A measure of optimism for the future of hydrogen as a major source of energy has been dashed in a new report from DNV.

In its first-ever standalone hydrogen forecast, the Norwegian-based assurance and risk management firm projects the clean-burning gas may reach 0.5% of the global energy mix by 2030 before rising to 5% by 2050.

This order of magnitude increase will mark the rise of a new industry—hydrogen for energy use.

But it will also fall far short of the at least 13% share of global energy mix that DNV said hydrogen must represent to meet net-zero emissions targets that are based around the Paris Agreement.

“What our report shows is that there is an increase in the use of hydrogen, but it’s just not fast,” said Hari Vamadevan, a UK and Ireland regional director at DNV.

He added that hydrogen is facing challenges not inherent to the build out of other renewable projects that are merely addressing a market need for more electricity.

"What makes hydrogen relatively unique is that you're trying to create supply and demand at the same time, and that's why it's a little bit more complicated," said Vamadevan.

The DNV report cited several bottlenecks to greater uptake including a lack of efficient infrastructure and a means to scale production. But the more overarching challenge DNV called out is the lack of government policies considered necessary to creating a robust market for hydrogen.

As the report reads, “Much stronger policies are needed to scale beyond the present forecast in the form of stronger mandates, demand-side measures giving confidence in offtake to producers, and carbon prices.”

A $7-Trillion Effort

Underscoring the nontrivial nature of what may be needed for hydrogen to reach 5% of the global mix is DNV’s estimate that doing so will require $7 trillion in spending over the next 3 decades. The figure includes:

- $6.8 trillion on hydrogen production systems.

- $180 billion on hydrogen pipelines.

- $530 billion on creating ammonia terminals.

This spending will be rather lumpy as different regions focus on different technology priorities over contrasting timelines. In general, the key regions to watch for growth in hydrogen production as laid out by DNV are Europe, North America, China, and Southeast Asia.

Europe is best positioned to displace the largest share of its current energy needs with up to 11% of hydrogen by mid-century. This would be followed by the advanced economies in Southeast Asia at 8%, North America at 7%, and China at 6%.

But in terms of total output, China is seen as leading the way by 2050 with 1,248 GW of electrolyzer capacity, or about 40% of the world’s total by that time. This compares with DNV’s projected 2050 capacity in North America of 305 GW and 574 GW in Europe.

DNV also noted that while a global market will likely come to fruition, hydrogen producers will remain very dependent on localized consumption. This is in part because it becomes uneconomic to transport hydrogen in pipelines beyond 2,000 km, or about 1,200 miles.

Domestic energy politics in much of the western world has also taken on a new tone recently, one that might help certain countries accept their share of hydrogen’s multi-trillion-dollar scope.

Vamadevan related that, “There’s an understanding now because of the crisis in Ukraine and the associated sanctions that there is a competitive advantage to energy security and energy independence.”

Therefore, he added, local and regional sources of hydrogen that would otherwise be “slightly disadvantaged by an incredibly low price of gas and oil globally,” as has been the case until recently, are now more likely to become bigger priorities for the world’s biggest energy consumers.

Policies Needed To Make a Market

The figures above are all dependent on various forms of government action and that those policies have some staying power. Such measures are also seen by DNV as critical for industrial and energy firms to take on a greater financial risk in building out hydrogen production infrastructure and supply chains.

Not least of these big moves is the price that is established for carbon emissions.

In DNV’s scenario, it is assumed that the world’s largest economies will set a price floor for carbon no lower than $20 and as high as $95 per metric ton of CO2 by 2030. In 2050, prices will have reached between $70 and $135 per metric ton. Europe is expected to set the upper end of these ranges.

Vamadevan described action on carbon pricing as “an important lever in terms of accelerating the current plans” for hydrogen expansion. However, he acknowledged that for much of the world the challenge for embracing carbon prices remains “an issue of when and by how much.”

A major commitment to building new renewable power projects will also be required since a global hydrogen market will demand dedicated wind and solar projects that do not directly compete with consumer demand for electricity. DNV said this surplus equates to 3,100 GW, or more than double today's installed generation capacity of solar and wind power.

Additionally, governments must help with funding projects aimed at establishing domestic consumption. “These are signals that the market can respond to,” said Vamadevan while noting as an example the UK government’s push to use hydrogen to heat many of the country’s homes.

Today, about 80% of central heating in the UK is made possible by natural gas but pilot projects with hydrogen taking that role are getting underway.

For its part, DNV is involved in testing the safe use of hydrogen inside homes as part of a UK government-funded project called HyStreet. DNV is also taking part in a similar project in the Netherlands and is involved in several other hydrogen-for-energy studies.

The Pathway to 5%

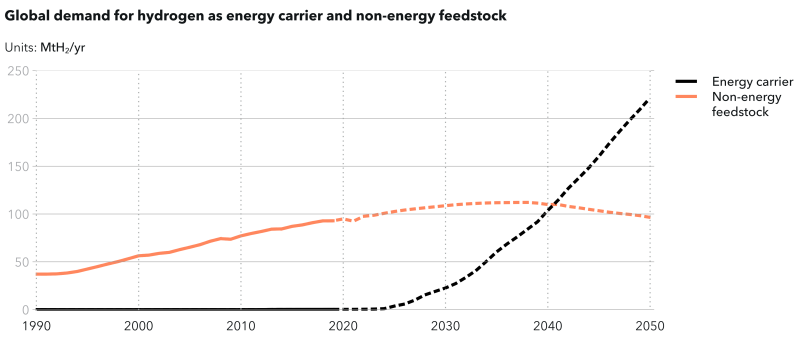

Current demand for hydrogen is around 90 mtpa which is equal to about 2% of the world’s energy supply. However, less than 5% of that supply is used directly to generate energy, heat homes, or as a transportation fuel.

Instead, hydrogen is primarily used for sulfur removal and heavy-crude upgrading at refineries and as a feedstock for ammonia plants that make fertilizer.

DNV does not see hydrogen moving far beyond these established use cases in the remaining years of this decade. It will simply remain too expensive outside of niche applications that are reliant on government subsidies.

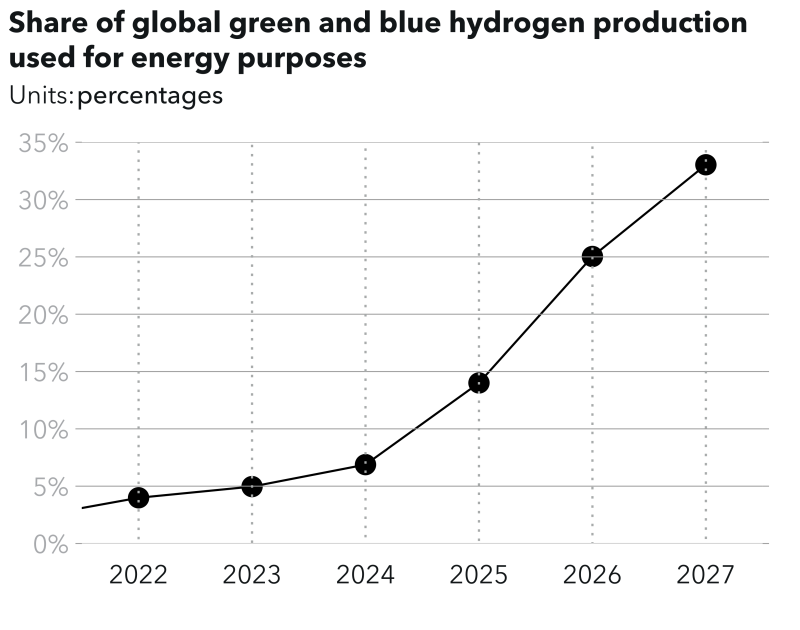

By 2030, things start to change in DNV’s scenario which expects a major price cut for hydrogen generated via solar and offshore wind energy sources, or green hydrogen. This would be possible thanks in part to the next several years of “cost learning” and a reduction in the cost of electrolyzer technology which DNV expects to fall 50% by 2050.

The all-in cost for these green sources of hydrogen is currently around $6/kW in North America and Europe. Sometime in next decade, the wider use of solar and wind power could result in an average global price for green hydrogen of around $2.50/kg which would be in the neighborhood of current costs for methane-derived blue hydrogen and grid-supplied hydrogen production.

Heating, both for residential and industrial use, will lead the way in terms of new demand growth during the 2030s. This reflects the lowest-hanging fruit for reaching consumers because it involves blending hydrogen with natural gas in existing pipelines.

DNV labeled the 2040s “the decade of demand diversification” and predicted escalating carbon taxes and net-zero mandates will mean hydrogen begins to touch more of the hard-to-decarbonize transport sector.

In other words, the higher cost of oil and gas consumption will open the door for competition from hydrogen.

While passenger vehicles are not likely to use much hydrogen, long-haul trucking is expected to see a large uptick in the adoption of fuel cells.

China is expected to be a leader in this regard. Of a $20 billion hydrogen fund that China recently stood up, DNV pointed out that half is to be routed into the creation of new hydrogen-based transport projects.

Maritime shipping currently consumes about 7% of global oil supply, which according to DNV, makes it another prime target for hydrogen displacement. This would be done by converting hydrogen from its gas form into ammonia which as a liquid is easier and cheaper to store.

DNV expects to see seaborne ammonia soar with a 20-fold increase in supply from 2030 to 2050. As a maritime fuel, hydrogen-derived ammonia will grow “from virtually nothing in the mid-2030s” to 95% of the market by mid-century.

The Role of Blue Hydrogen

So, what does all this mean for the oil and gas industry which is setting its hopes on becoming a major player in the shift toward hydrogen?

Among other things, DNV suggests there will be some crossover work for oil and gas companies or their employees who have compatible services and skill sets.

Vamadevan, who spent 30 years working on various oil and gas projects commented that the upstream industry is “used to de-risking big projects and knows something about gas.”

But DNV also warns that the oil and gas industry’s most synergistic hydrogen product will face increasing competition from those powered by solar and wind systems.

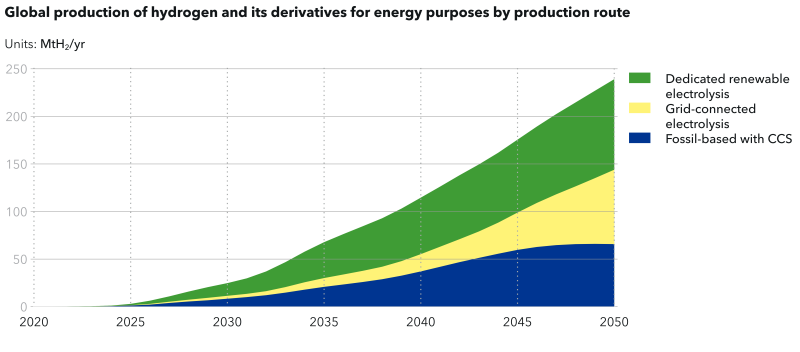

Blue hydrogen, that which is created by coupling the steam reformation process with carbon capture and storage (CCS), is currently facing challenges from high natural gas prices.

While prices are expected to relax in the coming years, DNV holds that “CCS is still a developing technology and concerns about long-term storage sites, uncertainties on future costs, and only marginal benefits from economics of scale are limiting the speed of deployment.”

By 2050, DNV forecasts that blue hydrogen may represent just over a quarter of global supply used for energy generation whereas more than 70% will come from a combination of grid-connected electrolysis and dedicated wind and solar electrolysis projects.

The biggest role for blue hydrogen that DNV expects by 2050 is for ammonia and methanol production. In addition to its current uses in refinery operations, these blue hydrogen derivatives will also be used to make marine fuel, gasoline blending, and aviation fuel.