The future of global energy can be reduced to two bits in a recent report: Solar power will represent about half of India’s electric power by 2050, and by then sales of liquid fuel will be higher than they are now.

Those items appeared in the recently released International Energy Outlook from the US Energy Information Administration (EIA) which describes a transition that ends with a mix in which oil and gas continue to play a large role.

While the growth curve for renewables is steep, the report noted that “oil and natural gas production will continue to grow, mainly to support increasing energy consumption in developing Asian countries.”

Adding a lot more renewable power and less coal to the mix will significantly lower the emissions associated with an expected 50% increase in energy demand.

The expected gains, ranging from 5 to 35% depending on the growth rate in those countries, is far from the net-zero emissions goal set to limit global temperature increases and the damaging climate changes associated with that trend.

Different Approaches

The outlook from the Washington, DC-based EIA is a stark contrast to reports from the International Energy Agency (IEA) in Paris that have used modeling to show the extreme changes needed to reach the goal of net-zero emissions by 2050, including sharp, swift, cuts in the exploration and production of hydrocarbons.

The EIA approach looks different because it’s modeling is based only on the policies and data that currently define energy use.

In different ways, the reports reveal the extreme challenges facing negotiators at the COP26 talks looking for ways to eliminate carbon emissions while meeting the energy needs of a world where the population is expected to grow by 2 billion by 2050.

There is something the EIA and IEA have in common—they’re both based in capitals far from the countries whose rapid growth make them the world’s big energy consumers of the future.

“Oil and natural gas production will continue to grow, mainly to support increasing energy consumption in developing Asian countries,” wrote EIA.

India is at the top of the list of countries where a vast, fast-growing population is working to move up the economic ladder. That will require rapid energy growth fueled by rising energy consumption, as in other rising Asian countries such as Indonesia, Vietnam, and China, whose future growth is expected to be slower.

They are outside the group of countries whose membership is used as proxy for the developed economies—the Organization for Economic Cooperation and Development (OECD).

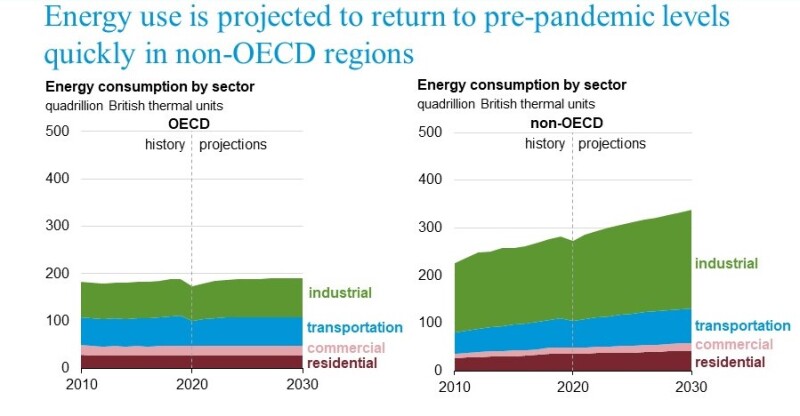

Emissions and energy use are expected to be relatively flat in these affluent countries where heavy industry has long been in decline. Energy consumption in the non-OECD countries is evidence of how it has shifted. These countries are using more than 50% more energy now, and they are expected to use twice as much in 2050.

There is a small dent in the top of the charts showing the demand dip due to COVID-19 last year, which is fading as economic life returns to something resembling normal.

This year is also the first where the demand for transport fuel is greater in non-OECD countries, and that is expected to remain true.

Fuel use for vehicles in the OECD is not expected to return to 2019 levels because of slow growth and regulations designed to maximize fuel economy.

In contrast, energy consumption in non-OECD countries will nearly double from 2020 to 2050, said Angelina LaRose, EIA assistant administrator for energy analysis, during an online briefing presented by the Center for Strategic and International Studies.

Based on those projections, emissions will rise by 35% in non-OECD countries, and only 5% in those in the OECD, based on current policies.

Growth Opportunities

The non-OECD countries are the key consumers for both oil and gas producers and renewable-power developers.

Oil and gas demand will rise to fill the needs of the growing transport and industrial sectors in rapidly growing countries.

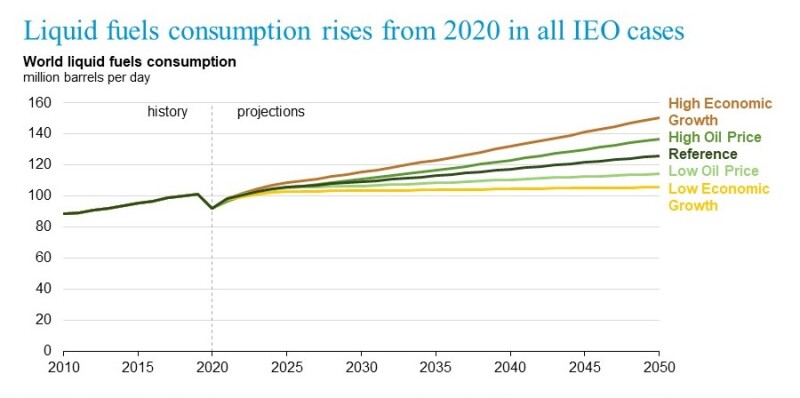

Those economies explain why even the slowest growth projection from the EIA shows greater oil demand. It ranges from a 20% increase in 2050 under its baseline projection to a 50% rise in a fast-growth scenario.

Oil- and gas-rich countries in the Middle East, Russia, US, Australia, and others will benefit.

Since most of the non-OECD countries lack oil and gas resources, “We see growth in the natural gas trade all through this model,” said Mindi Farber de Anda, EIA’s petroleum and natural gas modeling team lead.

Their hunger for more energy will make these the fastest-growth markets for wind, solar, and batteries.

By 2050, 90% of the incremental power in the non-OECD regions will be renewables. The renewables growth there will be twice that of the OECD countries where power demand will grow less, LaRose said.

More wind and solar power will create demand for backup power. In India, the EIA estimated 330 GW of battery backup power will be built to store solar power for delivery when the solar energy generated falls short..

Gas will also be in demand to power generators when renewables are offline.

“These are often the least-cost resource to meet reliability needs and provide energy when solar and wind are not available,” said Stephen Nalley, acting administrator of the EIA.

Steady improvements in solar and wind technology have made them increasingly efficient. But the big advantage of renewables over new fossil-fuel electric-generating plants is that after the plant is built, the source of the energy is free.

For that reason, renewables will be the choice when adding power. But older plants burning coal or gas will remain in operation because the power is needed, and the cost is affordable.

The capital investment in coal and gas was made many years ago, so the cost of the power is based on paying for the fuel to run the plant, said Chris Namovicz, EIA’s electricity, coal, and renewables modeling team lead.

For that reason, coal demand is likely to will remain a significant part of the energy mix through 2050.

Subject to Change

Every prediction above comes with a qualification: It is based on current laws, regulations, and economic trends.

The EIA’s view of the future changes as those factors change. Nalley emphasized these projections, not forecasts. So, as things change, the outlook will as well.

EIA predicts electric vehicles will make up 31% of the cars and light trucks on the road in 2050. That could go up if carmakers deliver on promises to build lower-priced electric cars that grab a larger market share.

Or if government policies push more people to go electric. If this occurs, the EIA will follow when that change looks certain.

“In the US, if Congress passes a law, we will model it. If the president says it off the top of his head at a news conference, not so much,” Namovicz said.