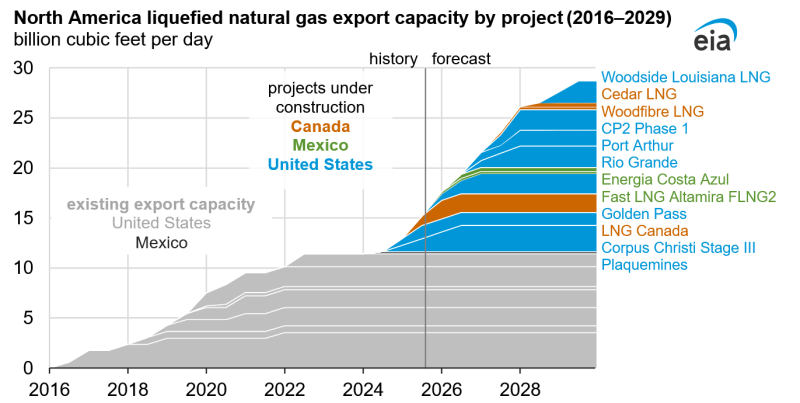

Liquefied natural gas (LNG) exporters in the US plan to more than double the country’s liquefaction capacity by adding an estimated 13.9 Bcf/D between 2025 and 2029.

The US Energy Information Administration (EIA) released data from its Liquefaction Capacity File and compilation of industry reports on 16 October. The US, already the world’s largest LNG exporter with 15.4 Bcf/D of capacity, continues to expand rapidly.

Across North America, total LNG export capacity is projected to grow from 11.4 Bcf/D at the start of 2024 to 28.7 Bcf/D by 2029, assuming all projects currently under construction begin operations as scheduled. Over the same period, Canada and Mexico are expected to add 2.5 Bcf/D and 0.6 Bcf/D, respectively. Combined, these North American additions will account for more than half of the world’s total new LNG export capacity through 2029, according to the International Energy Agency.

United States

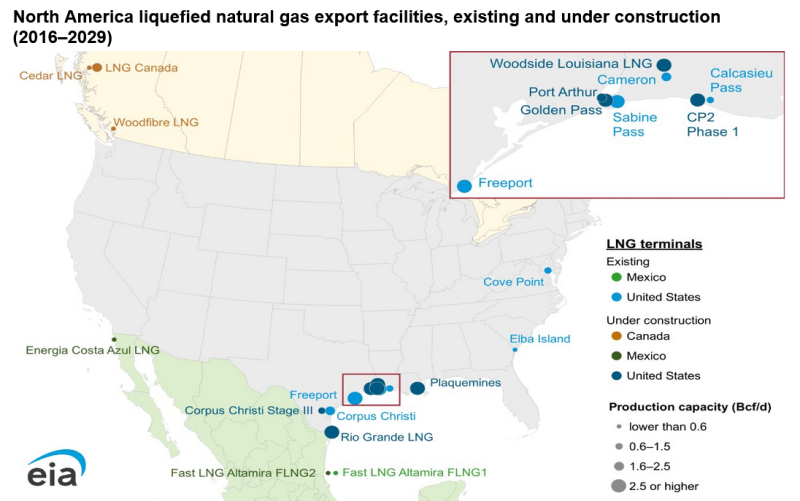

Planned liquefaction capacity additions in the US are focused along the Gulf Coast, the largest LNG export hub in the Atlantic Basin. New pipelines are being developed to supply these terminals with natural gas, though construction delays remain a potential risk for timely operations.

Plaquemines LNG Phase 1 shipped its first cargo in December 2024, while Plaquemines Phase 2 and Corpus Christi Stage III began shipping earlier in 2025 but have not yet entered commercial operation. Five additional US LNG projects have reached final investment decision (FID) and are under construction.

Port Arthur LNG Phase 1—1.6 Bcf/D

Rio Grande LNG— 2.1 Bcf/D

Woodside Louisiana LNG—2.2 Bcf/D

Golden Pass LNG—2.1 Bcf/D

CP2 Phase 1—2.0 Bcf/D

Canada

On 1 July, LNG Canada—the nation’s first LNG export terminal—shipped its first cargo from Train 1, following initial production in late June. Located in British Columbia, the facility can produce 1.84 Bcf/D from two trains (0.9 Bcf/D each) and is expected to reach full capacity in 2026. A proposed second phase would double capacity to 3.68 Bcf/D and expand the terminal to four trains, with operations expected after 2029.

Canada’s new LNG capacity on the West Coast will cut shipping times to Asia by roughly 50% compared with US Gulf Coast exports. Feedgas will be sourced from the Montney Formation in Alberta and British Columbia. Two additional projects under construction in Western Canada include: Woodfibre LNG (0.3 Bcf/D), expected to start exports in 2027, and Cedar LNG, a floating facility with up to 0.4 Bcf/D capacity, expected to begin exports in 2028.

Mexico

Mexico is developing two LNG export projects with a combined capacity of 0.6 Bcf/D: Fast LNG Altamira FLNG2 (0.2 Bcf/d) off the east coast and Energía Costa Azul (0.4 Bcf/D) on the west coast. Both projects will source feedgas from the US.

Mexico’s first LNG cargo was exported from Fast LNG Altamira FLNG1 in August 2024, supplied via the Sur de Texas–Tuxpan pipeline.