The oil and gas industry overall had a solid financial year in 2018, but the exploration and production (E&P) sector has still maintained the focus on capital discipline and returns forged in the wake of the oil price downturn 4 years ago. Analysts at S&P Global Ratings said that heightened price volatility and investor demands for improved returns on their investments are among the issues driving measured CAPEX and mergers and acquisitions activity in 2019.

“Companies are no longer rewarded when they show growth for growth’s sake,” said David Lagasse, associate director for oil and gas at S&P Global Ratings. “Investors are looking for companies that generate free cash flow and can give that cash to shareholders or pay down debt. Companies that outspend cash flow just for the sake of growth are being hit hard by investors.”

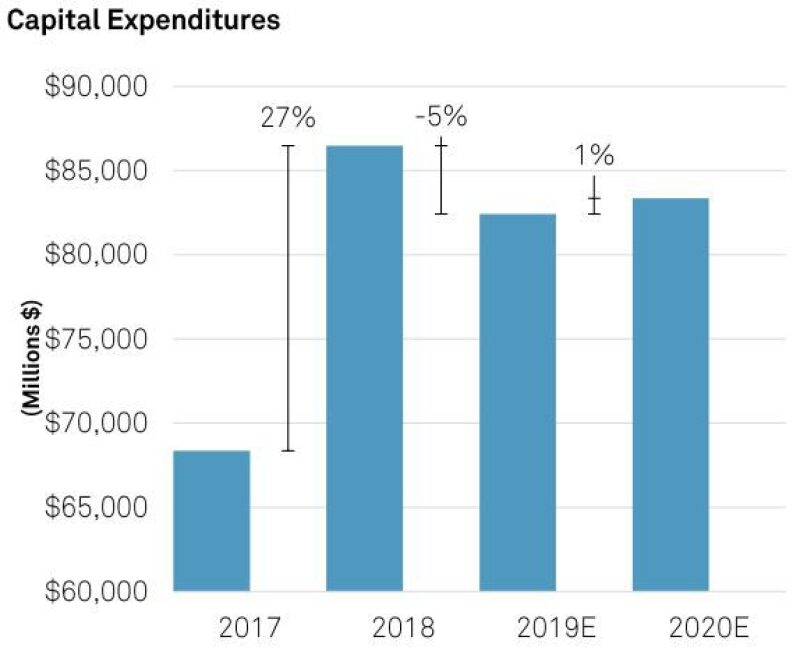

Speaking at a presentation on capital discipline in oil and gas, Lagasse said an emphasis on maintaining breakeven or better cash flow is one of the positive trends developing out of the E&P sectors. Companies are enacting lower capital spending programs and seeing stronger balance sheets as they repay debt. Paul Harvey, director of oil and gas for S&P Global Ratings, said that, after a relatively modest level of debt maturities in 2019, debt level should quickly build form 2020 to 2022. For some E&P companies, capital discipline will drive free cash flow, making it easier to continue paying down debt and further helping balance sheets that Harvey said had too much leverage in the current price environment.

“The capital markets have changed for the oil and gas industry. They’re becoming much more competitive. Investors want a lot more in terms of balance sheet strength and returns,” Harvey said.

These positive trends have been reflected in S&P’s rating assessment, which has approximately 70% of E&P companies listed as stable.

Along with price volatility, another negative trend Lagasse noted was geopolitical concern, particularly with regard to trade between the United States and China. With trade tensions ramping up and general concerns of slowing activity reported across several regions in the US, demand growth remains a big concern for E&P. He also referenced regulatory and environmental risk, with states issuing stronger regulations to curb methane emissions from hydraulic fracturing operations.

Capital discipline has led to increasingly efficient operations—despite US oil rig counts declining by roughly half since the end of 2014, oil production is at an all-time high. While this is good for E&P companies that can operate on lower price levels during the recovery from the downturn (Lagasse said several larger E&P companies are using $50/bbl WTI estimates to comprise their 2019 budgets), oilfield service (OFS) companies have been stuck with lower margins and lower revenues than many expected.

“It’s been said that some drillers are their own worst enemies. E&P companies and oilfield service companies have become increasingly efficient, using technological and operational advances to reduce the rig count, all the while increasing oil production to all-time highs. The improved productivity and efficiency has combined with investor sentiment to grow production at a more modest place while living within cash flows, and this has resulted in reduced E&P spending, impacting the oilfield service companies’ ability to gain margins,” Lagrasse said.

Harvey said completion services have been particularly hit by the lower margins.

“There’s an overcapacity in completions equipment and that industry has really taken it on the head,” he said. “Depending on who you talk to, some people think it’s hit a floor, others think it might weaken further, but we’ll see. The industry needs to reduce that oversupply either through wear and tear or just through taking it out.”

S&P’s OFS sector outlook is negative, and major companies like Halliburton, Schlumberger, and Weatherford have seen a downgrade in rating, but international OFS markets have shown steady improvement. Harvey said the offshore markets appear to have troughed and some (such as the jackup market) are showing signs of life. North American OFS markets are expected to remain challenging in the coming year, but improved Permian pipeline capacity could spur completion activity.