The US Federal Reserve Bank of Dallas gave an optimistic outlook for oil and gas in its third-quarter energy survey released this week.

The survey noted a larger-than-average number of comments from respondents, particularly regarding pipeline constraints and price differentials in the Permian Basin. The majority (70%) of executives responding said they expect the recent differentials between West Texas Intermediate (WTI) Midland and Cushing prices to have a slightly negative effect on oil production growth in the Permian over the next 6 months. However, only a small percentage of that group expects significant impacts, and 56% expects crude oil pipeline capacity to be sufficient to alleviate current takeaway constraints by the end of next year.

On average, executives expect WTI oil prices to settle at $68.81/bbl by the end of 2018—responses ranged from $55 to $85—and Henry Hub natural gas prices to reach $2.94 per million Btu.

The respondents did not have a favorable view of the US steel import tariffs enacted earlier this year: 67% say the tariffs have had either a slightly negative or a significantly negative impact on their business, with the remainder noting no impact. One respondent said the tariffs have added approximately $100,000 of costs to each of its wells, and suggested that “some thought” be given to removing the tariffs when domestic mills are not currently running the products.

Equipment utilization from the service company sector went up slightly in the third quarter, with the corresponding index moving from 41.8 to 44.8 in the third quarter. Input costs on the services side rose as well, while the index of prices received for oilfield services remained unchanged.

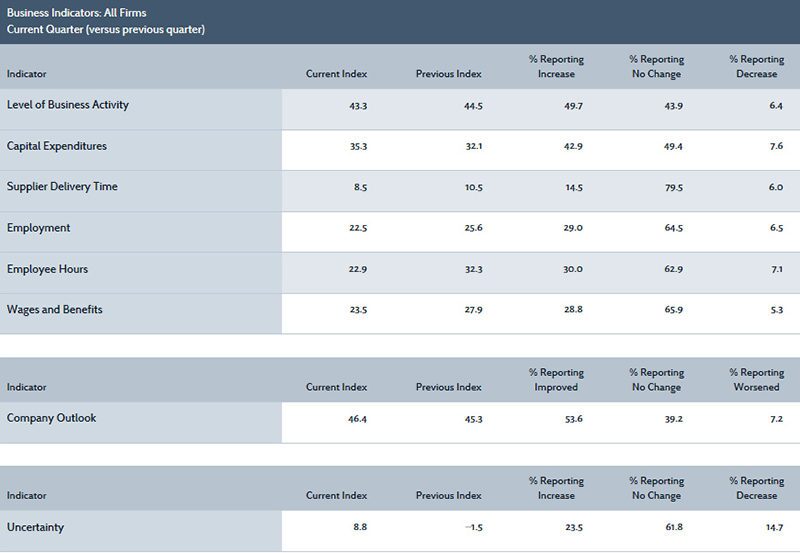

The survey’s business activity index—the survey’s broadest measure of conditions facing energy companies in the Eleventh Federal Reserve District—saw a slight drop from 44.5 in the second quarter to 43.3 in the third, but it is still close to the highest level recorded in the survey’s history. The business activity index for oilfield services companies fell from 54.2 to 45.9, suggesting a slight decline in growth, while the index for exploration and production (E&P) companies increased from 37.2 from 41.8.

Data for the survey was collected from 110 operators and 61 service companies. Each index is calculated by subtracting the percentage of respondents reporting a decrease from the percentage reporting an increase. Positive numbers in each index generally indicate expansion, while readings below zero generally indicate contraction.

Oil and gas production went up for the eighth consecutive quarter, though the oil production index went down 4.2 points from the second quarter. This decrease in the index suggests that crude production rose at a slightly slower pace in the third quarter. The natural gas production index is at its highest level ever, rising to 35.5.