While the widespread adoption of lower-carbon technologies could create uncertainty and may be perceived as a threat to the global oil and gas industry, it opens new opportunities for investment. According to consulting firm Deloitte, the global oil and gas industry has the opportunity to redeploy as much as $838 billion, or about 20% of cumulative capital expenditures, during the next 10 years. With this opportunity comes a portfolio-management conundrum for companies across the industry: capture the remaining value in hydrocarbons or decide if, when, and to what extent to shift their portfolios in favor of new growth areas including renewables and new-energy ventures.

For the purpose of its recent study into portfolio management in oil and gas, Deloitte defines a portfolio as the products, services, and business units that a company owns or invests in and defines portfolio strategy as deciding a company’s products, services, and business units rather than its overarching business strategy, which includes plans and actions that outline how a company will compete in particular markets.

The oil and gas industry saw a complete reversal of its fortunes in the past decade, with prices going from their peak to subzero, prime blue-chip companies being reduced to “speculative stock,” and the world’s largest initial public offering (Saudi Aramco) taking place alongside mass bankruptcies. Capital expenditures, which peaked at $750 billion in 2014, plummeted to $285 billion in 2020. Finally, overall performance in the sector lagged the larger market for much of this time, indicating to analysts that portfolios often were not fit to address industry headwinds.

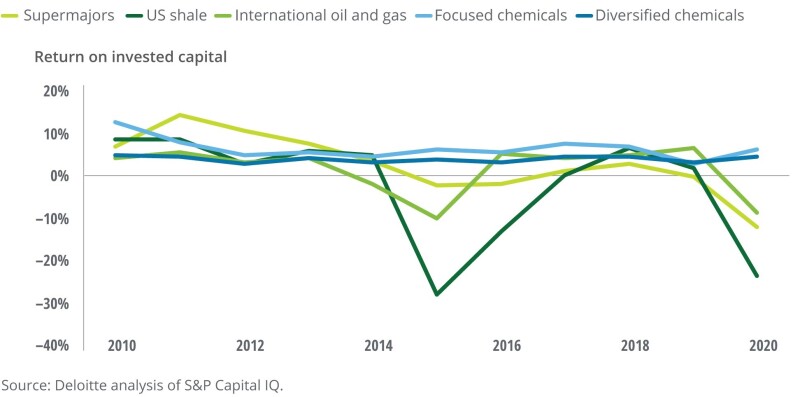

The return on invested capital (ROIC) for oil and gas over the past decade has been volatile, dropping below zero twice for most E&P companies. US shale proved particularly volatile, with deeply negative ROIC in 2015 and 2020. While chemical and specialty-materials companies’ ROICs were more stable, performance was flat to declining for many. Perhaps more important than ROIC in any particular year, said Deloitte, was the fact that performance has been trending downward rather than upward across the entire sector (Fig. 1).

The reality is that the high-growth phase of the oil market has ended, but the coexisting reality is that oil demand likely will not evaporate anytime soon. In fact, some accelerated energy-transition scenarios still project oil demand of at least 87 million B/D by 2030. In the wake of COVID-19 disruptions and an accelerating energy transition, the next decade could prove even more challenging than the past one. The gap between the extent of reliance on hydrocarbons now and a potential burgeoning green economy has created the current hold-or-pivot conundrum for oil and gas companies who understand the imperative to change yet are grappling with how much to invest to best position themselves for growth and in which green technologies to invest.

Capital Redeployment Guidance

To determine how much capital to redeploy, Deloitte suggested that companies start with capital that is not earning the desired return. The company analyzed 286 listed global companies and determined that, in a base-case scenario, these companies could have the opportunity to optimize up to 6% of future oil and gas production that may not generate a 20% return at an average oil price of $55/bbl. This translated to $838 billion, or about 20% of future capital expenditures across the global industry. According to Deloitte, the findings suggest that the opportunity to deploy will increase, rather than decrease, if oil prices stay above prepandemic levels.

Among low-carbon and new-energy solutions, market sentiment is currently strongest for renewable power, with solar and wind attracting the most media attention. Interest is also growing in green hydrogen and carbon capture.

Myths and Realities

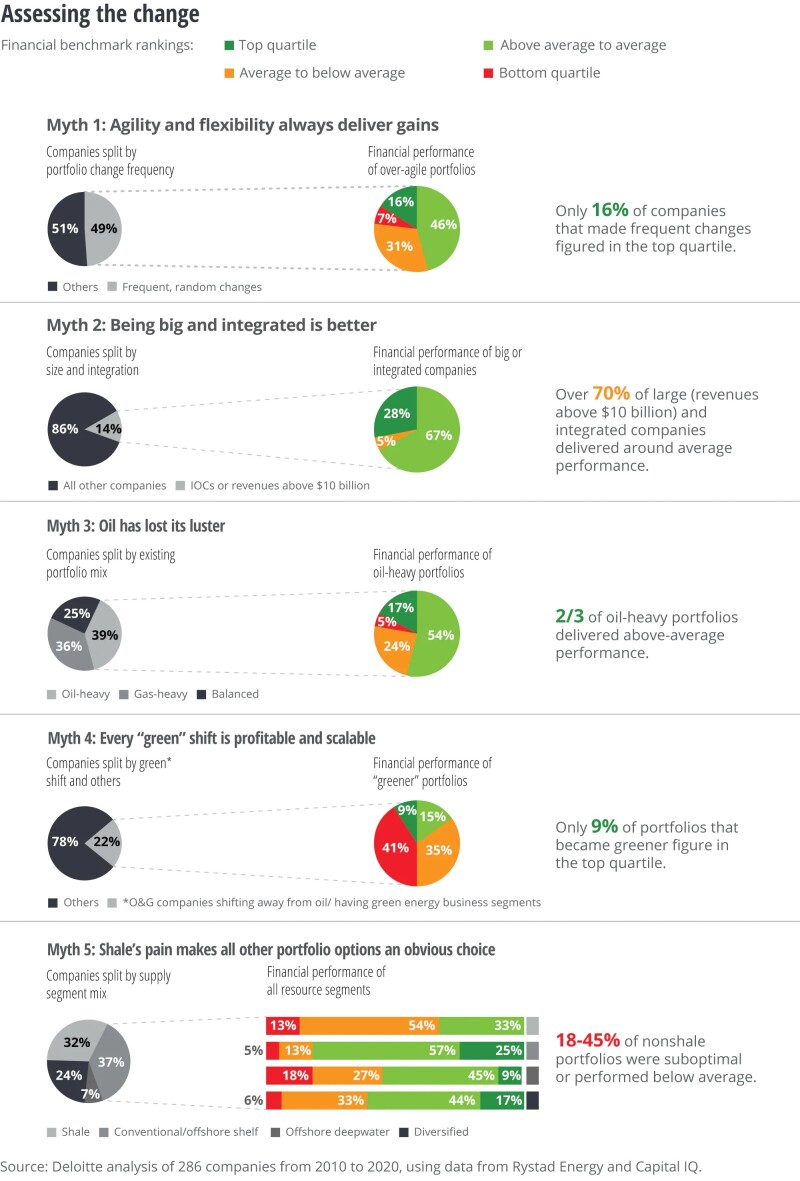

Based on its research, Deloitte has published a new Portfolio Transformation in Oil, Gas, and Chemicals series to provide insight to companies making capital allocation decisions and key considerations into portfolio transformation. The analysis dispels conventional wisdom (myths) about strategic shifts that may have contributed to unsuccessful transitions in the past. The myths and realities are presented graphically in Fig. 2.

Myth 1: Agility and flexibility always deliver gains.

Reality: Consistently maintaining an agile and flexible portfolio (especially one that includes short-cycled shales) can create tremendous impact. But, if portfolio optimization is overdone or done indiscriminately and follows oil price cycles, it can destroy the value and trust of stakeholders. Companies that seemed more strategic and deliberate in their portfolio building delivered much better results.

Myth 2: Being big and integrated guarantees success.

Reality: In some cases, strong balance sheets and integrated reporting structures could be hiding inefficiencies in portfolios of large companies. Of the publicly listed non-national oil companies (non-NOCs) that either have revenues exceeding $10 billion or are integrated, a majority underperformed over the past 10 years. Only 28% delivered top-quartile performance, and only three ranked in the top 10 performers, despite having some of the strongest balance sheets. Many NOCs have outperformed their publicly traded counterparts because of their low-cost resource base, high-pressure fields, and access to markets.

Myth 3: Oil has lost its luster.

Reality: Two-thirds of oil-heavy portfolios have delivered above-average performance. Even as oil reaches peak demand, it is expected to slowly plateau over the coming decades and to remain above 87 million B/D until the end of this decade. Just to replace the annual consumption and offset natural field declines, the industry would need to invest more than $525 billion annually in oil and gas projects.

Myth 4: Every green shift is profitable and scalable.

Reality: Of portfolios that have become greener, only 9% delivered top-quartile financial performance, underscoring the importance of a strategic, purpose-driven approach to portfolio transformation. In cases where oil and gas companies have made investments in renewables or clean tech that are complementary to their core business, those companies have seen benefits. Although the green shift is inevitable in the medium-to-long term, striking a right balance between hydrocarbons and green energy can be essential in the near term.

Myth 5: Shale’s pain makes onshore conventional plays an obvious choice.

Reality: Between 18 and 45% of nonshale portfolios analyzed delivered below-average performance. Where a company drills appears less important than how. Operational excellence is key to value differentiation.

For Further Reading

Portfolio Optimization in Oil, Gas, and Chemicals