This guest editorial presents a condensed version of the comprehensive industry white paper prepared for the Houston Offshore Technology Conference (OTC) as part of a 3-year Knowledge Partnership between OTC and Rystad Energy. The full white paper, which offers an in-depth analysis and broader insights, is available for download the report here.

The Evolving Offshore Energy Landscape: Navigating Transition and Opportunity

The global energy landscape is undergoing a significant and rapid transition, driven by increasing demand, policy shifts towards decarbonization, and technological advancements. While the urgency to reduce fossil fuel reliance and lower emissions grows, oil and gas remain fundamental to the world's energy supply, powering essential sectors such as transportation, heavy industry, petrochemicals, and electricity generation. The offshore sector sits at a critical juncture, facing the dual challenge of meeting persistent energy needs while reducing its environmental footprint. Offshore production is increasingly viewed as essential in bridging this gap during the transition.

Betting on Offshore

Between 2004 and 2012, offshore, particularly deepwater, was projected to dominate future oil production growth. Yet, the US shale oil revolution shifted this, with the unconventional sector driving global growth from 2013 to the present. Consequently, the significant deepwater expansion, potentially requiring up to 500 floating rigs, did not fully materialize. Both the oil market and associated supply chain markets collapsed in 2014, and the focus shifted to cost, performance, and drilling efficiency improvements. Today, capital discipline and prioritization of shareholder return trump production growth in shale, with offshore again competitive and poised for growth.

We are seeing a reborn offshore sector, but not at the level it could have been. Thus, instead of an offshore supply tsunami starting in 2012, we are ending up with a breeze wave 15 years later, at a more moderate finding and development cost level with Brazil, and other basins in the Americas and in Africa growing the most. For gas, East Africa has big potential and will be a new source of LNG.

Current Offshore Performance and Investment

The offshore sector remains a vital component of the global energy supply. In 2024, offshore oil production reached 28.4 million B/D, representing nearly a third of the world's total output, while offshore gas production hit approximately 115 Bcf/D, also contributing around 30% of global supply. Offshore fields represented 35% of total investment, 28% of production, and 30% of resources in 2024. These figures underscore the offshore sector's enduring importance.

Offshore investment also reflects this significance. While overall exploration & production (E&P) investment has held steady around $600 billion since 2023, about $210 billion was directed to offshore fields, a 5% increase from 2023.

Greenfield project sanctioning saw $110 billion allocated in 2024, with significant investment surges in South America (up 64% to $37 billion), Asia (up 33% to $21 billion), North America (up 33% to $14 billion), and Africa (up 17% to $6 billion).

Notably, over half of this greenfield investment is targeting deepwater projects, particularly in Brazil, Guyana, the US, and Suriname, highlighting the strategic shift towards these regions and emerging markets. Even as 2024 was a slow year for new discoveries overall, 80% of those made were offshore, predominantly in deep water, indicating continued exploration potential.

Future Supply, Demand, and the Role of Offshore

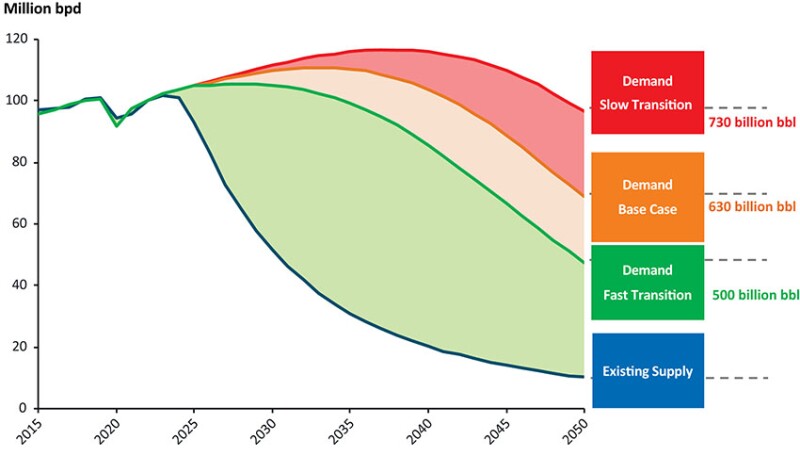

Global oil demand reached 103 million B/D in 2024, driven by growth in aviation and petrochemicals, particularly in emerging economies. Transportation remains the largest consumer. While oil will still be the mainstay in the near term, shifts towards cleaner technologies and efficiency gains are expected to moderate demand growth.

The transition maturity varies by sector, with passenger vehicles advancing faster than petrochemicals, trucking, shipping, and aviation. In the medium term, oil may retain its advantages in some sectors, as demand for petrochemical feedstocks is expected to grow. However, a more accelerated transition away from oil is anticipated in the latter half of the next decade as low-carbon technologies mature.

Future demand scenarios vary. A base case scenario suggests oil demand peaking at 110 million B/D in 2033. Even under fast transition scenarios, significant oil volumes will be needed. Meeting this future demand presents a challenge as existing production declines rapidly without new activity. Depending on the transition speed, between 500 and 730 billion bbl of new oil supply is required between 2024 and 2050.

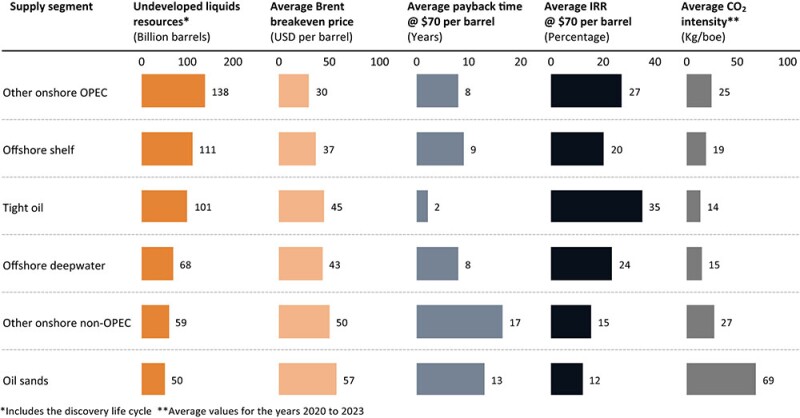

Deepwater supply is projected to outpace shale growth in the coming years, increasing by an average of 400,000 B/D annually from 2025 to 2030 before declining. Cost competitiveness analysis indicates offshore supply (shelf and deepwater) will play a significant role, with competitive breakeven prices compared to sources like oil sands and other onshore projects.

Offshore and Energy Transition

Achieving climate goals like those set in the Paris Agreement requires deep decarbonization. This involves transitioning the power sector towards more renewables (solar, wind, hydro, nuclear) and storage, electrifying end uses like transport and heating, and addressing residual emissions with solutions like carbon capture, utilization, and storage (CCUS) and clean fuels (hydrogen, biofuels).

The offshore sector is increasingly becoming a hub for these clean technologies:

Offshore CCUS: Offers vast storage potential in geological formations like saline aquifers and depleted reservoirs, often without land-use conflicts. Leveraging existing offshore infrastructure and expertise can reduce costs. Challenges include higher costs than onshore, logistical complexities, and evolving regulations. Projects are underway globally, including Norway's Snøhvit, Sleipner, and Northern Lights, and developments in the US Gulf Coast. Direct carbon capture on offshore facilities such as floating production storage, offloading, and storage units is also gaining prominence.

Offshore Wind: A rapidly expanding energy source harnessing stronger, more consistent winds offshore. Global installations are growing rapidly, driven by government targets. While bottom-fixed installations dominate, floating wind technology is advancing, projected to constitute about one‑eighth of the 658 GW offshore wind capacity expected by 2040. Europe leads, with the UK as a key market, followed by Asia.

Floating and Offshore Solar Photovoltaics (PV): Floating PV (FPV) involves installing solar panels on water bodies, offering benefits like reduced land use and potentially higher yields. Offshore PV is an emerging concept using specialized panels for marine conditions. The market is nascent, led by China, but faces cost, technological, and environmental challenges.

Other Marine Renewables: Geothermal energy, particularly leveraging oil and gas drilling expertise, is growing. Offshore geothermal potential exists but faces cost and technological hurdles. Tidal and wave energy offer predictability to complement intermittent renewables, though still require subsidies for industrialization.

Challenges and Enablers

The transition is not without hurdles. Rising greenhouse gas emissions remain a primary concern, demanding accelerated action. Supply chain disruptions, exacerbated by factors like recent US tariffs on steel, aluminum, and energy equipment, create cost volatility and sourcing challenges, particularly impacting tubular goods. Mitigation strategies include supplier diversification, inventory management, contractual adjustments, and leveraging digitalization for better visibility and risk management. Continued radical and incremental innovation is paramount for the whole offshore sector. It enables cost and emissions reductions, improves safety, and enhances operational efficiency.

Enabling offshore decarbonization and cost competitiveness requires further innovation.

Digitalization: Provides data for optimizing operations and supports electrification efforts.

Grid Infrastructure: Advanced transmission (e.g., high-voltage direct current) is vital for integrating large-scale offshore renewables.

Standardization: Standardized offshore platform designs can lower costs and speed up field developments.

Critical Minerals: Essential for technologies like wind turbines (rare earth elements) and batteries, but sourcing (e.g., deep-sea mining) raises significant environmental concerns.

Battery Storage: Crucial for grid stability with intermittent renewables.

Clean Fuels: Hydrogen and biofuels offer pathways to decarbonize offshore support operations like shipping and aviation.

Conclusion: A Balanced Path Forward

The energy transition demands a balanced approach, ensuring energy remains affordable and reliable while shifting towards cleaner sources.

Oil and gas, particularly from offshore, will remain essential for years to come, even as renewables expand. The offshore sector is pivotal, hosting both traditional production and burgeoning clean energy technologies. Successfully navigating this complex transition requires overcoming challenges related to infrastructure scaleup, technology costs, supply chain risks, and environmental impacts.

Ultimately, a collaborative effort between governments, industry, and researchers is needed to drive innovation, shape effective policies, and secure investment for a transformation that integrates energy security, economic growth, and climate action sustainably.

Maierdan Halifu is the North America Research Director at Rystad Energy. His expertise spans the energy value chain from upstream to downstream, leveraging data-driven analysis and strategic client engagement gained through roles as a shale analyst and client solution specialist. He holds an MSc in finance from the University of Gothenburg, Sweden.

Jarand Rystad is the founder and CEO of Rystad Energy, established in 2004. He has extensive experience in oil and gas strategy, having led projects for major energy companies, governments, and investors. A widely cited petroleum analyst and frequent keynote speaker, he specializes in E&P strategy, transactions and macro analysis. He holds an MSc in physics from the Norwegian University of Science and Technology, with additional academic background in philosophy and industrial economics.