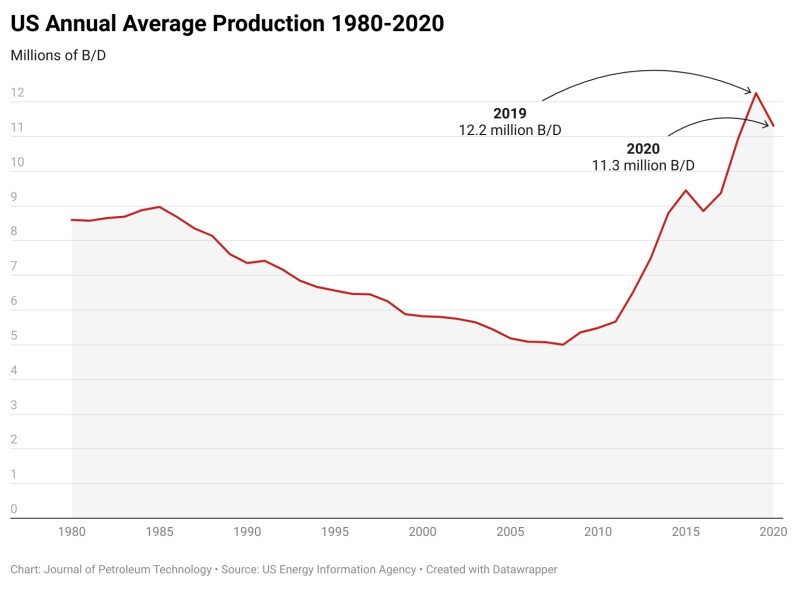

In 2019, US oil production hit a record-high average of 12.2 million B/D. Then a global pandemic put the world economy on pause and sent output tumbling down to an annual average of 11.3 million B/D.

This is according to new figures released Tuesday by the US Energy Information Administration (EIA) which said the 8% drop in 2020 represents the largest year-over-year decline in records that stretch back to the 1850s.

The numbers reveal the contrast between the pre-pandemic trajectory and that of the course altered by the virus' spread and a price war between Saudi Arabia and Russia in March:

- In January 2020, US crude was flowing at a peak rate of 12.8 million B/D.

- By May, output was down to 10 million B/D, the lowest monthly average of 2020.

The EIA estimates that in the last week of February, US oil production was back down to 10 million B/D. This followed a 100-year snowstorm that drove widespread power outages and well freeze-offs across Texas and Oklahoma.

Average output will eventually reach 11.1 million B/D for the year, the EIA projects, before possibly hitting 12 million B/D next year.

For now, though, the US slump is not being taken for granted. It is playing big time into the latest estimates on crude prices from the world’s biggest investment banks, many of which consider bounces of $5–$10/bbl likely in the short term.

Most Regions Find No Shelter From Storm

The historic decline in output can’t be all blamed on the pandemic and low prices. The EIA highlighted that the biggest regional drop came from the US Gulf of Mexico where multiple tropical storms and hurricanes forced mass shut-ins and platform evacuations. Average annual crude production in the US Gulf fell by 245,000 B/D, or 13%, to 1.65 million B/D.

North Dakota saw the second-largest reduction of 242,000 B/D to 1.18 million B/D—a 17% drop. In percentage terms, Oklahoma suffered worse, marking an 18% drop to an annual average of 469,000 B/D.

Texas, the largest oil-producing region in the country, averaged 4.87 million B/D in 2020, down only 4% from its record-high of 5.07 million B/D the year before.

New Mexico weathered the year of black swans by far the best, becoming the only region in the US to increase production. The outlier saw annual output jump by 15% to a new record of 1.18 million B/D. New Mexico is home to one half of the fastest rising US shale play, the Delaware Basin. Many producers ramped up activity there last year in anticipation of a drilling moratorium involving federal lands that was ordered in January by US President Joe Biden.

Life After Peak Production

In the background of the EIA’s year-end figures is that US production has very likely peaked. Some of the nation's largest producers appear to be coming to terms with that reality.

- “I do believe that most companies have committed to value growth, rather than production growth … And so I do believe that’s going to be part of the reason that oil production in the United States does not get back to 13 million barrels a day,” Occidental Petroleum CEO Vicki Hollub said last week in an interview with CNBC.

- During CERAWeek by IHS Markit, Pioneer Natural Resources CEO Scott Sheffield said, “I see US production flattish this year at around 11 million barrels a day with very little growth in the future.”

- Also at CERAWeek, ConocoPhillips CEO Ryan Lance said he expects future production growth to be moderated. “I hope there's discipline in the system. I think the worst thing that could happen right now is US producers start growing rapidly. I hope they give returns back to the shareholders.”

Is $100 Oil Next?

The US production picture represents the chief counterweight to the decisions made by OPEC+ which recommitted to production curtailments this month.

With US producers now wary of the word “growth” and the Saudi-led coalition of major exporters showing measured restraint, global oil prices have been marching upward. Adding momentum to the trendline are the expanding COVID-19 vaccine programs and the anticipation of increased global trade and travel.

As a result, the average cost of Brent crude futures is up more than 25% so far this year over 2020. May contracts for the international benchmark closed Tuesday at $67.52/bbl.

West Texas Intermediate (WTI) has so far seen a year-over-year rise of 34% and saw April futures close Tuesday at $64.01/bbl.

All of this means that there is once again a widening canyon between the predictions of where oil prices will go from here.

Megabanks JPMorgan Chase and Goldman Sachs have both recently concluded that the global economy is gearing up for a commodities supercycle that will carry oil prices higher.

Goldman prognosticators said last month oil may trade at $80 or higher this year. Meanwhile the oil and gas sages at JPMorgan informed investors of a tight-supply scenario unfolding in the next few years that may result in $100 oil prices.

The last time the industry enjoyed so-called “$100 oil” was in June of 2014 when prices topped out at $115 before being cut in half by January of the next year.

Many institutions began the year with average 2021 price calls of around $50, but have since issued significant upward revisions in light of lagging US production and the OPEC+ commitments. They are, however, not as bullish as other analysts and see a less dramatic snapback in prices unfolding.

- Barclays latest 2021 forecast shot up by more than 10% this month and has Brent crude averaging $62 and WTI at $58.

- Raymond James said last week that large inventory draws may drive WTI above $75. Its average price call for 2021 is $68 and then $72 in 2022.

- The EIA’s latest outlook is WTI at $57.24 and Brent crude at $60.67 for the year. The agency said it increased its forecast for both benchmarks by 14% after the decision by OPEC+ to extend production cuts into April.