Although oil experienced an extraordinary price increase over the past 4 decades, a turning point has been reached where scarcity, uncertain supply, and high prices will be replaced by abundance, undisturbed availability, and suppressed price levels in the decades to come.

In our new book, The Price of Oil, we conclude that the shale revolution will yield an increased output of oil in the world totaling nearly 20 million B/D by 2035. We also assert that a “conventional oil revolution”—the application of horizontal drilling and hydraulic fracturing to conventional oil formations in the world—will yield a further addition of almost 20 million B/D in the same period. This extra 40 million B/D is nearly twice as much as the global increase in oil production in the 20-year period from 1994 to 2014.

As these new production revolutions develop and expand internationally, they are bound to have a strong price-depressing impact, either by preventing price rises from the levels observed in 2015 (the Brent spot price averaged USD 53/bbl), or by pushing prices back to these levels if an early upward reaction takes place. Our optimistic scenario sees a price of USD 40/bbl by 2035.

Without serious climate policy restrictions, the use of cheaper oil will likely grow and extend its life expectancy throughout the global energy system.

The Carbon Bubble Fallacy

A deep climate policy is one that ensures that CO2 concentrations in the atmosphere do not exceed a doubling from pre-industrial levels throughout the 21st century, believed to be a warming of about 2 degrees Celsius. Such a policy would require global emission cuts of 30% by 2035, and no less than 50% by 2050, compared with 2011 levels. There is little doubt that implementation of climate policy this ambitious implies the end of the recent revolution in oil production. There have also been widespread claims that such a policy would result in massive stranded assets in the fossil fuel industries.

Would sizable proved reserves remaining in the ground due to a deep climate policy constitute a serious problem to the fossil industries? We do not think so, or else, the reserves would never have been created on such a prevalent scale. In the case of oil, the reason proved reserves have been created to last more than 50 years into the future, at present production levels, is that investment in reserve creation is relatively small in relation to total production costs, and therefore worth the companies’ while to assure reasonable peace of mind about future production potential.

The stranded asset problem could raise more serious problems if climate policy resulted in unused production installations whose development has involved heavy investment. Applying the rough and simplified assumption that oil output would be reduced in line with the overall emission cuts referred to earlier of 30% in the coming decades, oil production would be reduced from 89 million B/D in 2014 to around 62 million B/D in 2035. This would be a remarkable change, but even here we believe that serious stranded asset problems are unlikely to occur. Producing oil wells worldwide experience, on average, decline rates of 7% per annum, so stable production requires investments either in reserve growth or in the development of completely new fields. No more than 5 years of ceased investments would then be required to reduce current production capacity to the maximum 2035 level imposed by climate action. In the absence of dramatic and sudden measures imposed without warning, there is little likelihood that installations capable of continued production would be left idle in consequence of interventions to arrest climate change. These considerations raise questions about the realism of stranded asset fears.

Climate Policy Costs

The cost of a rational, deep climate policy, using the most efficient instruments and assuming that economic adjustment to the policy effects will be ideally flexible, has been assessed to amount to perhaps 1–2% of annual global GDP: USD 770–1,540 billion in 2014. Political issues will obviously arise, as these costs will ultimately have to be borne by unwilling taxpayers or energy users.

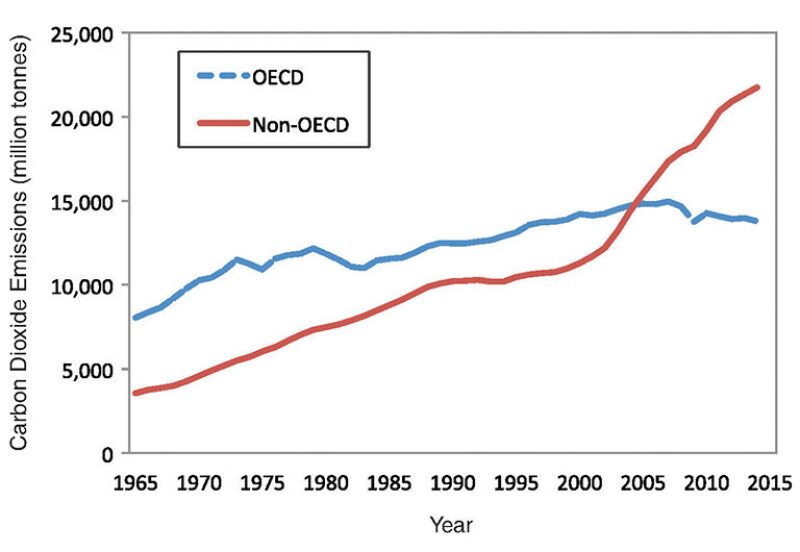

These issues will become much more profound since less developed countries are now the largest emitters (Fig. 1), and virtually all of the energy demand growth in the future will come from these countries. Yet it is reasonable for them to express an unwillingness to go along with a global emissions deal in which everybody is charged equally for each emission unit. Given the industrialized world’s history of intensive oil, coal, and gas use, it is clearly a politically and morally sensitive issue to deny less developed countries the use of fossil fuels to achieve reduced emissions at the expense of similar prosperity. Income transfers from wealthier countries would be required to get poorer countries aboard a global scheme.

Against this background, it may be appropriate to present results showing the order of magnitude of the required dollar flows if the world is to attain the emissions goal referred to earlier, with the non-OECD world’s participation paid for in full by financial transfers. By 2020, the net annual transfers have been assessed at USD 500 billion, of which USD 200 billion would be from the US. By 2050, the required annual transfers would exceed USD 3 trillion, with the US contribution rising to USD 1 trillion. At the Copenhagen climate meeting of 2009, wealthy countries pledged USD 100 billion a year until 2020 in compensation to the rest of the world, a promise renewed at the recent climate summit in Paris. To put these sums into perspective, actual commitments to date amount to about USD 10 billion in total, but even these meager offers are not definitive as they face political resistance in several of the countries making them. Given the relative size of these numbers, it is easy to understand the difficulty in bridging the gulf between the climate rhetoric and the political preparedness to incur the costs.

Climate Policy Prospects and Implications

Practically all energy forecasting organizations predict an expanding fossil fuel future for decades to come, with oil continuing to play a key part in satisfying the world’s energy needs. Moreover, the oil industry’s investment behavior exhibits unbelief in deep climate policy in the foreseeable future. We are inclined to share these views, and contend that the stranded asset phenomenon may come to apply in the main to expensive, subsidized renewables if these attitudes prevail and become instrumental in policy evolution.

Another point to consider in this context is that a vast majority of the world’s oil reserves are in the hands of state-owned enterprises in developing countries. These organizations have goals such as social and economic development, which are likely to be higher priorities than cutting emissions. Moreover, oil consumers in most oil-producing developing countries receive significant public subsidies. These subsidies are politically hard to discontinue. They also encourage domestic usage, and, by implication, the level of production.

Despite the difficulties in predicting what might transpire, history and current behavior point to no more than superficial climate action in the future. The cost of a severe policy is so high, and the confusion and inaction since the signature of the shallow Kyoto protocol so pervasive, that we deem a reversal of past climate policy inactivity to be highly questionable. The noncommittal nature and the extended deferral of action characterizing the just-completed Paris agreement support our view. Hence, we conclude that climate policy is unlikely to hamper the progress of our projected oil revolutions.

Roberto F. Aguilera, SPE, is an adjunct research fellow at Curtin University, Australia, and an associate of Servipetrol Ltd., Canada. He has participated in numerous energy studies, including those by the World Petroleum Council, US National Petroleum Council, and UN Expert Group on Resource Classification. | |

Marian Radetzki is professor of Economics at Luleå University of Technology, Sweden. He has held visiting professorships at Colorado School of Mines and at Pontificia Catholic University of Chile. In the 1970s, he worked as chief economist at the International Copper Cartel, and has undertaken numerous consultancies over the years. Radetzki and Aguilera’s new book, The Price of Oil, is published by Cambridge University Press. |