Working with clients who are looking to buy upstream oil and gas wells, I almost always hear, “We don’t want stripper wells.” Now that the recent heyday of US unconventional wells is also waning, this often goes along with, “We want conventional production.” With gas prices having been relatively low the past couple of years, it is often, “We want oil-weighted production.”

I am used to unicorn hunts and impossible asks, so I thought this was something reasonably doable. After a long year in a terribly gridlocked acquisitions-and-divestitures (A&D) market, I started thinking about it a little more. Most of the conventional packages that were coming to market had low-rate wells with many inactive wells tagging along. We were evaluating a lot of deals but were seeing several fail due to plugging and abandonment (P&A) liability and the inability of low-rate wells to handle the General and Administrative (G&A) structure of clients.

One client group was competent and ready to deploy capital, and we had gone on the hunt for off-market deals adjacent to their current production. Our team initially found 19 interesting assets, based on size and proximity, and was pleased to find that nine of the 19 had operators who engaged as seriously interested in selling. Our client turned down all nine assets. Every one of the nine assets was cash flow positive (surprisingly in 2020), in the right region, conventional, and the right size. Every one of the nine was turned down because of the large number of inactive and low-rate wells.

In a depressed A&D market with the lowest deal counts in over a decade, having nine assets rejected immediately was frustrating. We decided to screen out assets with low-rate wells and high inactive well counts before making calls and engaging sellers.

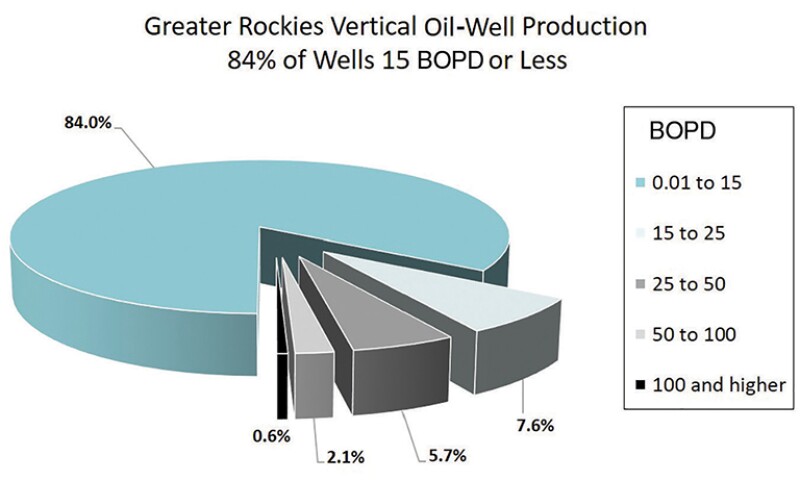

I downloaded data from all the wells in a Rockies state, screened for current production to get a flowing barrel comp range representing the right deal size, looked for oil-weighted properties, took out unconventional wells, added a rate cutoff around 20 BOED per well, and applied a cutoff where reported inactive wells made up less than 50% of the total well count.

Out of about 400 to start with, there were three assets left—only three.

At first, I thought that had to be wrong. I knew that US onshore conventional production probably had a large number of low-rate wells, but it seemed reasonable that there would be several assets that had wells doing 20–30 BOED. Thinking about it more, I sent a text to a colleague: “I bet US onshore conventional production is actually dominated by low-rate wells.”

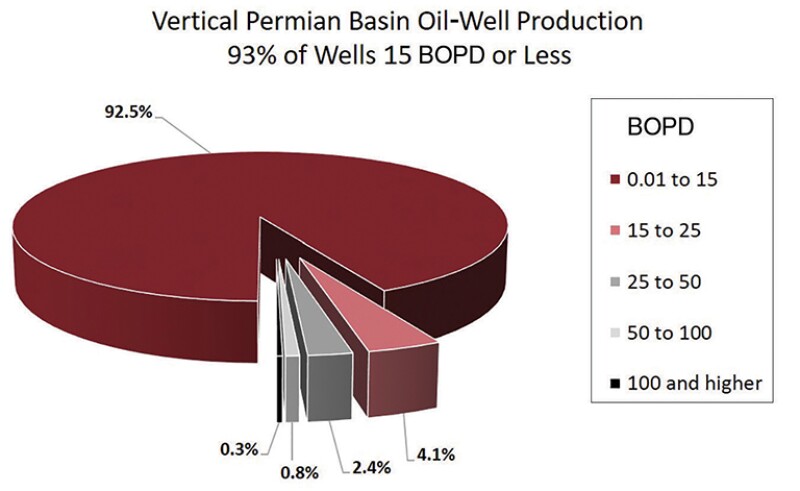

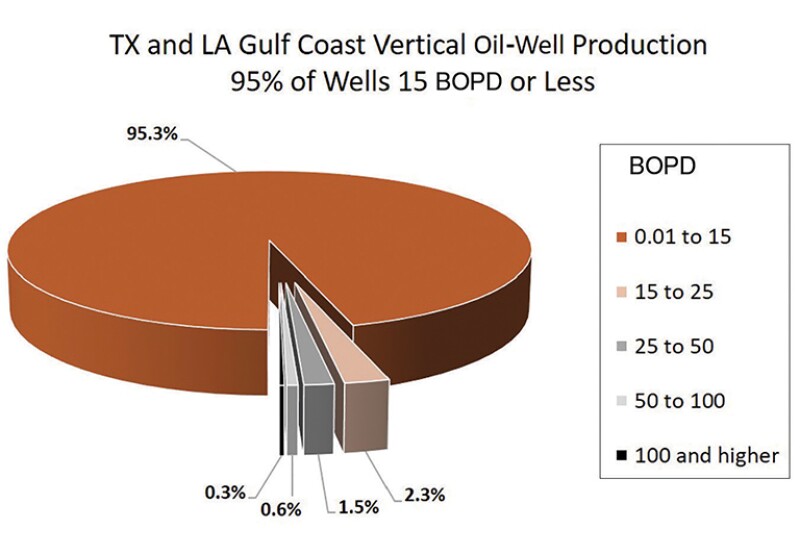

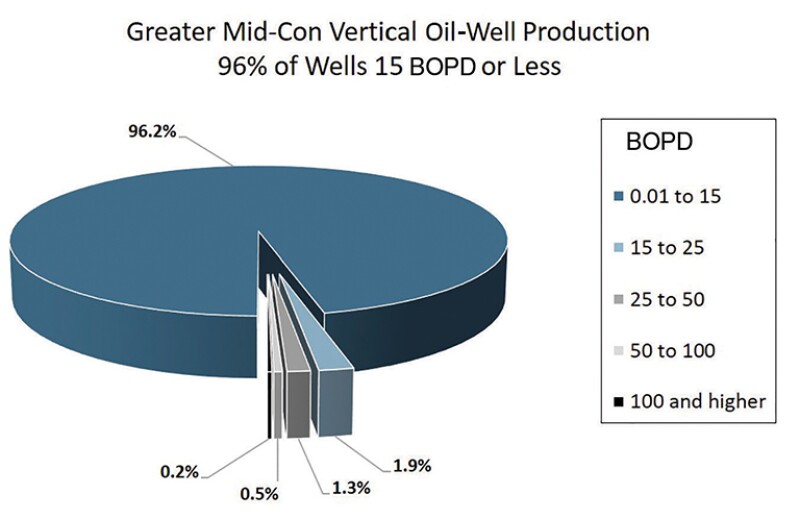

I then pulled data for the Texas Gulf Coast because I had another group looking there. The results were shocking: 97% of the wells were 15 BOPD or below.

All these clients want conventional assets without stripper wells—but they are all stripper wells.

With the analytics and numbers staring me straight in the eyes, I realized that buyers would be working with a very small set of assets if they truly wanted to avoid stripper wells—in the worst A&D market in over a decade (on a deal count basis: Bloombergy, Enverus).

The following analyses of low-rate wells by US region followed from the surprising results seen while looking for client deals.

There are limitations to using public data in any application. For certain applications and for small data sets, public data can be very misleading. However, the larger implications taken in the context of large data sets and knowing the limitations of the data are still telling and paint a stark picture of US conventional production.

Even if large error bands are used, the story is clear: Although they only make up about 10% of total US production (US Energy Information Administration [EIA], Enverus DrillingInfo), the vast majority of onshore US conventional wells are stripper wells.

In the exodus from unconventionals following the Permian bubble that peaked in 2016–2017, buyers are looking for conventional production. To be successful, they are going to have to accept the reality of low-rate wells and the increased operational competency that is needed to make these wells profitable in a relatively low-price environment. They are also going to have to reconsider G&A structures as these wells cannot support many costs above field-level operating expenditures (Opex).

The situation also adds to the ongoing concern over P&A liability as low-rate wells are often one problem away from being shut in. The massive size of the long-term P&A liability across the US has recently gained attention. Add the low-rate wells and this problem gets even larger. That is unless or until oil prices take off again and the economics move hundreds of thousands of wells back to being potentially profitable.

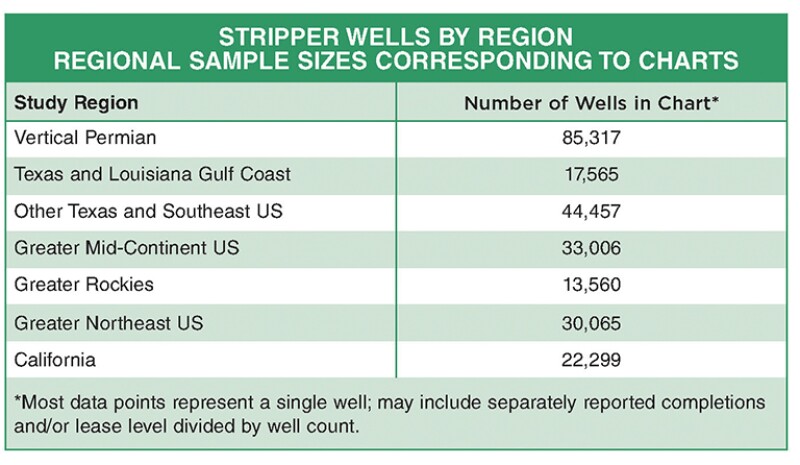

The majority of the data for this analysis came from Enverus DrillingInfo (DI). For Illinois and Indiana, the data came from IHS Markit. On a high level, data were limited to onshore US wells, classified as active by DI or IHS Markit. Vertical wells were used as a proxy for conventional production, although this assumption does cut out some important conventional horizontal plays. For the analysis here, oil wells were looked at independently of gas wells—based on whether DI or IHS Markit identified the well as an oil well per operator records with state agencies (DI’s state classification; IHS Markit’s primary product). For wells classified as oil and gas by DI without differentiation, a cutoff of 75% or greater oil was used; 6:1 BOE basis, past 12 months oil; and BOE. Wells were grouped into seven larger regions as shown in the map.

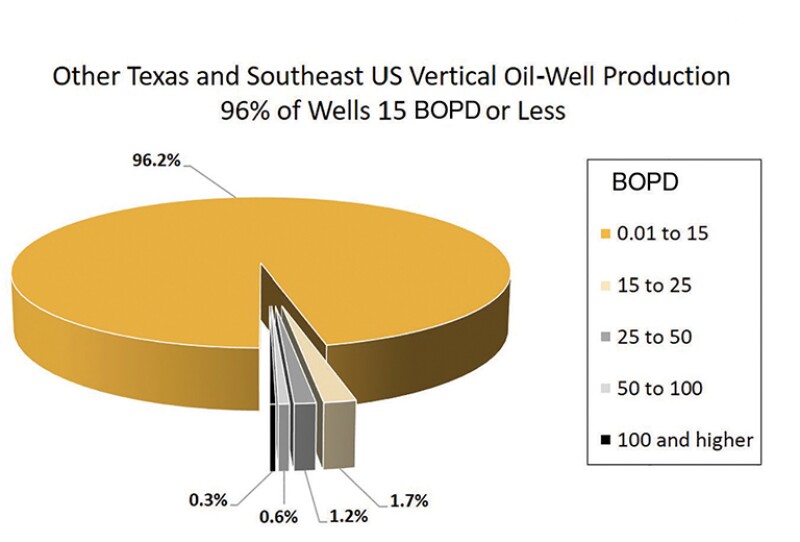

A stripper oil well was an oil well where average daily oil production over the past 12 months was 15 BOPD or less. When active producing wells in all categories (e.g., oil, gas, coalbed methane, and others) were used, and a 6:1 BOED including gas production, the added gas BOE generally moved about 5% of the stripper wells above a 15 BOED cutoff.

The results here are based on the past 12-month daily production; however, latest month production was also looked at, given pricing issues throughout much of 2020, which resulted in meaningful shut-in production for many operators in the middle of the year. (The monthly NYMEX gas price at Henry Hub was under $2/Mcf prior to August 2020 [www.EIA.gov]. Oil contracts often span a past 1–2 month average (last 30–60 day settlements.)

Overall, there was not much difference in the results. Wells with 0 BOPD were excluded from the analysis to avoid skewing the percentages. Wells under 0.01 BOPD were also excluded as this indicates an allocation or reporting issue. Region sample sizes are as shown in the table.

The following note applies to all charts presented.

Enverus DrillingInfo data were used for all states other than Illinois, Indiana, and Kentucky, for which IHS Markit data were used. The region is specified in each chart’s title and as shown in the map. Vertical wells classified as active: latest production in 2020; production of 0 excluded (under 0.01); binned by BOED for past 12 months—greater than lower bound and up and including higher bound; sample sizes as shown in table; public allocated data, typically an individual well basis—may include separately reported completions and/or lease level divided by well count.

Conclusions

The results are surprising: The vast majority of onshore US conventional wells are stripper wells. EIA and the Interstate Oil and Gas Compact Commission estimates from 2016 show about 770,000 marginal wells in the US. High-level calculations indicate a similar number in 2021.

If you consider P&A liability for 770,000 wells, they represent approximately a $20-billion liability, when assuming $25,000 per well with no present value discounting. However, these wells represent a meaningful percentage of US production, and many are operated profitably for years.

Stripper wells have lower production rates, so they need to be carefully managed by people who understand operations to keep production going with low overhead and Opex. For teams such as my clients in the introduction, overhead is often the biggest problem.

Even a 5 BOPD well at 8% decline with end-of-life P&A of $30,000 can carry $2,500/month in operating costs and have a positive PV10 at $40/bbl oil. You can even throw in a workover for $20,000 a couple years out and still have positive PV10.

What you cannot do is add even $800/month in overhead costs (be it corporate G&A, management team fee, COPAS overhead [https://www.copas.org/], contract operating fee, or otherwise) and still be profitable. Stripper wells can carry very little G&A above what is in the field-level Opex. Company and capital structures make stripper wells unprofitable for many teams. Those who can operate without the G&A burden and can keep the wells running without large workover costs have the ability to operate in this meaningful market segment for years to come.

We are in a new environment in the oil and gas industry given many factors including the recent disappointments in unconventional development, lower-for-longer oil prices, long-term depression in gas prices, and severe choking off of new capital. To be successful in the new environment, teams need to be built with efficiency and be comfortable leveraging outsourcing and technology. Teams that only focus on cost cutting are unlikely to survive as this market requires a balance of low costs, efficiency, experience, innovative solutions, and practical approaches focused on profitable oil production and not financial engineering or speculation.