mergers and acquisitions

-

The latest acquisition strengthens Cenovus Energy’s position as Canada’s largest SAGD producer.

The latest acquisition strengthens Cenovus Energy’s position as Canada’s largest SAGD producer. -

The deal follows Blackstone’s recent moves in gas-fired power and a pipeline venture with top US gas producer.

-

The deal marries Baker’s core competencies in rotating equipment, flow control and digital technology with Chart’s heat transfer, air- and gas- handling, and process technologies expertise.

-

The latest merger and acquisition report from Enverus Intelligence Research shows deal value fell 21% quarter over quarter.

-

Chevron now holds a 30% stake in a prolific offshore Guyana development, where oil production is expected to ramp up over the next few years.

-

The traditionally Oklahoma-centric producer adds new acreage in west Texas and New Mexico through a pair of purchases.

-

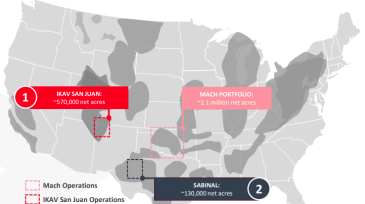

The supermajor follows other oil companies including ExxonMobil, Equinor, and Occidental Petroleum in the hunt to bolster US supplies of lithium.

-

The tentative offer has received unanimous support from the board of Australia’s second-largest oil and gas producer.

-

Viper Energy is acquiring Sitio Royalties Corp. and its more than 25,000 net acres of royalty interests across major US shale plays.

-

The second-largest gas producer in the US is aiming to pump an average of 6.3 Bcfe/D this year.