After its supply and price forecasts in March, the US Energy Information Administration (EIA) was forced to rerun its models by the announcement of historic tariffs on most of the world by the US. The EIA came back with another report on 10 April, forecasting Brent crude will average $68/bbl this year and $61/bbl next year—a drop of $6 and $7, respectively, from the prior forecast.

The EIA is calling for 2025 prices of West Texas Intermediate (WTI) to average $63.88/bbl for the year before dropping to an average of $57.48 next year.

The downward revision reflects the growing uncertainty around global oil demand growth as well the potential for additional supply from OPEC+ in the coming months.

The EIA now predicts that global oil consumption will increase by 900,000 B/D in 2025 and 1 million B/D in 2026. These new estimations are 400,000 B/D and 100,000 B/D less than the initial forecast in March, respectively.

While the reduction has been spurred by a few factors, the biggest has been US President Donald Trump’s sweeping new tariffs.

On 2 April, Trump signed an executive order announcing a minimum 10% tariff on imports from more than 180 countries, including some with tariffs as high as 125%. On 4 April, China retaliated by increasing existing tariffs on US imports to that country by 34%.

But, by 8 April, Trump appeared to back down as market volatility grew, postponing the tariffs for 90 days—except those targeting China. As of 11 April, the US was imposing a 145% tariff on Chinese goods after Beijing responded to the initial round of tariffs with a 125% tariff on all US goods.

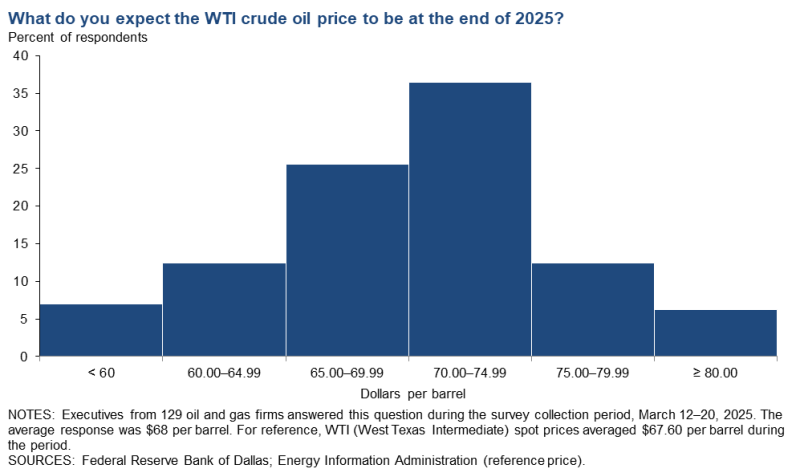

“The administration's chaos is a disaster for the commodity markets. ‘Drill, baby, drill’ is nothing short of a myth and populist rallying cry. Tariff policy is impossible for us to predict and doesn't have a clear goal,” said an unnamed upstream executive in the recent Federal Reserve Bank of Dallas energy survey.

Wide-Ranging Effects

The tariffs could prove to be a major blow to the upstream industry that recently saw some of its highest production numbers.

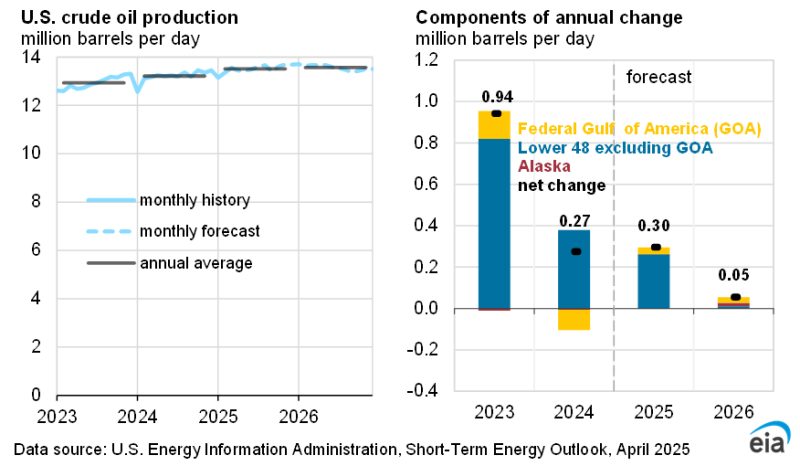

Crude oil production in the US Lower 48 reached a record in November 2024, exceeding an annual average of 11.3 million B/D. Increased production efficiency offset a decrease in the number of active oil rigs, increasing last year’s Lower 48 production by 3%. Overall, production in the US reached 13.2 million B/D in 2024, but the EIA expects production to begin to plateau, reaching 13.5 million B/D in 2025 and 13.6 million B/D in 2026.

Despite record high production, the newly announced tariffs caused the Brent crude oil spot price to fall by 12%. The EIA said it expects recent developments in global trade policy and oil production to contribute to lower global demand growth for petroleum products through 2026. This could spell bad news for producers because typical breakeven prices require between $61/bbl and $62/bbl to remain profitable.

This isn’t the first time Trump has established wide-ranging tariffs. During his last term, he imposed a 25% tariff on steel and a 10% tariff on aluminum imports, which caused US metal production to pick up but slowed down other industries because of higher costs.

Former Pioneer CEO Scott Sheffield appeared on CNBC last week to explain the knock-on effect the tariffs are having on the US oil industry.

“When they put tariffs on … the US steel companies raise their prices. Higher tariffs on imports raise US steel prices, and it costs us more to drill wells,” he said in the interview.

Perhaps one unintended consequence of the new tariffs is the response it is invoking from other nations such as Canada, Brazil, and Kazakhstan, which have committed to more oil production.

Members of OPEC+, including Saudi Arabia—which is set to add 2 million B/D of oil over the next 18 months—are speeding up their previously announced plans for production increases.

Even though EIA’s new report shows that they expect global oil inventories to increase by about 600,000 B/D toward the middle of 2025, market uncertainty could lead to lower economic growth, hindering the growth in demand for petroleum products.

“The effect that new or additional tariffs will have on global economic activity and associated oil demand is still highly uncertain and could weigh heavily on oil prices going forward. The implementation of energy-sector sanctions on Russia and Iran, as well as the wind down of Chevron’s Venezuela oil exports, have increased oil price volatility in the short term while markets and trade patterns adjust. In addition, the pace at which OPEC+ decides to unwind production cuts and the level of adherence to announced production targets continues to evolve,” read the EIA’s Short Term Energy Outlook.

Back and Forth

On 9 April, US crude oil hit a low of $55.12 on, down 23% from the closing price on 2 April when Trump announced his tariff plan. However, WTI made a comeback after Trump suddenly reversed course and announced a 90-day pause on high tariffs for most countries, except China.

The back and forth and political instability wrought by Trump has puzzled and frustrated many within the oil and gas industry. Recently, the president of Diamondback Energy, Kaes Van’t Hof, questioned how these decisions align with Trump’s “drill, baby, drill” mandate and how a global trade war would help shale oil producers.

“This administration better have a plan,” Van’t Hof said in a post on social media network X. The comment was directly aimed at energy secretary and former Liberty CEO Chris Wright. Van’t Hof added that US shale is “the only industry that actually built itself in the US, manufactures in the US, grew jobs in the US and improved the trade deficit (and by proxy GDP) in the US over the last decade … smart move.”

Although the market is experiencing temporary relief from Trump’s decision to pause tariffs, producers in the US are staring down an uncertain future.

“Uncertainty around everything has sharply risen during the past quarter. Planning for new development is extremely difficult right now due to the uncertainty around steel-based products,” said another anonymous respondent to the Dallas Fed Survey.

They continued: “Oil prices feel incredibly unstable, and it's hard to gauge whether prices will be in the $50s per barrel or $70s per barrel. Combined, our ability to plan operations for any meaningful amount of time in the future has been severely diminished.”