While LNG supply expanded by 25.7 Mt in 2025, setting the stage for continued growth in 2026, the war in the Middle East has triggered a year-on-year contraction that could define 2026 as the year the industry suffered a 3- to 5-year setback in expansion.

Closure of the Strait of Hormuz, which cut off access to global markets for Qatar and the UAE (together accounting for nearly 16% of global operational liquefaction capacity), has caused disruptions. More significant is the multiyear repair of war-damaged plants, whose capacity shortfall now threatens to raise LNG prices across Asia and Europe.

This disruption is unlike previous ones in that, rather than creating short-term demand spikes, the closure of the Strait is destroying short-term demand, the International Gas Union (IGU) noted in its newly released 2026 World LNG Report, prepared by Rystad Energy.

Emphasizing the investment confidence that dominated the sector in 2025, IGU President Andrea Stegher noted in his preamble to the report that 68.4 mtpa of new liquefaction capacity reached a final investment decision in 2025 (compared with 14.8 mtpa the year before), “making it the strongest year for project approvals since 2019 and capping a 5-year investment cycle that approved 206 mtpa of new capacity.”

Last year also saw the sanctioning of 9.5 mtpa of new floating LNG capacity, he noted.

Flexibility and Resilience in the Face of Crisis

“While the LNG industry entered 2026 against a backdrop of escalating conflict in the Middle East and disruption to critical supply infrastructure, the (IGU) Report found that the global LNG market has demonstrated a level of flexibility and resilience not seen during the previous energy crises,” Stegher said.

“The ability of a larger and more diversified supply chain to mobilize 40% of volumes on a spot basis” has helped to contain the immediate impact of the Hormuz crisis. Further, the rising liquidity on global gas benchmarks “has offered participants the tools to manage risk,” he said.

“Looking ahead, the fundamental drivers underpinning the longer-term outlook for LNG demand through 2035 remain intact. Population growth, urbanization, digitalization, rising electricity demand, and the continued pursuit of cleaner energy systems will require reliable and flexible energy solutions which LNG is uniquely positioned to support.”

Meeting Demand With New Capacity

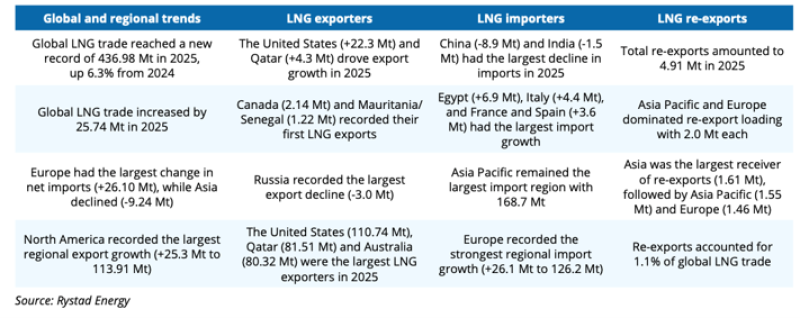

North American exports rose 25.3 mt in 2025 year-on-year as Europe’s imports climbed in parallel.

With Canada and Mauritania/Senegal becoming exporters, global LNG trade grew by 6.3% to 437 mt in 2025, the fastest rate since 2022, according to the IGU. Thirteen new regasification terminals opened last year while regasification projects were in development in eight prospective markets.

Onstreaming new capacity. A total of 30.1 mtpa of new liquefaction capacity was added last year, pushing global capacity to 524.5 mpta by year-end. The average global utilization rate in 2025 was 83.9%, a slight decline from 86.5% in 2024, driven by weather and maintenance issues, the report said.

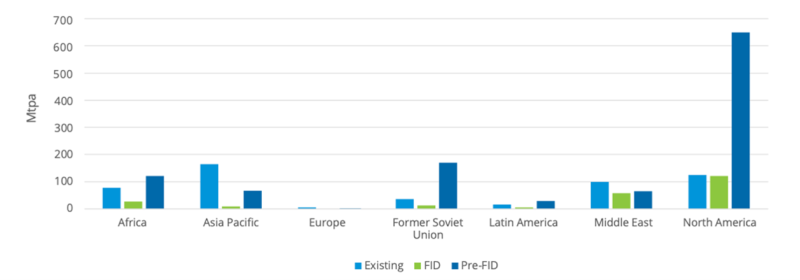

New FIDs entering the pipeline. As of the end of 2025, seven projects had reached final investment decisions (FID), bringing the total capacity of approved future liquefaction projects to 234.3 mpta.

Pre-FID assessments. Last year, 1,105.4 mtpa of proposed liquefaction capacity was under development, led by North America with 650.3 mtpa. Of that total, 384.4 mtpa was attributed to the US, 227.3 mtpa to Canada, and 38.6 mpta to Mexico.

Outside of North America, Russia followed with 170.4 mtpa, Africa (121.1 mtpa), Asia Pacific (67.0 mtpa), and the Middle East (65.7 mtpa). Elsewhere in the world, another 31 mtpa of liquefaction capacity remains in the pre-FID stage.

Political and regulatory support of LNG projects led to FIDs being concentrated in the US in 2025, particularly the Trump Administration’s lifting of the ban on non-Free Trade Agreement approvals, the IGU report pointed out. In contrast, supply and demand shocks at the start of the Russian-Ukraine conflict drove 2022 liquefaction approvals.