A reformed global upstream industry is turning the corner and could take a leap forward in 2018 following a 3-year purging of excesses. Activity growth is expected through continued unconventional development as well as from the beleaguered deepwater segment, but diminishing cost savings could discourage many still-cautious operators.

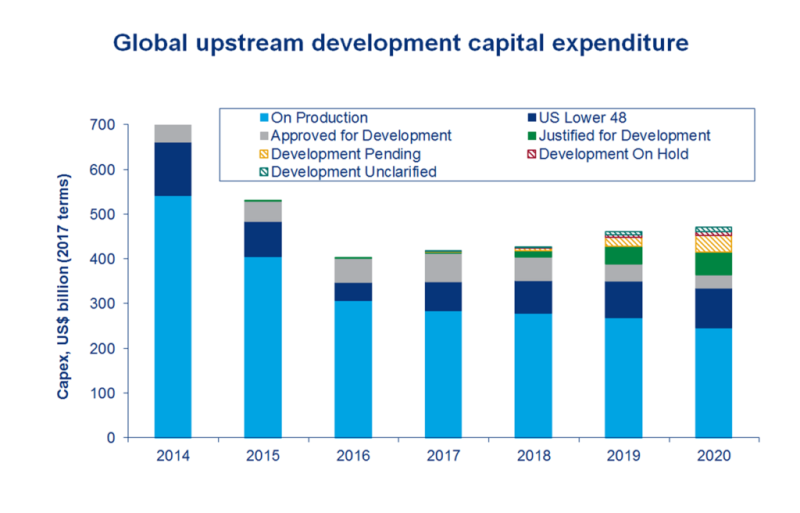

Consultancy Wood Mackenzie forecasts 2018 global capital expenditure to grow slightly to $400 billion after almost $1 trillion was removed from projected spending plans during 2015-20. The rise, outlined in its 2018 Upstream Outlook, reflects a 15% increase in spending for both unconventional and deepwater projects compared with 2017 levels.

A separate survey from Barclays forecasts an 8% year-over-year rise in global upstream spending in 2018. The bounce is still lower than previous recoveries in 2005 and 2011, which the bank attributes to a more conservative spending approach going forward. The bulk of the growth is expected to come in North America, and an uptick is seen from national oil companies (NOCs) and international oil companies.

“Now that the belt-tightening is done, companies are looking to deliver profitable growth and build for the future,” said Tom Ellacott, Wood Mackenzie senior vice president, corporate research. “We also expect to see signs that the investment cycle is starting to turn and the sector has reset itself to operate at lower commodity prices.”

The number of major project sanctions will increase to 25 in 2018 from just more than 20 in 2017, the consultancy predicts, representing a third consecutive yearly rise since a bottom in 2015. "The rise in project sanctions will be a clear sign that new projects can work in a low-price environment,” said Ellacott. Almost 80% of expected final investment decisions (FIDs) are greenfield, a notable uptick from previous years.

Portfolio Growth Opportunities Abound

"Oil and gas companies will continue to adapt portfolios to perform at high and low prices and also to provide a platform for longer-term energy transition," Ellacott said. “We’ve seen the majors being especially active in sweeping up bottom-of-the-cycle opportunities in 2017 to really strengthen their longer-term growth prospects. We expect to see more of this in the majors in 2018.” Larger companies, such as BP, will continue to build gas-weighted portfolios as part of their low-carbon transition.

Firms will focus on proving they can grow free cash flow at lower prices and fund higher shareholder distributions as part of a campaign to win back investors after a year of poor stock market performance, the consultancy predicted. Advancing a case for longer-term investment also will be a priority, which should be aided by ground-floor opportunities in the Middle East and Latin America.

Wood Mackenzie expects Iran and the UAE to award at least 10 billion BOE of discovered resources next year, while another 10 billion BOE of deepwater resources could be auctioned in Brazil. The year will kick off with Mexico’s next deepwater bid round, slated for 31 January, which offers 30 blocks to international firms.

“Looking at the upstream sector as a whole, we expect more activity from the Asian NOCs as they tackle structural production declines,” Ellacott said. “They really haven’t done much [mergers and acquisitions (M&A)] during the downturn, but we think they need to start reengaging in international business development. So expect to see more of them in 2018 as well.”

The majors during the downturn were most active in sanctioning new upstream projects, “more than all other industry groups put together,” Angus Rodger, Wood Mackenzie upstream research director, said during a webcast on the outlook. Asian NOCs were “completely at the other end of the spectrum, and they’ve effectively sanctioned very, very little—almost nothing—in terms of new projects in the last few years.” That combined with inactive M&A participation results in production profiles down the road that “start to look a little ugly.”

In the US, Wood Mackenzie believes tight oil “is really going to enter its second great phase of growth,” Ellacott said. US tight oil output in 2018 will jump 1.2 million B/D, up 24% year-over-year, the consultancy forecasts. “But it’s really a sector that’s going to be on trial” as it needs show it can deliver cash flow at lower prices and profitability, he said.

“I think at $60/bbl, if oil prices are sustained at current levels, it will be a sector that does turn back into free cash-flow generation territory,” Ellacott said. “It will be looking a lot more profitable at those sort of levels.” Challenges will re-emerge, however, if prices retreat back to the low-$50s/bbl as Wood Mackenzie is currently projecting in its macro forecast.

For companies that have been deterred by the high cost of entry in US tight oil regions, Ellacott noted BHP Billiton’s possible divestment of its US onshore position will be “a good opportunity to get a material position” there. Activist investor Elliott Advisors has been pushing for either a sale or spinoff of those assets. BHP’s Permian and Haynesville holdings are expected to draw the most interest.

But Are Cost Savings Sustainable?

As for the global service sector, Rodger thinks “2018 again is going to be probably another tough year.” He explained that many of the companies remain “perhaps overly dependent on a big potential uptick in spend,” which “is one of the biggest problems” for the sector. He sees “a lot of overcapacity” remaining in the marketplace, meaning the pain will continue “until some sort of natural equilibrium comes back into the play in the market. But that’s going to take time, and we probably don’t see that happening that quickly—at least not in 2018.”

Rodger noted “this maybe represents for upstream operators their best chance to lock-in really rock-bottom costs.” Wood Mackenzie’s global costs survey indicates, however, that the global service sector has used up its capacity for margin cuts, and costs should rise in the coming years as demand strengthens. As a result, overall savings for operators in 2018 “will be materially lower than in 2016-17,” with BOE operating expenditure (opex) inflation returning—albeit at a moderate rate.

Opex savings have largely come from cuts in labor and services, streamlining operations, and lower logistics charges, the consultancy said. Cyclical and operational cost savings for conventional pre-FID projects are expected to be sustainable through 2020 before fizzling. Europe has benefited from a 25% reduction in opex between 2017 and 2014 driven by lower labor and services costs, efficiency gains, and higher production.

In the Asia-Pacific region, South America, and parts of Sub-Saharan Africa, unit opex is already starting to increase because of a lower cost base, local content requirements, and the growing need for enhanced oil recovery in mature assets. US Lower 48 investment is seen rising year-over-year to 2021 as producers attempt to balance cost inflation with output gains.

“The Permian aside, cost inflation in the US Lower 48 is just starting to warm up,” said Jessica Brewer, Wood Mackenzie principal upstream analyst. “In fact, we are beginning to see cost increases in the supply chain in 2017, spurred on by higher rig activity and the drawdown of the backlog of drilled but uncompleted wells."

According to the Barclays report, 90% of North American operators surveyed see oilfield service costs rising in 2018, driven largely by pressure pumping. Almost half of the operators surveyed nonetheless say they plan to lift their land rig counts.

While Wood Mackenzie expects global operating costs to start increasing from 2018, those costs are still projected to be 5-10% below 2014 levels in 2020.