young University.