Produced water from oil and gas wells in onshore US plays may fall by nearly 20 billion bbl annually by the end of 2022, according to an IHS Markit analysis. The projected decline, which reflects a total water management market value of $28 billion, is down by 4% from 2019 volumes.

Paola Perez Peña, principal research analyst at IHS Markit, said the company expects the total water management market size in the US to drop about 20% below previous estimates. The decline in drilling and completion (D&C) activity in the next 2 years will also significantly reduce fracturing water volumes, while the decline in produced water volumes will be less severe.

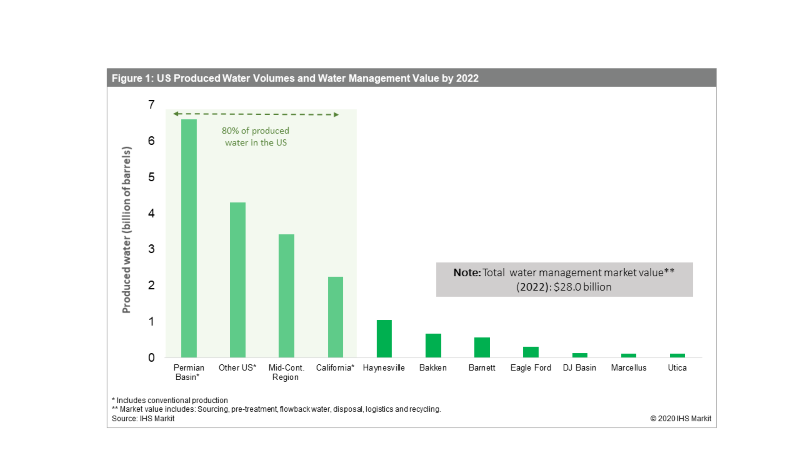

IHS Markit’s projection for year-end 2020 is that D&C requirements for water in US shale plays drops by 46% from 2019 to nearly 2.5 billion bbl. Produced water volumes from oil and gas wells in onshore US plays are expected to reach nearly 21 billion bbl, a 1% increase over 2019 levels and more than eight times the amount of water expected to be used for D&C in 2020.

By 2022, 41% of the produced water from oil and gas operations will be reinjected, 47% will be disposed of using saltwater disposal (SWD) wells, and 13% will be recycled for reuse in fracturing operations.

To estimate the future market values for oilfield water, IHS Markit considered the complete value chain of the market—water sourcing, treatment, and disposal, with logistics services throughout the chain. Of those segments, water logistics and disposal are the largest sectors and are expected to drive 91% of the water market value in 2022.

The data analytics group expects a decrease in water infrastructure investment by exploration and production companies in 2020 and beyond in response to falling oil prices. A significant decrease in D&C activity will represent a more than 60% drop in demand for sourcing, pretreatment, and flowback services combined.

As a result, the group said third-party water disposal companies have formed a new type of water midstream business model that is being adopted in the industry, especially in the Permian Basin. This new model eliminates the need for infrastructure investment from operators.

With the need for cost containment and the fragmented nature of water production, IHS Markit expects to see more collaboration and partnerships among operators. In addition, operations to handle oilfield water will be more localized and will shift toward multioperator infrastructure systems.