An international bidding round for oil and gas announced on 1 August is Egypt’s most recent move to bolster its lackluster economy. The country is facing a severe dollar shortage as a drop in tourism, capital, and exports have caused international reserves to sink by more than half to USD 16.4 billion since the political instability in 2011. Economic activity and vital imports also have been limited by the country’s arrears owed to foreign oil companies.

In July, Petroleum Minister Tarek El- Molla said the arrears were reduced to USD 3.4 billion in 2015–2016 from USD 3.5 billion a year earlier. He said the crude oil and natural gas received from the foreign partners’ share during 2015–2016 was worth USD 5.4 billion, and Egypt paid the partners USD 5.5 billion.

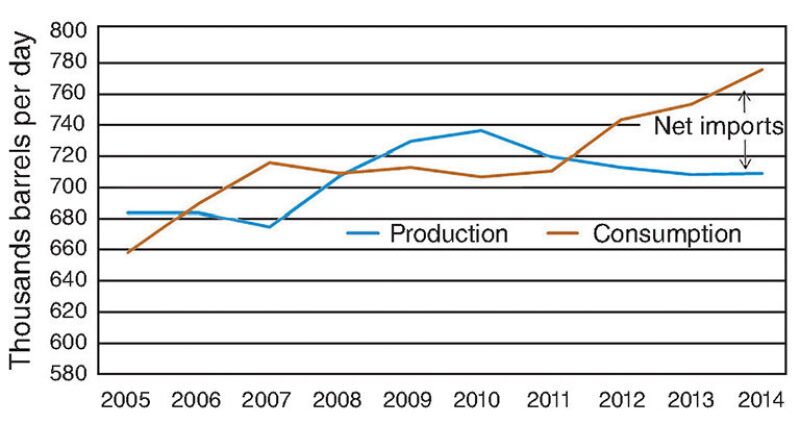

Egypt was once an oil exporter, but declining production and increasing subsidized consumption have turned it into a net importer. It is dependent on imported gas largely from Iraq and Jordan to keep pace with the country’s demand.

The high cost of energy subsidies in Egypt has contributed to the country’s budget deficit and the inability of the Egyptian General Petroleum Corporation (EGPC), the country’s national oil company, to pay off its debt to foreign operators. In the fiscal year (FY) 2013–2014, Egypt spent USD 18.2 billion on oil product subsidies and USD 1.8 billion on electricity subsidies. In FY 2014–2015, the Egyptian government projected the cost of oil product subsidies to fall to USD 9.2 billion as a result of its implemented subsidy reforms and the drop in global crude oil prices since mid-2014. However, Egypt’s spending on electricity subsidies has increased and is budgeted to cost USD 3.6 billion in FY 2014–2015.

To avoid significant backlash from the public at the prospect of dwindling subsidies, which now account for approximately one-fifth of the government’s total budget, the country is looking to increase production by appealing to foreign investment in its oil and gas sector.

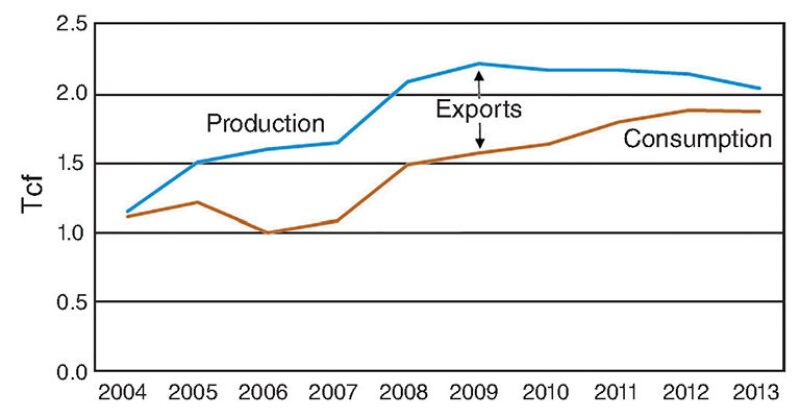

From 2012 to 2013, Egypt’s dry natural gas production declined by 5%. Substantial natural gas discoveries in the Mediterranean Sea and in other areas have been undeveloped because the price that the government was willing to pay foreign operators for the gas was too low, making some projects commercially unviable. However, in recent years Egypt has signed deals to pay foreign operators a higher price for the natural gas they produce.

New Agreements, Bidding Rounds

With an eye toward energy security, the country plans to accelerate the development of oil and gas discoveries, aiming to boost gas production by approximately 6 Bcf/D over the next 5 years involving an investment of more than USD 35 billion, El-Molla said in May. Last month, the government reported that current investments in new oil industry projects amount to approximately USD 7.7 billion, much of it stemming from new refining projects and the development of existing refining units.

El-Molla said the undiscovered potential in the Nile Delta Cone (232 Tcf), Levantine Basin (122 Tcf), the Western Desert (100 Tcf), and the Gulf of Suez (112 Tcf) provide further enticement to foreign investment.

The country’s desire to seek investments was demonstrated last month when Egypt’s Ministry of Petroleum announced that the Ganoub El Wadi Petroleum Holding Company (Ganope) issued a new international bid round for 10 exploration blocks in the South Gulf of Suez and the Western Desert (closing date of 30 November). This follows an international bid round issued in May (closing date of 31 August) by EGPC for 11 exploration blocks in the Gulf of Suez and Western Desert.

Recent oil and gas exploration contracts signed by the Ministry of Petroleum signal the move toward new production. Two new agreements were signed in July for oil and gas exploration at the Al Baraka area in Upper Egypt for Ganope, with the US company IPR and Cyprus subsidiary Mediterra. The Ministry cited a minimum investment of approximately USD 4.3 million, in addition to the drilling of three exploratory wells and a signature bonus of USD 200,000.

Last month, the Ministry approved five oil and gas drilling and exploration agreements. Four of the deals are offshore Mediterranean gas exploration and drilling agreements between the Egyptian Natural Gas Holding Company (EGAS) and BP, Eni, Total, and Edison. The fifth agreement, for oil drilling in the Gulf of Suez, is between EGPC and Trident Petroleum Egypt.

Supergiant Zohr on Fast Track

Following recent exploration successes in other countries in the Eastern Mediterranean, Eni’s August 2015 announcement of the discovery of the supergiant Zohr field, a 850-bcm natural gas field in the deepwater Sohar basin offshore Egypt, sparked optimism for Egypt’s economic rejuvenation.

The Zohr field holds more than 32 Tcf of gas in place. Onshore site preparation began in March, and production is expected by the end of 2017, with a progressive ramp up to reach a volume of about 75 million std m3 of gas per day by 2019. Eni was on plan to complete the fifth development well in July, and to begin drilling the sixth last month.

Eni’s Chief Executive Officer Claudio Descalzi said last September that it would take up to USD 10 billion to bring the Zohr gas to production. Contracts have been awarded in the past few months for the fast-track project.

OneSubsea won an engineering, procurement, and construction contract totaling more than USD 170 million from Belayim Petroleum (Petrobel), a joint venture between EGPC and Eni, to supply the subsea production systems for the first stage of the project. The scope of contract includes six horizontal SpoolTree subsea trees, intervention and workover control systems, landing string, tie-in, high-integrity pressure protection system, topside and subsea controls and distribution, water detection and salinity monitoring, and installation and commissioning services.

Aker Solutions won a contract worth more than NOK 1 billion from Petrobel to deliver 180 km of steel tube umbilicals, its longest-ever, that will connect the Zohr subsea development to an offshore control platform. The umbilical systems will be delivered by mid-April 2017.

Petrobel awarded Saipem an engineering, procurement, construction, and installation (EPCI) contract, the scope of which includes the installation of a 26-in. gas export trunkline and 14-in. and 8-in. trunklines, EPCI work for the field development in deep water (to depths of 1700 m) of six wells, and the installation of the umbilical system. Work was slated to begin in July and is due to be completed by the end of next year.

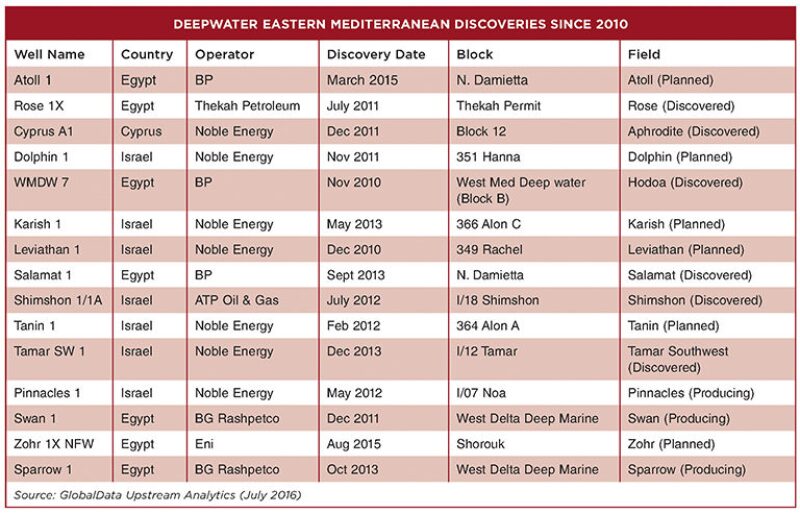

Other Eastern Mediterranean production is coming from Israel’s 9.9-Tcf Tamar field, which was discovered in 2009. Undeveloped discoveries in the region include the Leviathan field (22.9 Tcf) discovered offshore Israel in 2010, and the 4-Tcf Aphrodite field offshore Cyprus discovered in 2011.

Gas Imports Needed

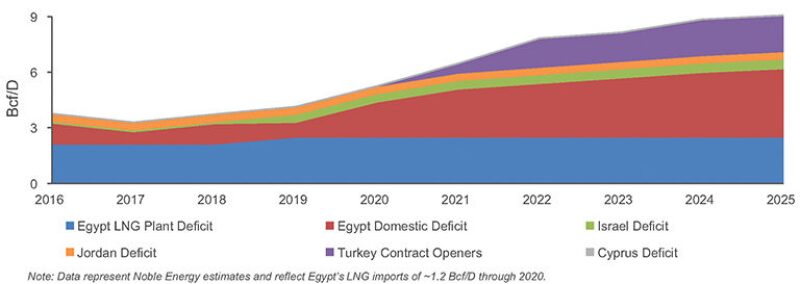

Until Egypt gets its newly discovered fields up and producing, it seeks critical gas imports. While several options appear to be possible, the complexities of regional agreements present challenges.

Last December, Israel’s National Infrastructure, Energy, and Water Minister Yuval Steinitz approved the first deal to export gas from the Tamar field to Egypt’s Dolphinus Holdings under a 7-year agreement. In the USD 1.2-billion deal, the idle East Mediterranean Gas (EMG) pipeline was slated to be used to transport 5 bcm of gas to Egypt.

However, EMG rejected the deal, contending that exporting gas from the Tamar reservoir to Dolphinus using its pipeline would harm competition, and the company has no intention of taking part in it. EMG also points to regulatory questions and its ongoing arbitration with Egyptian gas companies EGPC and EGAS related to the halt in the supply of gas from Egypt in 2011.

Bloomberg reported in May that Israel may agree to settle for half of the USD 1.73-billion fine Egypt was ordered to pay it so plans for exporting Israeli offshore gas there can proceed. Deals between Egyptian and Israeli companies had been progressing when an international arbitration court last December ordered Egypt to pay Israel damages for violating a contract to supply Israel Electric with Egyptian gas. Egypt exported natural gas to Israel until it canceled the agreement in 2012 as its wells became depleted and the EMG pipeline was subject to saboteurs. Negotiations continue and both countries will have to approve any final figure.

Israel’s Leviathan gas field is another possible source for Egypt’s gas imports. The Israeli government approved the development of the field in June. Containing an estimated 622 m3 of natural gas, the field is expected to be operational by 2019. The project will cost at least USD 5 billion, according to Noble Energy, which owns a 40% stake in the field.

Although Egypt’s own gas supplies exceed Israel’s, they are being used for municipal power supply. Importing Israeli gas could help the country’s industry sector, for which gas supplies are often limited in order to satisfy public demand, and fuel economic growth.

A July visit to Israel by Egypt’s Foreign Minister Sameh Shoukry, the first visit to Israel by an Egyptian foreign minister in 9 years, hinted at the possibility of new deals between the two countries. Discussions about gas imports to Egypt and regional cooperation in building infrastructure for gas imports to Asia or Europe were scheduled.

This article appears in the September 2016 issue of JPT.