Discovered in 2011 offshore the Malaysian state of Sarawak, the Kasawari sour gas field is today a symbol of Southeast Asia’s energy challenge.

Petronas is eyeing next year for first gas. By 2025 it hopes to see 900 MMscf/D flowing from the field to its sprawling Bintulu LNG export facility on the Sarawak coast.

But what makes the field a regional and industry bellwether is not its natural gas.

When peak output is reached, Petronas plans to stop venting and start capturing between 3.7 and 4 million mtpa of the CO2 that will be produced from the project’s wells over the next 2 decades.

That’s more than 8% of the greenhouse gas emissions Petronas reported for all of 2020. And in more upstream-friendly terms, the injection target at Kasawari is roughly equal to 77 Bcf of gas each year.

Keeping that huge volume of CO2 from ever seeing the light of day will require a dedicated platform that Petronas is in the midst of designing. It will also need a 138-km-long pipeline to send CO2 to a depleted field for permanent storage.

And of particular note, this second phase of Kasawari will not just be the Malaysian national oil company’s first such attempt at megascale carbon capture and storage (CCS).

With more than twice the planned injection rate of Norway’s Northern Lights CCS that is set to begin in 2024, Kasawari will become the world’s largest offshore CCS project just a year later.

The scale of Kasawari, found at a water depth of about 108 m (350 ft), is a result of its ranking as one of the most CO2-laden gas fields planned for development globally. When wells are flowing, it’s expected that up to 40% of what will come out will be CO2.

But since Petronas has also signed on to become a net-zero emitter by 2050, venting the field’s waste gas won’t be a viable option for long.

The sheer scope of the project, and that it is a maiden voyage of sorts for Petronas, has drawn attention to the impact CCS will have on upstream project development costs in Southeast Asia.

New research from Rystad Energy suggests that the capital inputs required to add CCS to Kasawari will hike the project’s breakeven gas prices from roughly $3.50/Mcf to more than $5.00/Mcf.

The energy consultancy sees a similar case especially for other offshore sour gas projects where CCS will likely be needed to abate production-driven emissions.

“Most of these projects are certainly in the study phase still,” said Prateek Pandey, vice president of analysis at Rystad.

“But the bigger challenge—more than the technology—is likely to be the economics of these projects and how operators justify the additional development cost with the implementation of CCUS [carbon capture, utilization, and storage] and CCS.”

Pandey’s remarks came while presenting the paper, OTC 31335, which he authored, at the recent Offshore Technology Conference (OTC) Asia in Kuala Lumpur.

More than 8,000 people took part in the technical gathering that was also Malaysia’s first in-person conference since the onset of COVID-19 began 2 years ago.

Talk in Malaysia’s capital city about rising energy prices along with Southeast Asia’s new CCS ambitions was in no short supply. Where a supply concern may be cropping up is the subject of Rystad’s paper.

It suggests that just under half of the future hydrocarbon resources from Malaysia, Indonesia, and Vietnam are at risk of facing delays and significant cost overruns. This is based on projects scheduled for a final investment decision by 2025 and amounts to around 4.5 billion BOE.

The problem facing project planners stems from these being sour gas resources. Though some of the reservoirs identified as at risk contain toxic and flammable hydrogen sulfide, the bigger concern from a cost perspective is their CO2 concentrations.

On the low end are fields with 15% CO2, and then there are fields like Kasawari with up to 40%.

Petronas has previously acknowledged that the CCS phase at Kasawari will increase its original spending plans, but it still expects to deliver gas economically.

Given today’s market, that may not be so hard to imagine. One might argue that even a 50% jump in development costs is tolerable given that Asian LNG spot prices as of late have been trading at record levels of above $60/Mcf.

Then again, predicting the long-term price picture can be a fool’s errand.

Pandey noted that “there is obviously high confidence in overcoming the challenges by the operators, because a lot is at stake.” His comment was a nod to the outsized role that sour gas is set to play in Southeast Asia’s energy supply mix.

Rystad’s paper was one of several presented at the conference that underscored how announcing a CCS project is the easy part. The herculean task of executing just one and then scaling up from there will require many billions of dollars, unforeseen setbacks, and untold amounts of engineering work.

Looking to become a regional leader in CCS, Petronas shared details about its early planning efforts in a modeling study on the leakage potential of a depleted reservoir off the coast of Sarawak.

The work sheds new light on what might happen if plugged and abandoned (P&A) wells become vectors for fugitive CO2. Ultimately, it was concluded that environmental impacts may be minimal and localized if leaks are small enough.

Separate work from Australia also focused on the integrity issues facing CCS assets. A paper led by authors from Schlumberger explains how traditional cement can degrade when exposed to high concentrations of CO2. That’s why in Australia’s first offshore CO2 injection well a special CO2-resistant cement was used for the P&A job.

On the midstream piece, Petronas also presented an outline of how it’s using advanced software to simulate how it will move captured CO2 and natural gas through a busy network of existing pipelines.

Meanwhile, Technip Energies is offering way to avoid pipeline traffic with a floating CO2 facility it calls the C-Hub. Included in the engineering firm’s idea is to build a fleet of purpose-built tankers that would load up with liquidized CO2 at industrial ports and deliver it to the hub for continuous injections.

Spend Today, Earn Tomorrow

The technology developments listed above, and others featured during the 4-day conference in Kuala Lumpur, reflect that CCS is a budding industry—not quite a booming one.

This is true in part because two key business enablers—a mature carbon credit market and carbon taxes—are not a major force today in most of the world.

However, many at OTC Asia acknowledged that the writing is on the wall, which has Southeast Asian operators trying to get out ahead of the matter today.

As Pandey framed the situation: “At some point, the price of not doing [CCS] can potentially be even worse as both the Indonesia and Malaysian governments are discussing a roadmap for implementation of carbon taxes in the near future.”

While all the fiscal pieces have yet to fall into place in Malaysia, Petronas is following the path that many international oil companies have taken in recent years. It wants to get out in front now so it can monetize later.

Speaking to OTC Asia conferencegoers, Petronas CEO Tengku Muhammad Taufik highlighted that more on this front is to come after the company launched its first carbon management business in March.

“This new unit will focus on accelerating our decarbonization efforts across the entire integrated value chain by managing a carbon storage portfolio for emissions produced not only by our operations, but potentially also to establish a regional storage hub for carbon emissions as a new revenue generator,” he said.

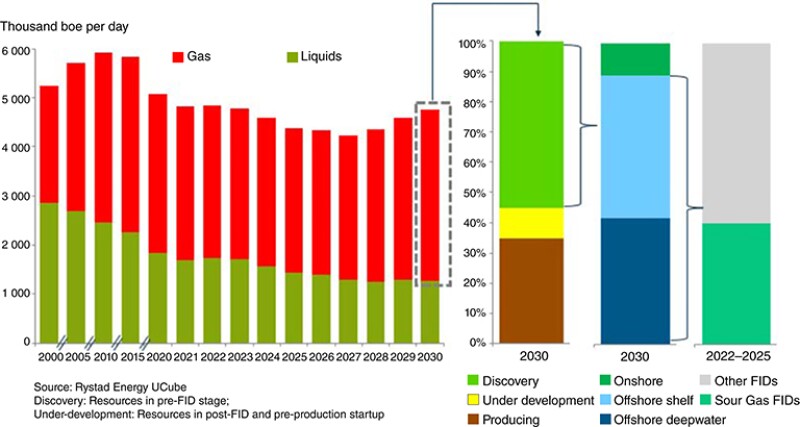

Fueling the Future With Sour Gas

In simple terms, Southeast Asia’s short-term energy outlook is highly dependent on sour gas—also known to the industry as contaminated gas—because it represents about half of what’s left to produce. The big downside is that sour gas is notoriously costly to process, even without considering the cost of CCS.

But as pandemic restrictions loosen further across the 11-nation region that is home to around 650 million people, several countries are expecting to witness annual economic growth rates of 5% or more.

To fuel the engines of that growth, oil and gas companies in the region—70% of which are led by NOCs—will spend $25 billion on greenfield projects over the next 3 years. This compares to just $2 billion spent over the previous 5-year period, according to numbers from Rystad.

The potential wave of capital outlay is driven in no small part by mandates across Asia to halt the construction of new coal-fired power plants and instead promote the conversion to or building of lower-emitting gas-fired power plants.

And with emissions firmly cemented as the industry’s chief persona non grata, CCS has suddenly taken a centerstage role in the planning of several of the biggest gas discoveries in Southeast Asia.

This will make Southeast Asia, and because of its CO2-laden sour gas fields, an important case study to monitor for years to come. Rystad’s breakdown of Southeast Asia gas supply outlook helps explain why.

- By 2030 natural gas is expected to account for more than two-thirds of Southeast Asia’s total hydrocarbon production.

- More than half of those future molecules will come from an untapped discovery—roughly 90% of which are found offshore.

- Rystad’s numbers also show that about 40% of this expected offshore gas contains high quantities of CO2 or other contaminants.

Memories of Gorgon Loom

Even more striking than the projection made for Kasawari, Rystad foresees a doubling of breakeven prices for the BP-operated Tangguh gas field off Papua New Guinea to around $6.50/Mcf. Found at a water depth of around 60 m (200 ft), BP is considering adding a CCS phase to the field using a depleted subsea reservoir.

A recent discovery offshore Indonesia that may be impacted is the Abadi LNG project. Japan’s Inpex, the field’s operator, is still evaluating the investment needed to tap into nearly 10 Tcf of offshore gas. One consideration it is looking at is the potential inclusion of an CCS facility which Rystad estimates would mean first gas breakeven at around $8.00/Mcf.

Looming in such scenarios is the industry’s recent history with CCS projects that have failed to live up to expectations.

Petronas has not shared many details about the Kasawari CCS scheme—including projected costs. But it has said it expects to store a total of 76 million Mt in its offshore storage site which is roughly 75% the volume Chevron is aiming to achieve with its CCS operation attached to the Gorgon LNG plant.

The comparison is highlighted in the Rystad paper which characterized the Gorgon LNG development as “an unforgettable experience, proving CCS is still incredibly complex.”

With a reservoir content of around 14%, Gorgon’s development called for a CO2-injection rate between 3.5 and 4.0 mtpa.

This scale maintains the Chevron project as host to one of the world’s largest CCS facilities. Marring its grandeur, however, is that CCS began operations 3 years behind schedule, which meant the LNG plant that was already on line was forced to vent several-more megatons of CO2 than planned.

By the time it started up in 2019 in Barrow Island off Western Australia, the CCS facilities at Gorgon cost the US-based supermajor $3.1 billion. This reminds that unlike Petronas’ CCS project, the Chevron project was constructed onshore, albeit in a remote location.

Chevron has gone on to face a number of issues after starting up the CCS plant, some understood to be caused by sand blockages in the storage reservoir. This has forced LNG operations to vent additional CO2 which resulted in Chevron and its partners agreeing to purchase more than $160 million in carbon credits last year.

A First Time for Everything

Southeast Asian executives did not shy away from the fact that they are new to the CCS game during conference discussions.

Chen Kah Seong, vice president of the center of excellence at Petronas, noted while on stage that his company had been engaged in CCS demonstration projects with Japanese partners since the early 2000s. Then he shared that a different mood struck when Petronas assumed the lead role in its megascale Kasawari project.

“When you are doing this for the first time, there’s a tendency of conservatism,” he said of the early decision-making process. While holding off from sharing specific examples, Chen added it became clear early on that the company could not climb the learning curve in isolation.

That meant calling up and meeting with colleagues from other companies with experience in CCS. He related that following “a lot of cycles of conversation” with those outside voices, “You come back, look at it and say, ‘Hey, we missed this. Let’s do it again.’”

The knowledge sharing is now flowing back out from Petronas and toward Thailand’s PTTEP, which is its partner in the Lang-Lebah sour gas project.

Found off Sarawak in 2019 with up to 4 Tcf of gas reserves, Lang-Lebah is the Thai national oil company’s largest discovery ever made and also is seen as a critical source of future supply for the Petronas-owned Bintulu LNG facility.

Its estimated reservoir content includes 17% CO2, which has project planners looking at the addition of Malaysia’s second major offshore CCS project. Rystad figures if the project becomes operational with a ready CCS capability, first gas will break even just shy of $6.00/Mcf.

As the front-end engineering goes forward, Nopasit Chaiwanakupt, a senior vice president at PTTEP, stressed the importance of its early collaborations with Petronas and state regulator, Petronas Malaysia Petroleum Management.

“We need cooperation, and we need to learn from each other instead of wasting time,” he said. “We don’t have to reinvent the wheel; we don’t have to go through the same mistakes.”

What To Do if CO2 Leaks, and How To Avoid It

One mistake no one in this arena wants to make is to ignore the risks associated with CO2 leakage.

In Malaysia’s case, 16 depleted fields have so far been identified with a CO2 storage capacity estimated to be around 46 Tcf. On paper, these spent assets boast enough pore space to store all of the nation’s future emissions and then some.

But what happens if some of the injected CO2 finds its way out?

In OTC 31447, authors from Petronas share how the company used numerical modeling to study this problem in an area where it plans to begin injections in a few years off Sarawak. The simulated culprits were P&A wells that had become pathways for fugitive CO2.

The paper keys in on two scenarios:

- A relatively small 6-mtpa leak from a set of three P&A subsea wells

- A larger 500-mtpa leak from a single P&A wellbore that lost zonal isolation

For some perspective, the biggest of these leaks might account for less than 1% of what Petronas is looking to inject at its Kasawari CCS project.

What the models show is that the smaller leak would have a negligible effect on marine acidity over a 3-year period.

For the bigger leak, a slightly acidic plume might form close to the seabed. This would be contained to a localized area near the wellhead, and maybe as little as 1% of the decreases in pH would exist beyond a 200-m radius.

While some may not describe that outcome as ideal, a finding more likely to induce confidence is that the 500-mtpa leak did not result in any of the CO2 bubbling to the surface and into the atmosphere.

Instead, the model predicted that leaks on this order and at such depth will fully dissolve the CO2 gas bubbles before they rise more than 5 m above the seafloor.

The bottom line for Petronas is that the modeling results show that small amounts of seepage present a low-risk concern. The data will also help in the company’s future monitoring efforts as subsea storage begins.

OTC 31562 from Schlumberger, Norwegian drilling management firm AGR, and the Australian government-backed CarbonNet Project covers another angle—how to prevent leaks from newer wells.

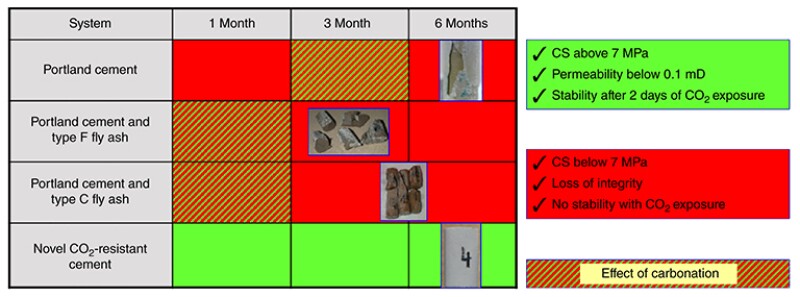

Australia’s first CCS injection appraisal well was drilled in December 2019/January 2020 and the thrust of the paper involves the P&A job performed shortly after. What the case study calls attention to is that CO2 does not only pose corrosion risks to steel pipe, it can also weaken the cement typically used in well construction and P&A.

The problem involves the effect on the traditional go-to cement of liquid CO2 held at or above its critical temperature and critical pressure (i.e., supercritical) or the effect of the carbonic acid formed when CO2 gas is dissolved in water.

Found at the local hardware store, Portland cement is also an industry mainstay that has been pumped down countless plugged wells around the world.

It is also relatively unprotected against a CO2-induced reaction known as carbonation. Tests done in a Schlumberger laboratory show that within 6 months of CO2 exposure cured core samples of Portland cement were deteriorating as material slowly leached out.

Ariel Lyons, a paper coauthor and customer engagement coordinator at Schlumberger, explained at the conference how this loss of integrity takes shape over time:

“In the first few weeks of exposure to CO2, the carbonation front eats away at the cement sheath and you start to lose the mechanical strength. At about a month, micro cracks start forming and calcite deposits grow, leading to a further loss of compressive strength and increased permeability.

“Over the years, the cement sheath erodes away to the point that the casing itself is exposed. And this leads to casing deterioration. And at that point, there are many pathways that the CO2 can take to migrate up to the surface.”

With an eye on building a CCS hub for Australia’s industrial emissions to the tune of 7 mtpa in the coming years, CarbonNet elected to mitigate such a zonal isolation risk when the time came to P&A its first appraisal well drilled into a storage system.

To do that, it used a commercial CO2-resistant cement designed by Schlumberger and that has been used in more than a dozen locations worldwide in high-CO2 wellbores, including those in CCS fields. While details of the service company’s cement material were not shared in the paper, it noted Schlumberger’s formula essentially does not produce the critical reactions that lead to the cement leaching and weakening.

Don’t Forget the Midstream Piece

While sharing other important lessons about ramping up CCS, an energy executive from China emphasized an area deserving of more attention is CO2 transportation and its costs.

For smaller Southeast Asian countries, this raised talk of a cross-border framework that would enable CO2 to move easily from one country’s emitters to another’s storage hub. This would be similar to Norway’s Northern Lights project.

Without the necessary policies in place, Chaiwanakupt from PTTEP said it’s too early to plan for such a development but implied it will eventually be needed to spur domestic storage.

He compared the concept to PTTEP’s own strategy involving projects in a foreign country “where we sell gas to the export market for a higher price and then we use the earnings from that project to subsidize gas for local use.”

Chaiwanakupt added, “Maybe we have to have an open, cross-border [CO2] project so that we can get income and revenues from the higher-carbon-price market to subsidize our local clients, the clients who cannot afford the higher capital costs.”

These expressions reveal how upstream companies are understanding that they have not only entered into the storage business, but the moving business as well. Alas, this means more technical boxes need to be checked.

Because it is corrosive, CO2 needs to be in pipelines at concentrations each is designed to tolerate. Because it is a gas and has volume, captured CO2 needs to be sent where there is room for it.

As it ambitions to become a CO2 hub operator, Petronas is working to sort out how existing pipelines and facilities can be best used to ship CO2. Using this infrastructure will keep capital and operating costs down.

The trick is knowing how to direct the traffic.

In OTC 31490, the company’s software approach called network simulation modeling is being “leveraged to scrutinize the infrastructure” and create a “dedicated corridor” for sour gas with a high CO2 content.

This kind of modeling is viewed as critical for anticipating various loading scenarios and designing routes to processing sites that can handle certain concentrations of CO2.

At the same time, Petronas’ system was built to identify “bad actors” or equipment and processes that were bottlenecking the most efficient transportation options.

When pipeline networks are not the answer, then the next best thing might be a CO2 shuttle. We’ve seen a forward-thinking concept from Equinor that called for autonomous submarine tankers.

But perhaps details presented by Technip Energies at OTC Asia could be considered a more practical near-term approach. The company’s concept is called the Offshore C-Hub, and as presented in OTC 31566 centers around what amounts to a floating storage and offloading unit for liquefied CO2.

Picking up the industrial-sourced CO2 from port storage tanks would be a small fleet of custom-built tankers that could be up to 250 m long for the most remote offshore projects that are several mtpa in capacity. Aside from carbon taxes, such a proposal needs to ensure the whole system is designed to enable a continuous injection rate into the storage formations.

Technip Energies said once terms are finalized, a C-Hub could be up and running within about 3 years. The paper’s authors explained that such a short time frame to delivery is plausible because the entire system can be assembled using mostly established technologies.

That includes the mooring systems now utilized for floating production, storage, and offloading units, to which the CO2 tankers would attach.

Technip Energies believes a relatively rapid deployment may help its concept compete with pipeline projects while providing the added benefit of being easily relocated to another location.

For Further Reading

OTC 31335 Billions of Barrels at Risk in Southeast Asia Due to Sour Gas by Prateek Pandey, Rystad Energy.

OTC 31447 CO2 Leakage Marine Dispersion Modelling for an Offshore Depleted Gas Field for CO2 Storage by M Rashad Amir Rashidi, Petronas; Edgar Peter Dabbi, DHI Water & Environment, et al.

OTC 31562 Cementing the First Australian Offshore Carbon Capture and Storage Appraisal Well by Ariel Lyons, Mahdi Sheikh Veisi, Amir Salehpour, Cinto Azwar, and Shameed Ashraf, Schlumberger; Lynden Duthie, AGR; and Steven Marshall, CarbonNet.

OTC 31490 A Shift in a Paradigm for Monetization of High-CO2 Fields by Leveraging Simulation Modelling Approach for Malaysian Gas Network by Sukrut Shridhar Kulkarni, Petronas.

OTC 31566 A Floating Hub Solution for Offshore CO2 Injection and Sequestration by Audrey Lopez, Cyrille Dechiron, and Morvan Favennec, Technip Energies.