Russia has shown a remarkable ability to add oil and gas production in the face of daunting obstacles. It has aggressively expanded in Asia, by rapidly adding production in east Siberia, as it builds pipelines to China and a liquefied natural gas (LNG) facility deep in the Arctic.

A panel of eight leaders from the Russian oil and gas business recently offered an impressive growth story in the face of international trade sanctions and oil prices that sunk into the USD‑30/bbl range year ago.

“I have an impression there is a kind of positive mood,” said Alexander Novak, Minister of Energy of the Russian Federation, at a panel session at the IHS Markit CERAWeek conference in Houston. “Prices are becoming stable, more predictable,” he said, but added “there is uncertainty about what comes next.”

As Novak was talking about how the oil-and-gas-driven Russian economy is growing again after a 2-year downturn, oil markets remain weak due to rising US unconventional oil production and lingering high inventories.

The upbeat feeling mentioned by Novak was largely the product of a deal between OPEC and major producers, particularly Russia, to reduce their output.

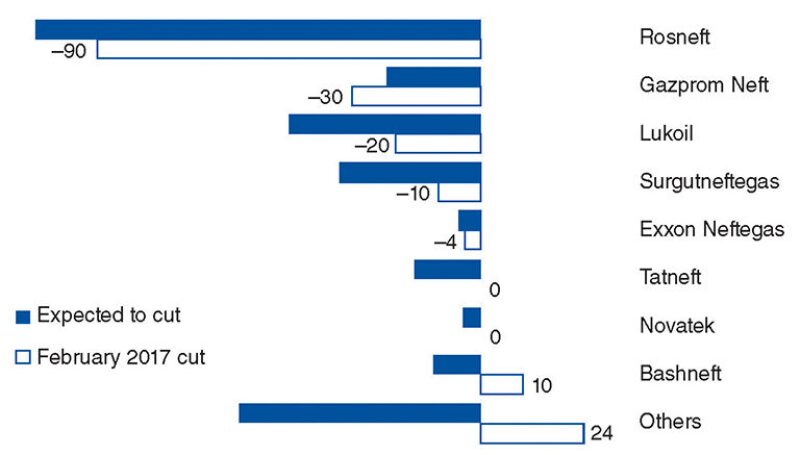

As of late March, Russia was less than halfway to meeting its pledge to cut output according to a report by Rystad Energy. That study showed that while the largest Russian producers had made cuts equal to about 50% of the 300,000 B/D commitment, those reductions were offset by rising production from independents, particularly by the biggest one in this group, Irkutsk Oil.

“We do not currently see any evidence of Irkutsk Oil or other smaller producers planning to comply with the reduction program targeted, and thus there exists an upside risk to the overall agreement,” said Veronika Akulinitseva, an analyst for Rystad Energy.

Russia remains the biggest supplier of gas to Europe, but an oversupply of gas there means it is scrambling to retain customers demanding lower prices. That is a big change from earlier this decade when gas supplies were tight, and Russia was able to demand top prices.

“Those days are gone now” as the supply gap changed to a supply glut, said Maxim Nechaev, director of consulting in Russia for IHS Markit.

To grow, Russia has turned to Asia. To reach those markets, it is building pipelines, expanding energy export facilities at Pacific ports, and constructing gas liquefaction facilities as part of a program to push its share of the global LNG market from 5% to 15%.

Export routes run in “two directions and none of them are more important than the other,” said Mikhail Margelov, vice president of Transneft, which controls 90% of the pipeline traffic in Russia.

Asia offers demand growth that Europe does not, but Russia is competing for a share of the oil market with Saudi Arabia and is competing in the gas market with earlier international pipelines and Australian LNG producers. “LNG is ample and can freely fill any supply gap anywhere in the world,” Nechaev said.

Growth Requirement

One sign of the times in Russia was the fact that Irkutsk Oil was responsible for one-third of the production growth in Russia last year, said Matthew Sagers, managing director in energy for IHS Markit, which organizes CERAWeek. It did that by running 32 drilling rigs in eastern Siberia, even during the worst of the oil slump.

The company was born at the start of the century and has been growing about 35% a year, with funding for its drilling program coming from investors in Japan, Europe, and the US, said Nikolay Buynov, chairman and president of Irkutsk. While Russia’s independent producers get little attention, Buynov noted that investor-owned Russian oil companies are “a normal part of the industry.”

Independents are getting some notice now because, as a group, they added 24,000 B/D of production in February. The Rystad report said that if Russia honors its promise to OPEC, the country’s top producers may have to cut deeper.

“It could be more challenging for smaller operators to technically reduce production, and also the impact from such a reduction could hurt them more than such producers as Rosneft, for example,” Akulinitseva said.

Reductions by Irkutsk would slow development of Russia’s production frontier in eastern Siberia, which offers both huge potential and proximity to China. Rystad estimates that the company added 30,000 B/D of production there last year and could add up to 20,000 B/D this year, with a breakeven price around USD 30/bbl.

Based on the oil in the ground in Russia’s east, there is big room for growth.

Last year, the Russian geology and geophysics data company Rosgeologia acquired a record amount of seismic data in eastern Siberia and the Russian Far East to meet the demand for explorers in a region that is “not covered by intense development,” said Roman Panov, director of the company, known as RosGeo.

Greater Recovery

Russian producers have had to find ways to add production to offset declines in aging fields in east Siberia. Getting what is left in those thick formations has required adapting the tools used to produce oil from ultratight unconventional formations for economical completions in not-so-tight rock.

Russian production from “hard to recover” reservoirs is now 1.3 million B/D and is expected to rise to 2 million B/D, said Novak.

Since 2010, there has been a rapid rise in the use of horizontal drilling and multistage fracturing to stimulate tight Russian reservoirs with an average permeability of around 0.1 millidarcy or more, said Sergey Kudryashov, general director of Zarubezhneft, a state-owned oil company, with operations outside of Russia.

When faced with unexpectedly complex rock, Russian firm Gazprom resorted to drilling horizontal wells in a fishbone pattern, with branches of the lateral like the skeleton of a fish, to effectively produce it.

“We are not pioneers” in the method, said Vadim Yakovlev, deputy chairman of the management board, first deputy, chief executive officer, Upstream Gazprom. “But what is special is how quickly we can go from testing to production.”

Marketing Frontiers

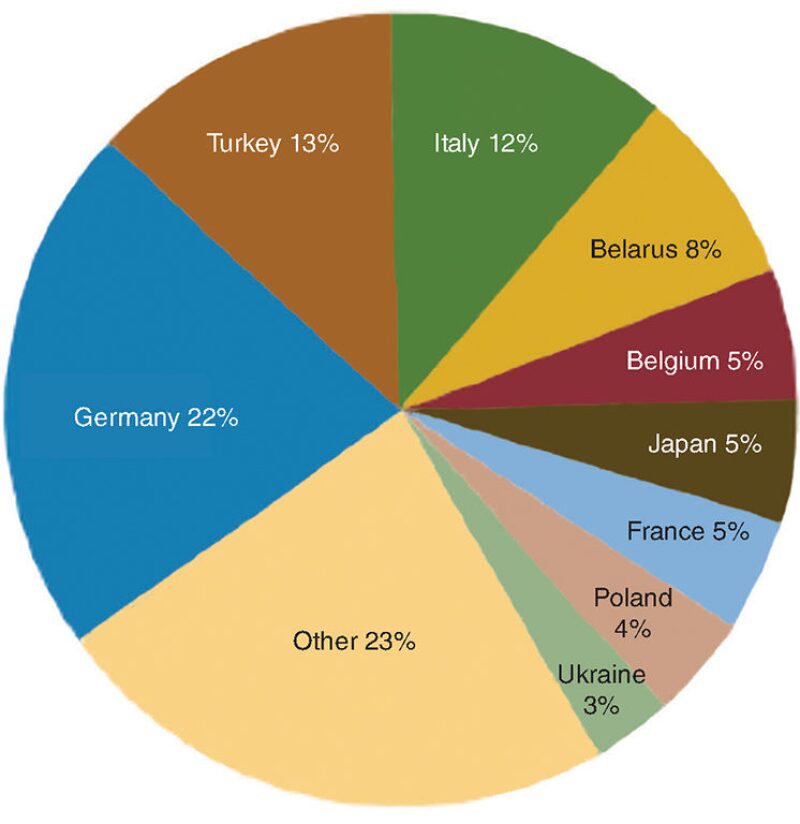

Russia remains the biggest single gas supplier to Europe, and it is working to significantly expand its pipeline delivery network.

“Russia has more than enough gas supply to fill any gas supply gap in Europe,” said Reinhard Ontyd, chief commercial officer for Nord Stream 2. Next year, a venture, whose western European partners include Shell, hopes to get the approvals needed to begin building an offshore pipeline paralleling the route of the Nord Steam 1 line, which it plans to complete by 2020.

The problem for Russia is that Europe is a slow- to no-growth market with ample supplies. More imported gas will be needed as the output declines from aging fields in the North Sea and the Netherlands, according to a CERAWeek conference panel on the European gas market.

Gas sales would also go up if Germany decides to switch from domestically produced coal to imported gas for electricity generation. While that would significantly reduce emissions, Germany has no plans to do so.

Another problem for Russia has been its involvement in the Ukrainian conflict and the annexation of Crimea, which led the European Union to impose international economic sanctions and a push there to develop alternative gas sources.

“Especially after the conflict in Ukraine, Gazprom gas sales in many countries have gone down, and the overall sentiment in the market has been that if there were alternative sources of gas imports, more countries would switch to other suppliers,” Akulinitseva said.

Russia is expected to remain the biggest gas supplier for Europe, with a market share ranging from 25% to 35%. But utilities there are seeking other options.

“We must promote secure supply at the European level going three directions,” said Elio Ruggeri, senior vice president for gas supply origination and infrastructures for Edison SpA, which is working on multiple projects.

An east-west line will transport gas from Russia’s planned TurkStream pipeline in Turkey to Italy, because Russia “will be the main actor in the European market for a long time to come.”

Another will go south and east to major gas discoveries in the eastern Mediterranean, including the Leviathan field off Israel, to Europe.

And a third will build regasification facilities to accommodate LNG tankers from around the world.

Liquid Pricing

This world of gas supply options is requiring Russia’s gas giant, Gazprom, to become a lot more focused on customer relations. European buyers are no longer willing to sign contracts with a gas cost formula based on the price of oil, when they can buy gas cheaper on European spot markets.

“Gazprom announced that it will exercise a more flexible price policy toward European customers by increasing, and at times even switching fully to, spot-based pricing,” Nechaev said, adding, “This is supposed to stop erosion of Gazprom market share in Europe and increase customers’ loyalty.”

Ontyd described how building Nord Stream 2 will “enable competition.” That could prove to be true. When the gas from a growing European pipeline network is added to ready access to shiploads of LNG from the US and Australia, all that supply creates business opportunities.

With surpluses in Europe and Japan, “traditional buyers will become sellers in the next few years” increasing the amount of liquidity and trading in the market, said Jonathan Westby, co-managing director for energy marketing and trading at Centrica in the UK. “The ability of Europe to provide swing capacity” will increase its role in the global gas trade, he said.

Growth in gas liquefaction capacity by 2020 will put about “200 cargoes on the water at any time,” said Charif Souki, chairman of Tellurian Investments, a US LNG company he cofounded after being pushed out of Cheniere Energy, which pioneered the US LNG export business.

He describes how this fleet of LNG tanker ships will dampen price spikes by delivering gas in places when supplies are short, such as during a record cold snap in Europe.

But the future of his company, and anyone else developing a gas delivery project, still depends on long-term contracts using a price formula that will generate the cash flow needed to convince bankers to lend billions of dollars, and be attractive to consumers.

Oil-pegged contracts have worked in that role, but increasingly gas prices are not moving in tandem with oil prices. “Gas-on-gas competition will lead to a decoupling on a global scale to the oil mark,” Westby said.

If Europe becomes a global hub for the gas trade, a likely candidate to replace oil in the price formula is the Title Transfer Facility (TTF). That is the price paid for gas at a virtual trading point used by Dutch traders. It is actively traded like its better known counterpart, the Henry Hub price, which is the US benchmark used for many contracts.

Any change will take time. Russia’s gas contracts still include oil in the formula, said Sindre Knutsson, an oil and gas market analyst for Rystad, adding, “Even if Gazprom has been flexible in changing their contracts structure, they do not seem to turn fully to hub-indexed contracts.”

But Russia’s sprawling energy sector is also creating LNG competition in the Yamal project in the Arctic, where three liquefaction trains are 90% complete and will be coming on line in 2018 and 2019, said Denis G. Khramov, deputy chairman of the management board of Novatek, the gas producer leading the project.

Despite icing conditions and remoteness from LNG markets, he said the supplies from these projects will be economically viable and competitive.