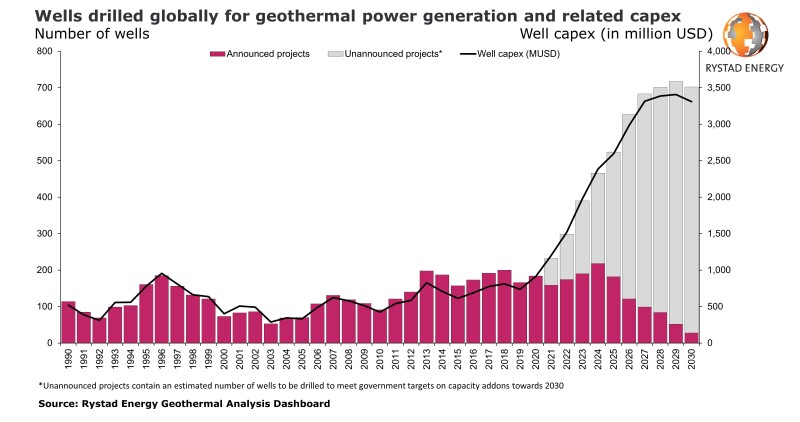

Renewed interest in the geothermal sector in recent years, which has seen oil and gas majors make investments in numerous startups, is set to see a new record in the number of wells drilled for power generation, surpassing 200 this year for the first time. Spending on geothermal activity is expected to boom in the coming years, with global well capital expenditure breaking the $1 billion threshold in 2021 before soaring to $3 billion in 2026, if government targets worldwide are to be met.

Geothermal and Petroleum Engineering: Where Subsurface Engineering Meet

An SPE Live event planned for 21 October is set to look at the intersection of geothermal and petroleum engineering. Read more about the event and register here.

According to Rystad Energy’s geothermal dashboard—which covers more than 1,700 geothermal power generation and direct use projects globally—there has been an uptick in drilling activity in the last 6 years. Rystad estimates that, between 2015 and 2020, approximately 1,100 geothermal wells were drilled for power generation, with an average of 180 per year in the period. The sector is set for significant growth, however, as Rystad said it expects to see approximately 500 wells drilled in 2025.

The firm’s wells forecast is split between announced projects and unannounced projects. For unannounced projects, it has estimated the number of wells that countries need to drill in order to reach government-set targets on geothermal installed capacity. Historically, such estimates have tended to exceed actual capacity additions. However, given the current high level of interest in geothermal, the pace of innovation has picked up, which could see more countries entering the fray.

“Whether or not geothermal targets will be met relies on the development of new systems like enhanced geothermal systems (EGS) and advanced geothermal systems (AGS),” said Daniel Holmedal, energy service research analyst at Rystad Energy. “If successful, we should see a big surge in well activity in multiple countries. Although targets have previously proved to be too ambitious, the current push in this growing industry is promising and could provide attractive opportunities for well services players.”

The geothermal sector has traditionally been dominated by high-enthalpy regions where wells have been drilled at depths of between 2,000 and 3,000 m. Looking at the active geothermal wells for power generation, most have reservoir temperatures of more than 200°C.

Given these temperature requirements, the well location factor has often proven to be a bottleneck for the scalability of geothermal as the number of countries that have high-temperature reservoirs located at 2,000 m or deeper is limited. New systems such as EGS and AGS are aiming to change this and make geothermal more accessible.

Although the fully realized commercial opportunity of these technologies may not be fully apparent before 2030, EGS and AGS developments offer the chance for the geothermal sector to grow significantly, Rystad analysts said. It said it expects the number of active wells for geothermal power generation to surpass 10,000 by the end of the decade. This increase could support a total installed capacity of 36 GW in 2030, more than double the installed capacity in 2021. Most of this capacity will be added between 2025 and 2030, with levels in 2025 expected to be around 23 GW.

In addition to geothermal for power generation, geothermal district heating is also gaining ground, with Europe and China the two main markets. Although there has been some recent focus on geothermal district heating in the US from the Department of Energy’s National Renewable Energy Laboratory, no specific policies have yet been put in place.

Some countries in Europe have already outlined their ambitions for geothermal district heating out to 2050. The Austrian Energy Agency expects to spend approximately $1.2 billion on geothermal district heating—comprising wells and infrastructure—between 2020 and 2050, with $215 million lined up for the period to 2030. Rystad analysts said they believe this will translate into approximately 40 wells being drilled between 2020 and 2030. In its heat masterplan, the Netherlands has provided an even more ambitious outlook for its geothermal district heating industry, with 20 wells per annum planned to be drilled between 2020 and 2025 and 40 each year between 2026 and 2030. Further growth is then expected toward 2050.

Additional interest in geothermal may be generated by the repurposing of existing oil and gas infrastructure as well as the extraction of lithium. The abandonment of oil and gas wells is predominantly a zero-return activity in economic terms, meaning geothermal could offer a life-extension opportunity to operators. In Europe, there are multiple examples of this, including the Zsana-Kiskunhalas project in Hungary that started up earlier this year. Lithium extraction from geothermal wells has also made headlines because it has a higher return compared with traditional uses of geothermal.