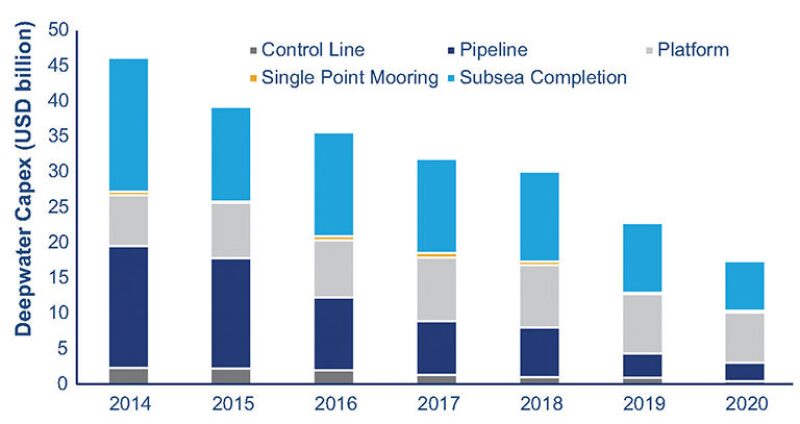

Those waiting for the offshore exploration sector to come back should expect delays. “We are at the bottom of the cycle,” Julie Wilson, research director for global exploration at Wood Mackenzie, said during a presentation at the 2016 Offshore Technology Conference (OTC) that showed deepwater spend declining through 2020, with no upturn in sight.

The problem is that an oil price of USD 50/bbl is still short of the price needed to profitably develop deepwater fields. An oil price of USD 60/bbl is the break-even cost for 70% of the proposed deepwater projects, she said.

The energy information company predicted a growing backlog of postponed projects in the coming years, totaling USD 150 billion by 2020, in a sector where future investment will be affected by whether it can break from its reputation for high costs.

Deepwater producers have made progress in cost cutting. Despite the drop in hydrocarbon prices since 2013, the gap between the value of what has been discovered and the cost of finding and appraising those fields has narrowed.