In early February, TotalEnergies revealed its plans to withdraw from the North Platte deepwater development in the US Gulf of Mexico (GOM). Given the historically inviting and economically competitive US offshore when it comes to oil and gas development, word of the French producer’s decision struck an ominous chord.

Things have changed for operators looking to forward multibillion-dollar megaprojects in the GOM. Today, there may be more headwinds than ever before facing future large-scale developments—an unfavorable political regime, competition for investment not only with other oil projects around the world but also with renewable projects, and supply chain woes that have made the waits for long-lead-time items even longer, along with the simple fact that the region has gone several years with very few major discoveries.

The backlog of potential GOM megaprojects is stuck in the single digits, and likely is less than five. Shell has its Leopard find and Blacktip complex. Equinor has Monument. After that, things get gray.

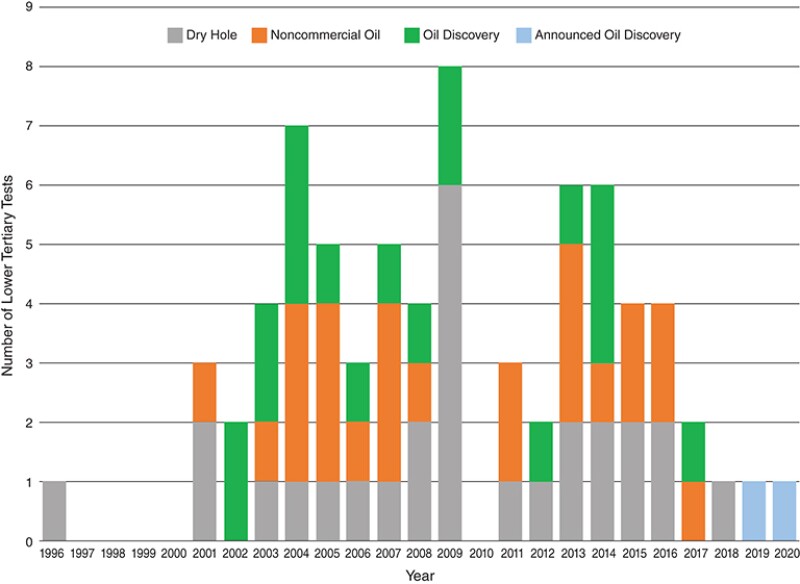

The number of Lower Tertiary wells—where any elephant fields remaining would likely be found—has decreased steadily over the past decade (Fig. 1). According to the Bureau of Ocean Energy Management (BOEM), six Lower Tertiary exploration wells each were drilled in both 2013 and 2014. That number dipped to four in 2015 and 2016. Only one was tallied each year between 2018 and 2020. Of the 25 Lower Tertiary wildcats drilled between 2013 and 2020, BOEM counts seven as oil discoveries, nine as noncommercial, and nine as dry holes. The slide in activity could be related to soft oil prices or it could be that the region, which has been actively explored since around 2000, has matured.

TotalEnergies’ Chief Patrick Pouyanne told investors that it was not US policy that made the company shift gears, but rather the fundamentals of the company’s portfolio. “It’s a purely intrinsic decision linked to the project and linked also to our capital allocation,” he said. “It’s honestly at the limit—at the high limit of the range we gave ourselves. North Platte, because of its size, in fact, we knew it. It’s not a giant field. It’s really on the high side of these metrics. So that’s one point. And second point, we prefer to invest in Sepia and Atapu in Brazil rather than in North Platte.”

North Platte straddles four blocks in the Garden Banks area of the US GOM in about 1300 m of water. The field development plan was based on eight, 20,000-psi subsea wells and two subsea drilling bases connected via two production loops to a newbuild, lightweight floating production unit (FPU). Oil production at plateau level was expected to average 75,000 B/D with associated natural gas.

“TotalEnergies just signed up with Brazil, which has projects more along the lines of what they’re looking for—200,000 B/D-type projects with future upside,” explained Justin Rostant, principal analyst with Wood Mackenzie. “Similarly, in Uganda, they just signed on the Lake Albert (Tilenga) project, which includes multiple fields they’re going to jointly develop—again another 200,000 or 250,000 B/D project. The Uganda project also includes investments in a 60,000 B/D refinery, a 1440-km export pipeline, and potentially a renewable power project. So, truly it’s an integrated megaproject. They also just had a massive discovery in Namibia. Again, a multibillion-barrel discovery that will turn into another megaproject. Those are the kind of projects they’ve been looking at and North Platte just could not compete.”

Headwinds

In addition to portfolio high grading, there are a number of factors applying pressure to the multibillion-dollar development scene in the US offshore. First, even though the Biden administration held a large Gulf of Mexico lease sale last year, it claimed it was obligated to do so by court ruling. Since that time, another judge threw out the results of that sale, and the administration has signaled it does not plan to appeal that decision. The administration said the most recent court action will prompt it to delay decisions on new oil and gas drilling on federal land and other energy-related actions.

“Agencies are experiencing significant delays and wastes of resources as they scramble to rehash economic and environmental analyses prepared in connection with a broad array of government actions,” the Department of Justice wrote in a legal filing in February. “Work surrounding public-facing rules, grants, leases, permits, and other projects has been delayed or stopped altogether so that agencies can assess whether and how they can proceed.”

Second, inflation is also playing a role in decision-making when it comes to field development projects. Raw materials such as steel have seen robust price increases over the past 2 years and are expected to remain elevated compared to historic values.

Additionally, long-lead-time items, which can already take months to receive, have become longer-lead-time items due to negative effects of the coronavirus pandemic.

Finally, the effects of the energy transition are setting in, and operators are changing their mindsets accordingly. With lofty carbon goals set by many countries across the globe, including the US, producers are becoming more conscious of the carbon intensity of their projects. If there is a silver lining for the US Gulf, it is that it has one of the lowest greenhouse-gas emission intensities of any basin in the country.

According to Enverus, the GOM carries a greenhouse-gas-emissions intensity of just over 8. By comparison, the Delaware Basin in west Texas carries an intensity of around 9.5 and the Williston Basin in North Dakota has an intensity greater than 19. That said, the very optics of a large offshore oil project in the age of the energy transition may factor into a company’s investment decisions, even in today’s high-oil-price environment.

While the price per barrel of crude danced around $100 in early March, operators would likely be the first to remind you that when it comes to megaprojects, it is not about the price at the time of sanction, it’s about the price when they turn the taps. For many large-scale projects, that can mean the difference of 5 to 7 years, or more.

“Rystad documented that 2021 had the fewest worldwide oil and gas discoveries in 75 years,” said Erik Milito, president of NOIA (National Ocean Industries Association). “To meet global cumulative demand over the next 30 years, more than 300 billion barrels of oil from undeveloped and undiscovered resources need to be added to currently producing assets globally. The Gulf of Mexico can bridge the gap in energy production.”

He added, “While there may be policy headwinds from Washington, DC, at the moment, policymakers are going to need continued Gulf of Mexico oil and gas production to meet emissions and climate goals. The Gulf of Mexico is a low-carbon basin for oil and gas production, and it is leading the energy transition by helping to build other energy segments, like offshore wind and carbon capture and storage. The Gulf of Mexico can be as enduring as our policymakers allow it to be.”

Meanwhile, in the Gulf of Mexico …

Today, megaproject activity in the US Gulf is as active as it has been in years with three multibilllion projects due to come on line this year—BP’s Mad Dog Phase II (via the Argos floater); Shell’s Vito; and the Murphy-led King’s Quay project, which ties three separate fields (Samurai, Khaleesi, and Mormont) back to one floating host. Current known projects that fit the megaprojects mold are Shell’s Whale (2024), Chevron’s Anchor (2024), and Beacon’s Shenandoah (2024); each has already reached final investment decision (FID) and are under construction.

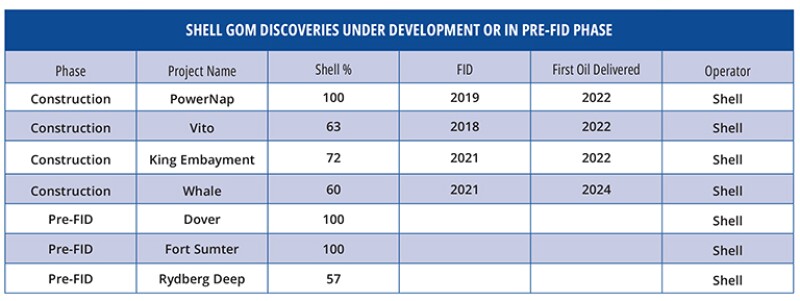

The Blacktip complex and Leopard (Shell) and the Monument find (Equinor) are the likely candidates for the next megaproject (Fig. 2).

“Blacktip, Blacktip North, and our Leopard discoveries are all opportunities to increase production in the Perdido corridor, where Shell’s Great White, Silvertip, and Tobago fields are already producing,” the operator said in an email statement. If the Shell finds end up not requiring a standalone development, infrastructure in the area, namely the Perdido spar, could host that production.

Shell’s pre-FID projects in the deepwater GOM—Dover, Fort Sumter, and Rydberg Deep—are all located in the Mississippi Canyon area south of its Appomattox field, where the operator has a floating production unit installed, and could be developed as future subsea tiebacks to the host.

Monument may yet prove to be a tieback candidate to existing infrastructure. The operator is appraising the discovery now in Walker Ridge block 315 using the Seadrill West Vela.

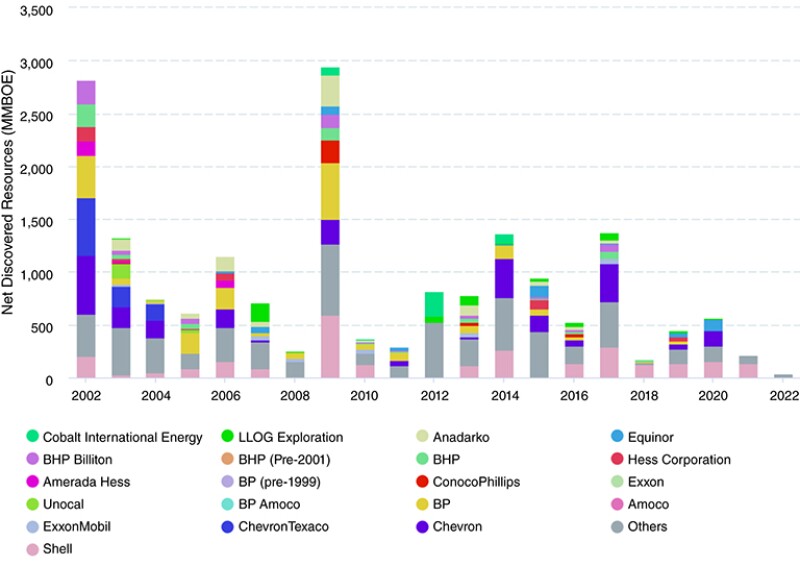

“We have been estimating the size of those discoveries,” said Rostant. “There’s still some uncertainty around it. I do think there might be fewer and fewer opportunities to have new, high‑volume, major projects” (Fig. 3).

Research firm Westwood Global Energy Group expects offshore engineering, production, and construction (EPC) spend in the GOM to be subdued this year, after the TotalEnergies North Platte announcement, which resulted in a $1.2-billion downward revision to forecast offshore EPC award value in 2022. While field partner Equinor has expressed its commitment to developing the project, the operator has not provided a revised development timeline.

“Westwood anticipates $420 million in offshore EPC spend this year, driven by subsea tieback projects such as Chevron’s Ballymore fields, as well as infill activities at Murphy Oil’s Dalmatian and Oxy’s Lucius fields,” said Mark Adeosun, senior analyst offshore for Westwood Global Energy Group. “No floating production systems are expected to be sanctioned in 2022.”

The Gulf of the Future

While oil and gas development will continue in the deep waters of the US Gulf for decades to come, the likely outcome will be highly targeted, infrastructure-led exploration that can be developed quickly via tiebacks to existing facilities.

“Economic trends over the past few years have favored tiebacks and leveraging world-class subsea infrastructure in the US Gulf of Mexico,” explained Milito. “But the Gulf of Mexico is still a productive and prolific basin and companies are still willing to invest significant capital in the region. How companies tackle new projects in the region will be influenced by long-term price factors. The size and scope of projects will respond to long-term energy prices, and given current events on the world stage we are seeing that global energy pricing can change in almost an instant. At the moment, the outlook for future inventories is uncertain.”

Westwood sees the current environment with high commodities prices and the US suspension of Russian oil imports following the invasion of Ukraine as a potential boon to onshore production domestically, with evaluation of possible fast-track development options on offshore discoveries continuing. Over the 2022–2026 period, the firm anticipates just 40 subsea trees to be awarded in the GOM.

“However, potential upsides remain, as the need to remain energy independent could encourage investment in infrastructure-led, fast-track development from undrilled prospects,” said Adeosun.