High energy prices and a greater focus on energy security will not slow the world’s long-term ambition for a low‑carbon future. However, annual analysis by DNV believes unprecedented pressure is reinforcing a two‑speed energy transition.

Despite the turbulence across energy markets and the crisis in Ukraine, the company’s latest Energy Transition Outlook states that the cost of solar and wind energy and rising carbon costs, hitting EUR 100 ($109) in Europe, will outweigh the present short‑term shocks to the energy system. For the first time, the forecast sees non-fossil energy nudge slightly above 50% of the global energy mix by 2050, largely due to the growth and “greening” of electricity production.

While global intentions to abate carbon emissions and curtail global warming are aligned, lower-income regions, where cost is the main driver of energy policy, are seeing a totally different trend.

Europe—The Leader of the Decarbonization Pack

Europe is the clear frontrunner as it looks to double down on renewables and energy efficiency to achieve net zero and strengthen its energy security to attain energy independence in the longer term.

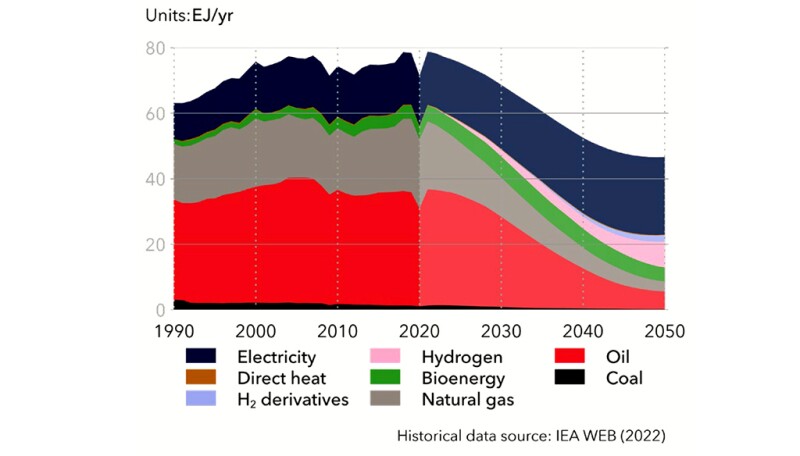

Final energy demand will change profoundly in the next 3 decades and will decrease by 21%, influenced by energy-efficiency gains and rapid electrification. For instance, due to the COVID-19 pandemic and supply shock emanating from the invasion of Ukraine, gas consumption will fall dramatically in the short term to almost half the amount in 2050. Gas will meet just 10% of Europe’s energy demand in 2050 compared with 25% today (Fig. 1).

Fossil fuel use will be more confined to a few sectors representing only 28% of the primary energy mix by 2050. Oil demand will decrease from 19 exajoule (EJ) in 2020 to 8 EJ in 2050 and will mainly come from nonenergy use in the petrochemical industry (40%) and transport (37%). The strong decrease in demand will mean that total imports will decrease by 61% for oil and 64% for natural gas from 2020 to 2050.

Meanwhile, the share of renewable energy will rise from 40 to 45%. EU targets include:

- 320 GW of solar PV capacity by 2025 and almost 600 GW by 2030

- Half of electricity to come from wind by 2050. This will see onshore wind expand from 173 GW today to 1,000 GW. Offshore wind will rise fivefold from 60 GW wind by 2030 to 300 GW by mid-century.

The REPowerEU strategy explicitly ties energy independence from Russia with increasing clean power and energy efficiency. With a host of initiatives aimed at ending the dependence on imported Russian fossil fuels by 2027, around EUR 210 billion ($229 billion) additional investment is needed over the next 4 years. The plan builds on the full implementation of the Fit for 55 proposals and suggests going further with higher renewable energy targets, including hydrogen and nuclear, and more meaningful energy efficiency efforts.

To speed up deployment, the region will establish dedicated go-to areas for renewables with shortened and simplified permitting processes in areas with lower environmental and social risks.

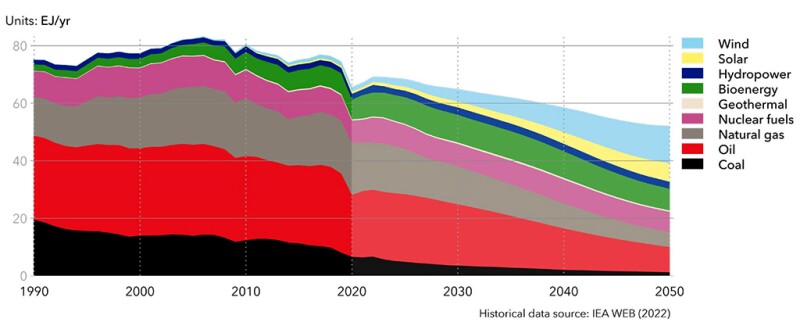

In the coming decades it is anticipated that the European energy system will undergo an energy transformation more profound than that of any other region (Fig. 2).

DNV’s Pathway to Net Zero report, an analysis on what is required to enable the world to reach net zero emissions by 2050, indicates that Europe would need to reach net zero by 2043 for global temperatures to stay within 1.5°C (and assuming other regions achieve specific net zero timelines). In that case, European CO2 emissions would drop from 2.9 Gt in 2020 to –0.1 Gt by 2050, and to –0.4 Gt with direct air capture. It also asserts that by backing up pledges with real policy, the region will boast the highest carbon-price level, from $150/tCO2 in 2030 to $250/tCO2 20 years later.

Lagging but not Losing the Climate Battle

Unlike ramped-up climate change advances in Europe, the transition to low carbon in North America is moving slower. This laggardness has been compounded by anti-dumping investigations targeting Chinese solar cells/modules and limits placed by the US Supreme Court on the powers of the US Environmental Protection Agency.

While there remains a deep-seated reluctance to climb down from its fossil fuel dominance, the mindset is starting to shift. The passage of the US Inflation Reduction Act makes large investments in renewable energy with the duration of the support lasting into the 2030s.

Both the US and Canadian governments are striving to achieve net zero greenhouse gas targets: intermediate goals for 2030 are 50–52% of 2005 levels (US) and 40–45% (Canada). Both federal governments are pursuing cooperative transition efforts, through the Mission Innovation, Net-Zero Producers Forum, Global Methane Pledge, and the Climate Club of the G7.

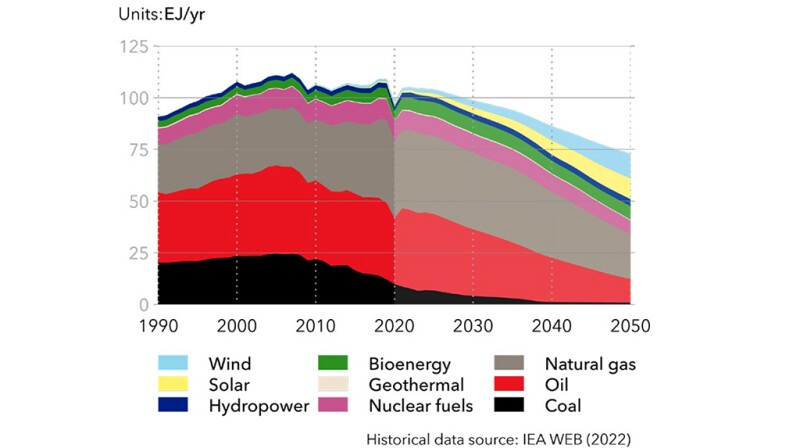

Regardless of climate change intentions, North America will still be heavily reliant on natural gas in 2050 (Fig. 3) with renewables comprising only 34% of primary energy consumption.

In terms of world primary energy supply, North America comes in second, consuming 17% of the world’s natural gas in 2050, behind the Middle East and North Africa. Compared with a similarly developed region like Europe, which will have one of the lowest levels of natural gas consumption in 2050, North America is on a very different path.

The main reason for natural gas dominance is its affordability as modest carbon pricing keeps natural gas cheap. This is unlikely to change until the 2030s when it is anticipated that gas will be outpriced by renewable technologies, including wind, solar, and hydrogen. Higher carbon prices in some states and Canada does not change this general picture.

DNV analysis predicts that natural gas will overtake oil as the largest primary energy source in North America within the next few years. This marked decrease in oil use, especially in the transport sector, will see the share of oil drop from 90% in 2020 to 46% by 2050.

However, while transition plans have progressed with Canada’s 2030 Emissions Reduction Plan and the US Inflation Reduction Act (2022), coming on the back of last year’s Infrastructure Investment and Jobs Act, high gasoline prices and energy security concerns have triggered calls to increase the regions’ oil output in the interim. This suggests that decarbonization efforts may be delayed.

DNV’s Pathway to Net Zero report indicates that under a Paris-aligned scenario, emissions in North America would decline by 68% by mid‑century with the average carbon-price level forecast to rise to $25/tCO2 by the end of the decade and $70/tCO2 in 2050. This entails North America capturing 205 MtCO2 per year in CO2 emissions, which is in the same range as Europe by 2050, and up from 42 MtCO2 in 2030.

A rapid reduction in natural gas and oil will drive down harmful emissions, supplanted by electricity and hydrogen, in the energy system: transport emissions will be the most challenging to abate. Policy-wise, the Canadian government is directing a Pan-Canadian approach and steadily increasing the economywide carbon price. However, as there is no federal policy in the US, pricing will be dominated by development in US state cap-and-trade schemes.

Paris Target Hangs in the Balance

While the DNV report asserts that inflationary pressures and supply chain disruption will pose a short-term challenge to renewable growth, the analysis suggests this will exert little long-term influence over a transition that will be rapid and extensive across the globe.

However, if the world is to reach net zero by 2050, global CO2 emissions must be reduced by 8% every year. This means North America must reach net zero well before 2050, OECD regions by 2043, and China needs to reduce emissions to zero by 2050 rather than the current goal of 2060.

The strongest push on the road to a global energy transition is the rapidly reducing costs of solar and wind energy, which will outweigh the present short-term shocks to the energy system. By 2050, they will grow 20-fold and 10‑fold respectively and will dominate electricity production.

Al-Karim Govindji, global head of public affairs for DNV Energy Systems, joined the company in 2018. His focus is on strengthening DNV’s relationships with national and regional governments, sector associations, as well as government affairs personnel of companies in the energy value chain. He follows policy related to technologies that are critical to achieving 1.5°C, such as renewables, hydrogen, CCUS, energy efficiency, and storage. Prior to this, he led DNV’s decarbonization and demandside management business across Northern Europe and Middle East & Africa, supporting industrial, commercial, and utility customers.

Previously, Govindji spent 9 years at the Carbon Trust on innovation policy in areas such as industrial energy efficiency, offshore wind, thin film PV, and sustainable aviation biofuels, running multimillion-pound programs for the United Nations and for the UK government. Prior to this, he worked for Kearney in operational strategy and for Bank of America in acquisition finance and corporate lending. He holds a BEng in chemical engineering from the University of Birmingham and an MBA from Oxford University.