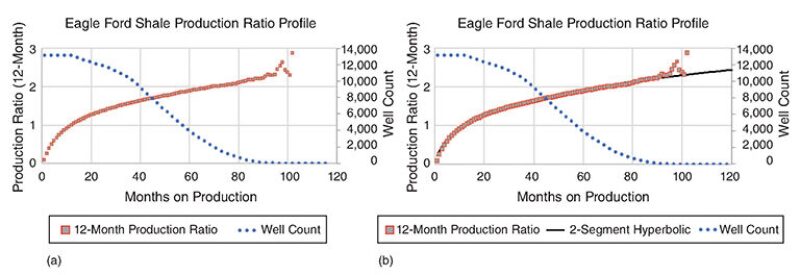

Operators and investors are interested in finding better metrics to evaluate the production performance of unconventional multifractured horizontal wells (MFHWs). The complete paper discusses the use of cumulative production ratio curves normalized to a given reference volume in time for different unconventional plays in North America to investigate the median trend for each play and the median ultimate recovery per play. The paper discusses the choice of 12-month cumulative production for a reference volume as a normalization parameter.

Introduction

Many methods exist for forecasting the production rate from unconventional reservoirs, but all have limitations. Recently, several publications have appeared relating the expected ultimate recovery (EUR) to the initial rate or the cumulative production after 3, 6, or 24 months. In the complete paper, these publications are reviewed, and their learnings extended, to several unconventional reservoirs.

Work in 2018 studied 147 MFHWs covering many formations in the Permian Basin and a wide range of input variables and determined EUR using rate transient analysis, numerical simulation, and decline-curve analysis.