Despite a growth in total capital expenditure (Capex), the outlook for subsea hardware is significantly less positive than it has been in previous years. This is due to the major decline in oil price, which has seen the price of a barrel go from a peak of USD 111 in June 2014 to below USD 50 in January, recovering to around USD 60 in April.

The high oil price over the past few years was driven by demand, particularly from China. In recent months, however, a decline in demand from regions such as Asia, Europe, and North America has led to supply overweighing demand, resulting in falling oil prices. The other major factor is the surge of US shale oil production, while the decision by the Organization of the Petroleum Exporting Countries (OPEC) to defend its market share rather than oil prices by not restricting output has piled further misery on prices.

These events will have a major impact in limiting the number of new projects sanctioned and reducing the expected annual growth until 2018 when Capex declines. The effect of the oil price decline on sanctioned projects will be limited, as in most cases, the Capex has already been assigned and at this point, operators are unlikely to stop work on a development.

Another reason that Capex will not decline too significantly is that some projects, such as Eni’s Offshore Cape Three Points in Ghana, have been ordered despite the low oil price. It is also important to note that many projects will be deferred, not canceled, and longer term growth is expected in the subsea market.

Other issues, such as the Petrobras scandal and political issues in a number of key regions, also add uncertainty to the final years of the forecast.

Drivers of Subsea Hardware Installation

Despite the collapse in oil price, there will be a number of other supply and demand side drivers that affect subsea hardware installation activity. They are the

- Move to deep water

- Development of complementary production technologies

- Marginal and remote field development

- Fields in harsh environments

The replacement of declining production from maturing basins is vital. Long-term demand for oil and gas is increasing in developing regions, and creating additional pressure to explore and produce in deeper waters. High oil prices have enabled investment in deepwater developments and technology, and previously unviable or marginal projects can now be developed in these Capex-intensive situations.

The period of high oil prices has also led to exploration of ultradeep basins: Shell’s Stones development in the US Gulf of Mexico (GOM) will have the deepest floating, production, storage, and offloading (FPSO) vessel ever installed when it begins production later this year.

However, exploration and development will now suffer because of the collapse in oil price as operators aim to ensure that low costs and high margins are established in projects before approving them. Despite this, most oil companies are taking a long-term view of the market and will only defer, not cancel, these high-Capex projects.

Although marginal fields remain a key driver, the effect of these fields will be lessened by oil price uncertainty. Sanctioned marginal projects such as the Kraken oil field in the UK North Sea will continue as planned, but new projects face a high risk of development plan delays. Similar to deepwater projects, marginal field production will be crucial for meeting the world’s energy needs and ensuring the continued development of mature basins such as the UK North Sea. The recent UK tax incentives are an example of how these marginal fields can be made economic and attractive to operators.

In recent years, the subsea sector has seen rapid technological progress to ensure that hardware can withstand higher pressures and more expansive subsea developments. This advancement has enabled cost-effective production to develop, for example, tying in additional wells to a single manifold. These small tie-ins can be uneconomic with a low oil price and, because of the speed with which they can be installed once sanctioned, a number of them are likely to be delayed until a rise in oil price is seen.

In addition, the slow maturation of subsea processing technology will enable production from challenging reservoirs including heavy oil. This is still relatively early in development, however, and use of the technology will be affected by the lower oil price. A lot will depend on the success of the large, high-Capex compression unit on Åsgard B in the Norwegian Sea. If this system proves to be a worthwhile addition to the field and operates smoothly, it will be much easier for other companies to

sanction the technology for fields that they believe require subsea processing.

Operators are becoming increasingly interested in the development of 20,000-psi hardware as fields with higher pressures and temperatures. Trees rated at 20,000 psi are still some way from being ready for use, with the first likely to be on the Kaskida-Tiber development in the GOM in the early 2020s. FMC Technologies is expected to continue development of this technology, but the uptake from operators will be constrained until a sustained high oil price convinces them that 20,000-psi projects are worth the high capital costs.

Components

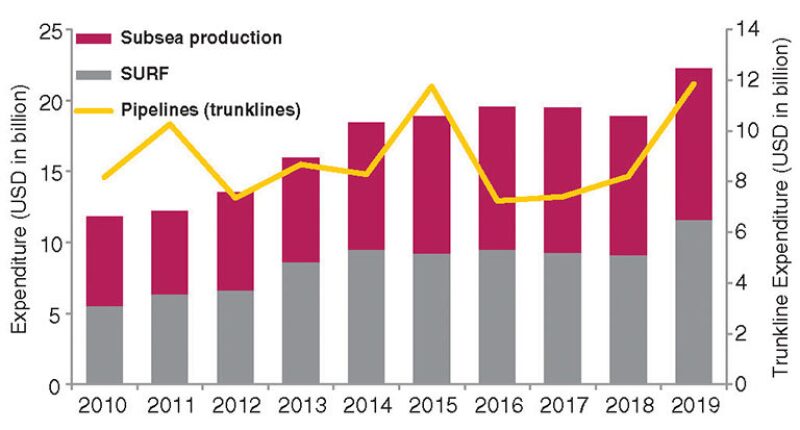

Subsea production hardware will attract USD 50 billion of expenditure from 2015 to 2019, driven by a number of large projects in deep water such as the 65-tree Kaombo project in Angola that was sanctioned early last year. Having already been commissioned, such projects will go forward and show why the market will remain steady in 2016–2017 despite the low oil price.

The subsea umbilical, riser, and flowline (SURF) market will approach USD 48 billion in Capex, boosted by a revision of development plans where projects are developed as tiebacks rather than with their own fixed or floating platform, thus increasing the length of required SURF units. This is often a cheaper solution and will be an attractive option in a time when companies are under pressure to cut costs. Also, the development of remote fields and the addition of new project phases will drive expenditure in this category.

Other factors such as the use of certain production facility designs drive higher installation Capex of particular pieces of hardware. For example, the subsea completion of wells with a floating production unit—more commonly seen in African and Latin American deepwater developments—directly drive more installations of larger riser bundles, thus increasing Douglas-Westwood’s view of the forecast spend for SURF units.

Driven by a number of large projects, the trunkline spend is forecast at USD 46 billion. The market for trunklines will remain relatively consistent from 2016 to 2018, but this will represent a decline from a high mark seen this year that resulted from the installation of pipelines such as Ichthys, a deepwater 718-km-long pipeline to be installed in Australia by Saipem.

An analysis of the top five subsea equipment vendors indicates that backlogs are at near record levels of more than USD 17 billion. However, the industrywide backlog was 6% lower than in the second quarter and 1% higher than a year ago.

The high level of backlogs will ensure that the next few years will be busy for industry players working through their current order books, and this is reflected in their share prices. Since the oil price collapse, the indexed share price of subsea hardware manufacturers has declined by 34%, significantly less than others such as drilling companies.

Over the next 2 years, a decline in backlogs is expected as new orders for equipment dry up in the low oil price market. Major subsea players such as FMC and Aker are likely to be affected, and as the number of orders shrinks, they will likely have to lower prices to win orders. It is not a simple issue, and lower costs will have to be balanced with maintaining high safety standards. This expected increase in price competition is going to be important in an area in which equipment costs continued to grow even as the oil price peaked.

It is important to highlight that this is only expected to be a short-term problem and the growth in Capex spend after 2018 shows that orders will grow again after a few lean years.

Africa to be Highest Spending Region

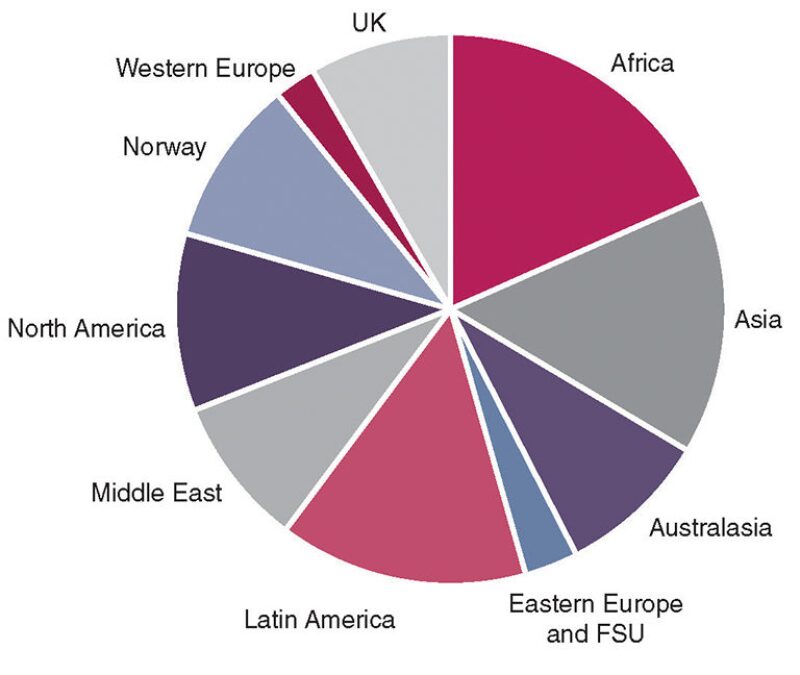

Africa will have the highest installation Capex over the forecast period and account for 18% of the total, mainly because of a number of large subsea developments including Kaombo and Egina in Nigeria. Despite this, the large number of deepwater projects, high local-content requirements, and political instability mean that Africa will be heavily affected by the oil price collapse.

A number of projects that were due to be sanctioned this year are likely to be deferred until they make sense economically. The Bonga South West-Aparo project in Nigeria is an example, with operator Shell deferring the project as a way of cutting costs. As a result, Capex in the region will decline significantly in 2017–2018. A number of projects will still be sanctioned with Eni recently ordering for its Offshore Cape Three Points development.

Latin America accounts for more than 15% of forecast subsea Capex, most of it coming from Brazil. Project execution is a major issue for Petrobras with a 70% local-content requirement and engineer shortage, thus placing pressure on the supply chain, inflating costs (reportedly up to 50%), and delaying delivery of production systems (predominantly FPSOs). Continued challenges at major Brazilian yards have led to work being farmed outside of the country.

The major issue for Brazil, however, is the scandal that has embroiled Petrobras. It has led to the departure of most of the senior management team and the banning of many companies from bidding on projects, which will likely see costs squeezed, leading to higher levels of scrutiny and project deferrals as a result. However, due to the long lead times of the hardware in Brazil, the ramifications of the scandal are not expected to be seen on installation Capex until after the forecast period.

Asia will also see high levels of hardware spend, accounting for almost the same amount as Latin America. Much of this expenditure will be for trunklines and export lines as opposed to subsea production as fixed platform developments remain a more popular option for fields in the region.

Elsewhere, subsea hardware spend is split across the globe and every region will see some expenditure. In certain regions, such as the Middle East, this will be mainly for trunklines while others will see spend mostly on subsea production equipment.

Conclusions

Overall, the market for subsea hardware will be constricted as the effect of the low oil price hits numerous projects on a global basis. While this will be negative for both operators and subsea manufacturers over the next few years, the trend is unlikely to last. Oil companies tend to take a long-term view of the market and while there will be delays, most projects will still be sanctioned once the oil price stabilizes and equipment costs lessen.

One of the sectors most affected will be the hardware manufacturers who will have to lower prices and become competitive to win the smaller number of orders available. Due to the operator’s focus on cutting Capex, the decrease in hardware prices was inevitable and will be worsened by the significantly reduced oil price.

Regionally, Africa will see the most subsea Capex over the forecast period. This will, however, be highly affected by the collapse in oil price. Deepwater developments are common and complex local-content issues prevalent in many African countries, leading to high development costs. Following Africa are Asia and Latin America, each of which has a 15% share of Capex. However, these are not the only regions that will have a noticeable share. The spend will be spread globally, thus showing the growing requirement for subsea hardware worldwide.