ExxonMobil reduced the value of its proved reserves by one third last year and is in the process of cutting its staff by more than 10,000, which from an investor point of view has its upside.

The cut means its total reserves are the lowest since ExxonMobil’s 1999 acquisition of Mobil, according to Reuters. But oil prices have surged to more than $60/bbl, and big investor-owned companies (IOCs) that cut spending and costs can expect a surge in cash flow, according to a report from Wood Mackenzie.

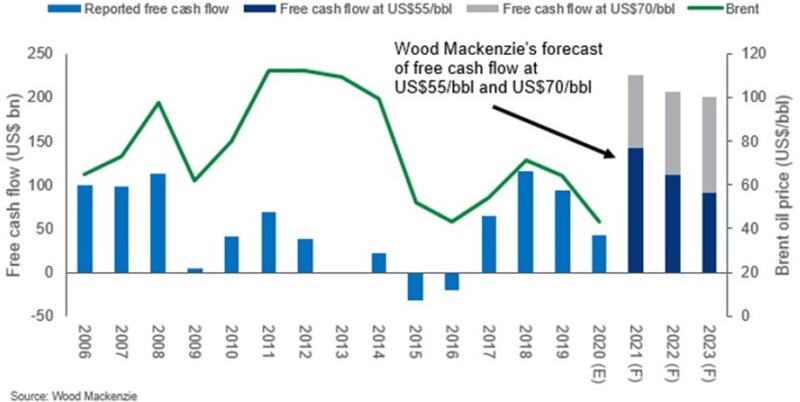

“Savage cost cuts imposed last year as the global economy contracted in the face of the COVID-19 pandemic saw average IOC corporate cash flow break-evens reduced from $54/bbl pre-crisis to $38/bbl,” said Tom Ellacott, senior vice president, corporate analysis for the energy information and consulting firm.

The deep spending cuts for Exxon Mobil, including ongoing layoffs as well as reduced expectations for future oil prices and demand, help explain its reserve estimate cut from 22.4 billion BOE to 15.2 billion, according to its annual report.

The big hits were in North America. The heaviest was a 3.7-billion-bbl reduction in expected bitumen production from its Kearl and Cold Lake operations in Canada. The second largest was a 2-billion-BOE reduction in the US. Reduced spending on unconventional drilling explains 75% of the unconventional cut, according to the company’s report.

The number of people employed by the company shrunk by 2,900 to 72,000 at the close of last year, according to the report which did not say how many contractors have been eliminated by the continuing staff reduction program.

In October, Reuters quoted a company spokesman saying 15% of the workforce could lose their jobs. At the end of 2019, Reuters reported the company employed 88,300 workers, including 13,300 contractors.

Meanwhile, big oil companies are benefiting from what Wood Mackenzie described as a V-shaped recovery, expected to generate record levels of free cash flow. If oil prices for the year average around $55/bbl, it would be the highest cash flow since 2006; if oil reaches $70/bbl, it could be double that.

For ExxonMobil that brightens the outlook for investors who had been worrying about the company’s growing debt as it borrowed to pay dividends not covered by operating earnings.

Despite higher prices, the industry appears to be sticking with tight budgets for oil and gas exploration and development.

“We expect companies to continue to plan for the worst, prioritizing net debt reduction in redeploying surplus cash flow,” Ellacott said. “Some players will also look to speed up debt reduction by selling noncore assets.”

Earlier this week, ExxonMobil did as much by selling stakes in 12 North Sea fields producing 38,000 B/D for more than $1 billion, restarting a program to sell off marginal fields that was disrupted by last year’s crash.

The money will also support work in more promising plays in Guyana, the US Permian Basin, Brazil, and liquefied natural gas development.

While some European majors are buying into renewable power, ExxonMobil’s plans remain focused on hydrocarbons, which Ellacott said is not going to be a growth business.

“Strategically, the move away from volume growth and towards harvesting the legacy oil and gas business is part of the energy transition reality—one in which pressure to decarbonize is only heading in one direction.”