2020 set the stage for a profound transformation in the oil and gas industry.

The oil and gas industry was already facing a challenging transition process as economies move toward a low-carbon future; however, surviving and prospering in a low-oil-price and high-risk environment is an even greater and more urgent challenge. Producers with relatively high-cost production will bear the brunt of production curtailments, since none are able to sustain uneconomic production for very long.

In the years leading to 2019, shale plays stole the show, increasing production as long as prices sustained the frantic pace of drilling required for the production increases observed in the US. On the other hand, the intrinsic characteristics of deepwater plays—highly front-loaded investments and long project cycles—worked against them. Relatively low prices that were just as challenging for shale plays were considered a reason to delay deepwater projects (Rigzone 2016).

Portfolio diversification is an important risk-mitigation strategy, whether by region, country, environment, or play type. However, for the majors of the industry, it is increasingly difficult and risky to rely on many relatively small projects to keep their portfolio pipeline full. Given the size of large companies, large projects are required to guarantee high levels of production over long periods and to keep their project portfolio manageable.

Larger plays, and those that are less subject to environmental restrictions, tend to be found in large offshore basins, where deepwater plays dominate. At the same time, the world offers fewer opportunities with acceptable country risk. Thus, larger plays in safer regions have become essential elements of the core business of large oil and gas players.

Besides offering the potential for large production, deepwater plays often can provide low Opex because of their scale and productivities, such as in the Brazilian pre-salt trend (the “pre-salt”), where many wells have consistently delivered sustained average production above 40 thousand BOPD (ANP 2020).

Furthermore, deepwater plays involve large, complex projects that are well suited to the megaproject management capabilities of large players of the industry. Those projects are also amenable to technological innovations that have delivered impressive performance improvements and cost reductions. As an example, Petrobras claims that in 2020 its lifting costs for deepwater pre-salt fields have come down to below $3.00/bbl, and under $5.00/bbl including rig-leasing costs (Petrobras 2020a).

As to innovation-related gains, two Petrobras programs represent unprecedented achievements in deep waters. Prod1000 expects to reach first oil within 1,000 days of a discovery, and Exp100 seeks to achieve a 100% discovery rate in exploratory wells, a feat that breaks the paradigm that has assigned high exploratory risks to deepwater exploration everywhere in the world (Petrobras 2020b).

Existing infrastructure in deepwater plays has also become key in locating exploration and production (E&P) activities, since it can lower Capex and aid the viability of projects that would otherwise be uneconomical.

Despite the challenges that deepwater plays offer—such as the deepwater setting itself, the need for complex equipment and large infrastructure, the need to penetrate thick salt layers, and the need for enabling technologies—they have generally been overcome very successfully. So much so that deepwater plays represent a large share of world oil production, despite being sourced from a limited number of large plays (US EIA 2016).

In 2012, the US Geological Survey (USGS) conducted a review of major conventional world oil and gas provinces and made estimates of yet-to-find (YTF) resources (USGS 2012a). Those assessments suggest geological favorability and production potential when companies consider strategic E&P targets.

However, before being considered as investment and development targets, provinces need to exhibit geological favorability, large YTF potential, at least some existing infrastructure, and offer locations that do not present serious technical or environmental impediments or country risks.

Based on those criteria, many provinces and plays can be excluded outright. Of those remaining, Northwest Australia, attractive for LNG projects, has suffered serious cost overruns which reduce its strategic attractiveness (Boiling Cold 2020). The Equatorial Margin is too undeveloped and exhibits high risk, and even standout plays in the Guyana-Suriname Basin suffer from political developments that threaten business stability (Argus 2019). The Mexican Gulf of Mexico (GOM) suffers from the political risk of undefined and volatile Mexican oil policy.

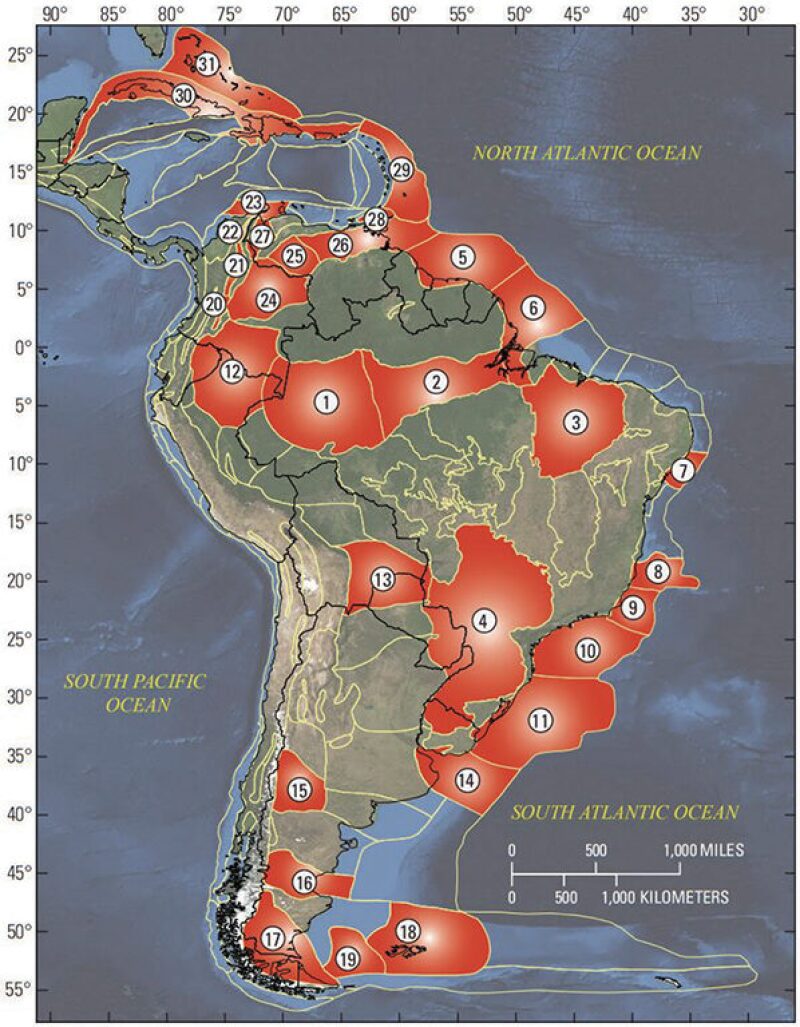

In South America, the specific USGS assessment of the region points to the Guyana-Suriname Basin and the Campos and Santos Basins (Fig. 1: provinces 5, 9, and 10) as the three with the highest YTF potential. The Santos Basin leads by far (more than twice the mean YTF potential of the other provinces combined) because it encompasses much of the pre-salt (USGS 2012b).

Elsewhere in South America, either because of high geological uncertainties, nearly undeveloped petroleum basins, or high country and regulatory risks, the prospects for a significant acceleration of industry activity are unlikely. This excludes several South American deepwater plays from consideration, including some to which the USGS assigned significant YTF potential, such as offshore Argentina and Uruguay, and large tracts considered promising frontier basins such as Pelotas.

This analysis suggests that the prime world provinces for the industry to concentrate its E&P budgets are the US GOM and the Brazilian pre-salt. The GOM already hosts numerous operators, and has the size, potential, and favorability to be able to handle a significant increase in activity and new projects. Likewise, in Brazil, besides the market-dominant presence of Petrobras, other companies have debuted in the pre-salt, which also has the size, potential, favorability, and infrastructure to attract a large number of new players and a major increase in activity and projects.

Brazilian pre-salt plays have been described as superior to the GOM plays in many respects (Jones 2020). Noteworthy is the relative disparity in potential payoffs between the two regions with GOM successes measured in as little as a few thousand BOPD from discovery wells. In the entire US, there were only 23 wells that produced over 12,800 BOPD in 2018 (US EIA 2019). In the pre-salt, over 60 wells produced more than 20,000 BOPD in May 2020 (ANP 2020). Furthermore, the potential of the pre-salt is huge, estimated to be between 176 and 273 billion barrels of recoverable oil (Jones & Chaves 2015).

However, the US GOM and the Brazilian pre-salt can be considered similarly attractive, since the GOM´s proximity to the US and the safety of a US operating environment may balance the exceptional potential of the pre-salt. This still leaves Brazil as the only world-class deepwater destination available outside the US.

New oil and gas investments can arrive in Brazil either directly, through acquisition of blocks at bidding rounds, or through farm-ins to some of the many projects waiting to be developed, many in the hands of Petrobras which does not have the financial wherewithal to proceed with all of them on its own. ANP (Brazil´s national oil agency) expects production to reach 7.5 million BOPD in 2030, from under 3 million BOPD currently, just based on existing projects (Petersohn 2019). This suggests that Brazil will inevitably become a top-five world oil producer.

In the pre-salt, production can grow in leaps of 180,000 BOPD (the typical production capacity of most standard FPSOs in the region). By 2030, ANP estimates that more than 50 new FPSOs may be added in Brazil (Abelha 2019), which suggests a potentially higher upside to production growth than current expectations.

Other analysts have also forecast a significant rise in activity in South America, especially in Brazil, as majors become more efficient and increasingly dominate deepwater projects with potential for large discoveries (Wood Mackenzie 2019).

While shale plays attracted a large and increasing share of upstream investment since 2016, the offshore sector will be least affected by the current round of severe investment reductions (Rystad 2020). This resilience reflects the long cycle times and relative inflexibility of offshore projects, once underway, but also a recognition of the strategic importance of the deepwater sector for the survival of the industry.

Going forward, the deepwater plays of Brazil will represent a significant share of new production worldwide. Among the main drivers will be the Transfer of Rights areas auctioned in 2019, pre-salt and concession bidding rounds held in the past few years, and rounds to be held in the next few years. All those rounds involve plays with multibillion barrel recoverable accumulations. A preview of what is to come can be seen in the Buzios field, which recently achieved 844,000 BOPD production from four FPSOs (Reuters 2020).

The trend toward greater investment in deepwater plays will change the face of the industry, stranding many relatively uneconomical producing plays, and eventually concentrating activities and production into major, world-class plays. Brazil stands out as the prime candidate for attracting industry investments to its plays, which exhibit exceptional potential, productivity, resilience to low oil prices, and few environmental restrictions, and are in a region that offers low operating risk.

The oil and gas industry can survive only by focusing on such plays.

References

Abelha, M. 2019. Brazilian Exploration Scenario and Opportunities. ANP APPEX presentation.

ANP. 2020. Boletim da Produção de Petróleo e Gás Natural–Maio 2020.

Argus. 2019. Guyana Oil Play Clouded by Looming Political Shift.

Boiling Cold. 2020. No Winners From Shell’s $US17B Prelude Floating LNG.

Jones, C.M. and Chaves, H.A.F. 2015. Assessment of Yet-To-Find Oil in The Pre-Salt Area of Brazil. 14th International Congress of the Brazilian Geophysical Society, Rio de Janeiro. SBGf Conference Papers, 2015.

Jones, C.M. 2020. GOM Pre-Salt Potential.

Petersohn, E. 2019. Pre-Salt Super Play: Leading Brazil Into the World’s Top 5 Oil Suppliers.

Petrobras. 2020a. Petrobras Financial Performance 1Q20.

Petrobras. 2020b. Sustainability Report.

Reuters. 2020. Brazil’s Petrobras Says Buzios Field Platforms Achieved Production Record.

Rigzone. 2016. OTC 2016: Deepwater Projects Delayed as Low Oil Prices Linger.

Rystad Energy. 2020. Global Upstream Investments Set for 15-Year Low, Falling to $383 Billion in 2020.

US EIA. 2016. Offshore Production Nearly 30% of Global Crude Oil Output in 2015.

US EIA. 2019. The Distribution of US Oil and Natural Gas Wells by Production Rate.

USGS. 2012a. An Estimate of Undiscovered Conventional Oil and Gas Resources of the World, 2012. Fact Sheet 2012-3042.

USGS. 2012b. Assessment of Undiscovered Conventional Oil and Gas Resources of South America and the Caribbean. Fact Sheet 2012-3046.

Wood Mackenzie. 2019. Deepwater’s Latin America Comeback.