US shale producers moved fast last year to take advantage of a newly emerged completions technique called the simul-frac that involves stimulating two horizontal wells at the same time.

The frontrunners of this new trend are slashing completion times by more than half as compared with zipper fracturing. This is according to analysis from Rystad Energy which found the simul-frac approach represented 8% of all well completions in the US onshore sector during the fourth quarter of last year.

“That’s quite a big increase from the previous year. In 2019, we saw barely any—under 1%,” said Justin Mayorga, a senior analyst at Rystad. “Now where is this going? I think it’s a little early on to anticipate that.”

Mayorga developed the algorithm that enables the Oslo-based energy consultancy to identify simul-frac completions based on how many feet per day are being stimulated and how much horsepower is on location. A typical simul-frac requires at least 25% more horsepower than the average zipper frac spread.

Zipper fracturing remains the dominate completion technique for US producers and has seen efficiency gains of 43% since 2017. Despite this, Rystad found that 2020 simul-frac jobs completed their stages 60% faster.

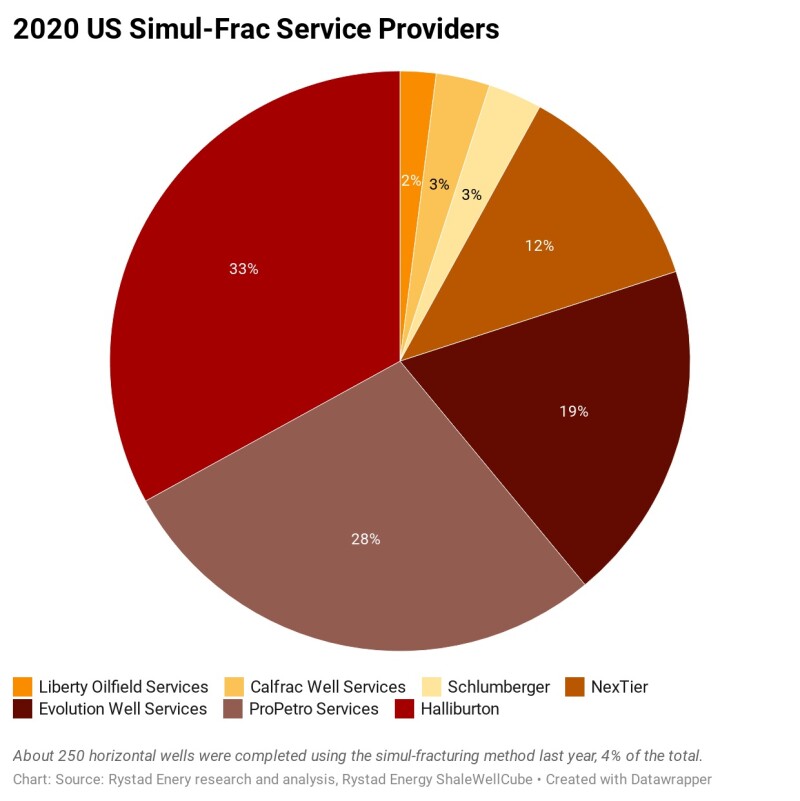

Rystad’s data also show that simul-fractured wells represented 4% of the US onshore total in 2020, or nearly 250 out of the roughly 6,000 wells completed. The oilfield service company responsible for about one-third of those jobs and the overall market leader is Halliburton.

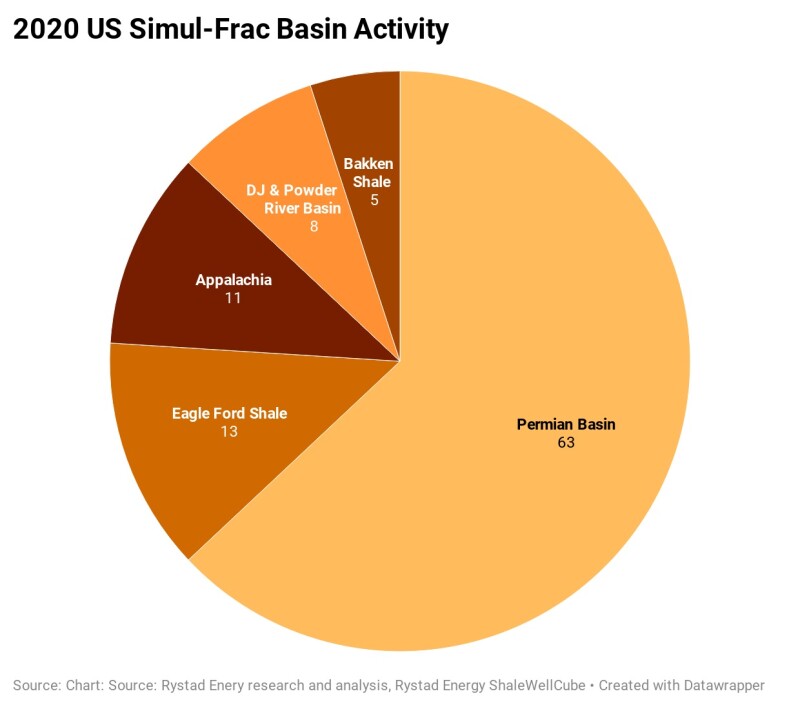

The hotbed of this trend is the Permian Basin which accounted for almost two-thirds of all simul-fracs done in the US last year. In addition to being the most active basin in the country, the Permian also has the most four-well pads—the ideal number for an operation designed to work in pairs.

Among the Permian operators that have recently taken a shine to the simul-frac is Ovintiv. Executives from the Denver-based producer highlighted during a quarterly call in October that the speedy approach is lowering average well costs by $400,000.

A Low Ceiling for Uptake?

Thomas Jacob, a vice president at Rystad, noted that the simul-frac market share today looks a lot like where the popular zipper frac method was about a decade ago. “But we don’t think we will see the same level of adoption because there are a few bottlenecks,” he said.

In 2011, around 12% of the horizontal wells in the US were completed with the zipper fracturing technique that allows for swift transitions between stages in offsetting wells. By the fourth quarter of last year, zipper fracturing represented 78% of US completions activity.

Zipper fracturing became the norm last decade because of cost savings and flexibility. The method makes economic sense in two-well configurations as it does in three-well configurations, and so on.

The cost savings of the simul-frac are best realized instead on four-well pads.

Figures from Rystad show that pads with at least four wells represented 46% of all fracturing activity on a wellhead basis. “So that is the addressable market,” for the simul-frac, said Jacob.

Further limiting uptake could be that some operators prefer not to spend their cash as fast as the simul-frac allows for.

The burn rate of these jobs is driven in large part by the need to ensure that enough water and sand are available to keep up with the pressure pumps. This might call for additional on-site storage which can increase upfront capital requirements.

Some of those opting out of the simul-frac might be doing so as a sort of hedge. Instead of bringing on their wells as soon as possible, this group may be content to move at a slower pace, which might benefit them if oil prices continue to climb.

Simul-fracs also require splitting the pumping rates between the wells, which means instead of 100 bbl/min, each well on the pad may only receive 80 bbl/min. Rystad believes this is one reason why it has not seen operators use the technique so far in highly overpressured and screenout-prone formations such as the gas-rich Haynesville Shale.

OFS Seeking Better Trade-Off

With demand for pressure pumping still depressed, service companies are understood by Rystad to be earning only minimal premiums for simul-frac contracts.

“Until the pricing gets there, the operator is taking most of the gains vs. the OFS side,” said Mayorga. Though it remains unclear, he added that the biggest benefit realized by the service providers may be lower maintenance costs.

While more pressure pumping units are required to be on location, they function at lower rates and spend less time on each pad. On the other hand, the pump engines are running constantly, which could increase equipment attrition rate in the long term.

Smaller service providers might also be particularly challenged with maintaining a backlog of work while deploying the faster fracturing method.

“That’s a big concern coming up right now,” said Mayorga of the smaller firms. “They might be just working themselves out of work by being so efficient.”

However, the value proposition could improve thanks to better technology.

Mayorga said some pressure pumpers have already begun to adapt to the simul-fracturing market by taking delivery of new units that can reach higher pump rates to reduce the overall size of each fleet.