The sourcing, handling, and disposal of water is an increasing issue in US tight oil and gas operations and represents both a threat to operators and an opportunity for the supply chain. Both well count and completion intensity have grown in recent years and rising pressure from environmental regulations—e.g., federal Clean Water Act, Colorado’s Senate Bill 181, etc.—means that water management has become a key focus for operators, specifically produced water disposal and recycling.

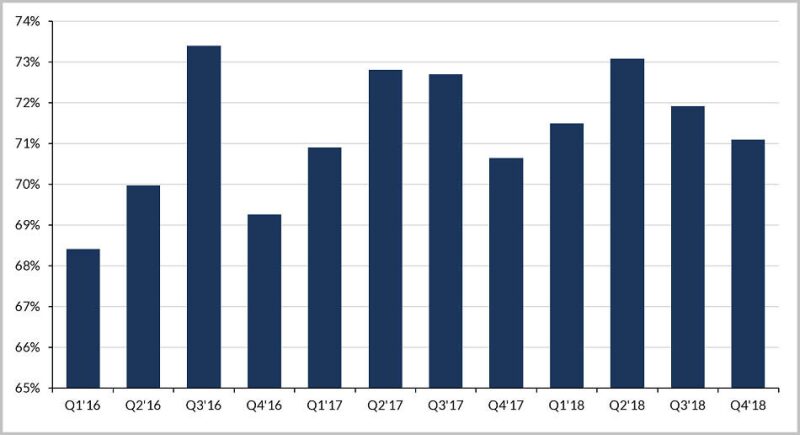

Following the downturn, the recovery in activity levels translated to not only an increase in the number of wells completed, but more importantly longer laterals using more proppant (frac sand) and water per foot during hydraulic fracturing, which created more flowback and produced water. In the Delaware Basin, the water cut for wells has increased from an average of approximately 70–72% since 2016.

Based on data from Westwood’s Energent service, a Centennial Resources 2-mile lateral in the basin uses about 26 million pounds of 100-mesh frac sand and approximately 22 million gallons of water to achieve a 47-stage fracture. With the rise of multiwell pads, these high-intensity completion practices have led to the overall increase of per well production resulting in a rise of US onshore liquids production, including water.

Produced water management costs have significantly increased for operators due to the rising number of truckloads per well required and a shortfall of available disposal or treatment capacity within reasonable distance. Pricing for disposal via road tankers currently ranges between $0.30–$2.00+ per barrel depending on available supply, location of saltwater disposable wells and local area regulations. Numerous service companies and operators have filed additional saltwater disposal well permits to handle the increase in produced water. Additionally, investment in water infrastructure created a new “water midstream” service company category.

Westwood’s analysis suggests that continued investment in water midstream along with operator collaboration will likely encourage a gradual shift toward using dedicated pipelines instead of trucks which would be a safer, more reliable, and more economical long-term solution. Secondly, using more recycled water for hydraulic fracturing would reduce requirements for sourcing fresh water as well as reduce the produced water surge for disposal, significantly alleviating the increasing water management burden on operators. Successfully developing and maintaining an adequate new transportation and recycling infrastructure is challenging but does present opportunities for service providers.

Currently, only a handful of players have been aggressively developing in-field produced water treatment and recycling services. Despite competing with large oilfield service (OFS) contractors and their technological leadership, smaller specialist contractors could likely develop and offer specific services (e.g., temporary water piping, water treatment, etc.) or the full range of recycling services at more competitive price points than large OFS contractors. Also, management services to prevent plugging, corrosion and growth of bacteria in pipelines, and optimized and cost-effective recycling plants will likely be required.

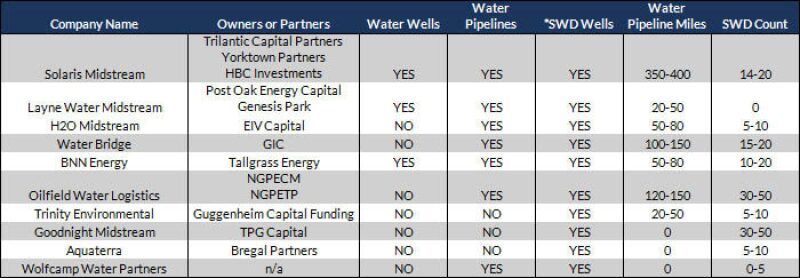

Water management to date has been basin specific. Private equity and infrastructure funds’ interest in water midstream, as demonstrated by their backing of companies such as Layne Water Midstream (Post Oak Energy Capital/Genesis Park), Waterfield Midstream (Blackstone), Water Bridge (GIC), and H2O Midstream (EIV Capital), presents a unique opportunity to create water services that scale across the US shale plays.